Short-Term Rental Tax Loophole Explained: How STR Investors Offset W-2 Income in 2026

The short-term rental tax loophole just became roughly five times more powerful than it would have been under the old law. Without the One Big Beautiful Bill Act (OBBBA), the 2026 bonus depreciation rate would have dropped to just 20% — the second-to-last step in a scheduled phase-out to zero. Instead, the OBBBA permanently restored 100% bonus depreciation for property acquired after January 19, 2025, turning 2026 into one of the most favorable years on record for STR investors looking to offset W-2 income with rental losses.

The STR tax loophole rests on three pillars: the IRS 7-day rule that reclassifies your rental as a nonpassive activity, the material participation tests that prove you actively manage the property, and cost segregation paired with bonus depreciation that generates six-figure paper losses in year one. This guide breaks down each component with real numbers, IRS citations, and a complete worked example showing how a $400K Airbnb property can produce approximately $28,000 in federal tax savings in its first year of operation.

Disclaimer: This article is for educational purposes only and does not constitute tax, legal, or investment advice. Tax laws are complex and individual circumstances vary. Consult a qualified CPA or tax attorney before implementing any tax strategy described here.

What Is the Short-Term Rental Tax Loophole?

The short-term rental tax loophole is an exception under IRC Section 469 that allows rentals with average guest stays of 7 days or less to be treated as nonpassive activities when the owner materially participates. This distinction is critical: nonpassive losses can offset active income sources like W-2 wages, while passive rental losses cannot.

Under standard tax rules, rental activities are automatically classified as passive regardless of the owner's involvement. This means any losses from a traditional long-term rental are trapped — they can only offset other passive income, not your salary or business earnings. The $25,000 passive loss allowance phases out entirely above $150,000 in adjusted gross income, making it irrelevant for most high-income investors.

The STR exception exists because, as one r/airbnb_hosts community member put it, "Most of the tax law about rentals is about LTRs not STRs." The tax code was written with long-term leases in mind. Short-term rentals that require active daily management — guest communication, turnover coordination, pricing adjustments — function more like a business than a passive investment. The IRS acknowledges this by exempting them from the passive activity rules when the owner is genuinely involved.

STR Loophole vs Real Estate Professional Status (REPS)

Many investors confuse the STR loophole with Real Estate Professional Status (REPS), but they serve different taxpayer profiles. Here is how they compare:

| Dimension | STR Loophole | Real Estate Professional Status (REPS) |

|---|---|---|

| Hours required | 100+ hours (Test #3) or 500+ hours (Test #1) in rental activity | 750+ hours in real estate AND more than 50% of total working hours |

| Day job compatibility | Yes — can keep W-2 job | Difficult — real estate must be your primary job |

| Property type | Must be STR with avg stay of 7 days or less | Any rental property (STR or LTR) |

| Spousal qualification | Each spouse qualifies independently | One spouse can qualify for the household |

| Audit risk | Moderate — IRS scrutinizes hour logs | High — IRS closely examines 750-hour / 50% claims |

| Best for | W-2 earners with 1-3 self-managed STRs | Full-time real estate investors or agents |

The IRS 7-Day Rule: How Short-Term Rentals Get Special Tax Treatment

The IRS 7-day rule is the gateway to the entire STR tax strategy. Under Treasury Regulation 1.469-1T(e)(3)(ii)(A), a rental activity is excluded from the passive activity rules if the average period of customer use is 7 days or less. This classification transforms the rental from a passive activity into a trade or business activity for tax purposes.

How the Average Is Calculated

The IRS uses the weighted average of all rental periods during the tax year — not the median, not the mode, and not any single booking. Every night your property is rented counts toward this calculation.

Here is how it works in practice. Suppose your Airbnb had 30 bookings in 2026:

- 25 bookings averaging 3 nights each = 75 total nights

- 5 bookings averaging 10 nights each = 50 total nights

- Weighted average: 125 total nights / 30 bookings = 4.17 days

At 4.17 days, this property qualifies under the 7-day rule. Even though five bookings exceeded 7 nights, the annual weighted average stays well below the threshold.

The 30-Day Exception

What if your average guest stay falls between 8 and 30 days? You may still qualify if you provide significant personal services to guests — services comparable to those offered by a hotel or bed-and-breakfast. Standard Airbnb hosting (providing linens, Wi-Fi, a stocked kitchen) does not meet this bar. However, properties that offer daily housekeeping, meals, or concierge services could qualify under the extraordinary personal services exception.

Practical Tracking Tips

Material Participation: The 7 IRS Tests (and Which One STR Hosts Actually Pass)

Meeting the 7-day rule is only half the equation. To classify your STR losses as nonpassive, you must also demonstrate material participation in the rental activity. The IRS defines material participation as "regular, continuous, and substantial" involvement, measured against seven specific tests under Regulation 1.469-5T.

The Seven Tests

- Test #1: You participate in the activity for 500+ hours during the tax year

- Test #2: Your participation constitutes substantially all participation in the activity

- Test #3: You participate 100+ hours AND more than any other individual (including employees and contractors)

- Test #4: The activity is a "significant participation activity" and your total hours across all such activities exceed 500

- Test #5: You materially participated in the activity in any 5 of the prior 10 tax years

- Test #6: The activity is a personal service activity and you materially participated in any 3 prior tax years

- Test #7: Based on all facts and circumstances, you participated on a regular, continuous, and substantial basis

Which Tests STR Hosts Actually Use

For most Airbnb hosts with W-2 jobs, Test #3 is the most achievable path: log 100+ hours on the property during the year and ensure no other single individual — including your cleaning crew, co-host, or property manager — exceeds your hours. At roughly 2 hours per week, 100 hours is realistic for anyone who actively manages their listing.

Test #1 (500+ hours) works for investors with multiple properties or those who self-manage extensively. At 500 hours across a single property, you are spending nearly 10 hours per week — a significant commitment, but achievable for hands-on hosts who handle their own turnovers, maintenance, and guest communication.

What Counts as Qualifying Hours

The IRS accepts a broad range of management activities for material participation in an STR:

- Guest communication — responding to inquiries, coordinating check-ins, handling issues

- Pricing adjustments — monitoring market rates, updating nightly prices, managing minimum stays

- Cleaning coordination — scheduling turnovers, inspecting cleanliness, restocking supplies

- Listing management — updating photos, writing descriptions, responding to reviews

- Maintenance oversight — scheduling repairs, coordinating vendors, conducting inspections

- Financial management — bookkeeping, expense tracking, tax preparation related to the property

- Market research — analyzing comparable listings, studying occupancy trends, evaluating amenity upgrades

The Contemporaneous Log Requirement

The IRS expects a contemporaneous log — meaning you record hours as they occur, not reconstructed at tax time. Retroactive logs assembled during an audit carry minimal weight. The most effective method, cited by multiple tax advisors including WCG Inc., is a Google Calendar or spreadsheet with entries like: "Feb 15 — 1.5 hrs — responded to 3 guest inquiries, updated pricing for March." Date, duration, and specific activity — every time.

Cost Segregation and 100% Bonus Depreciation: The 2026 Game-Changer

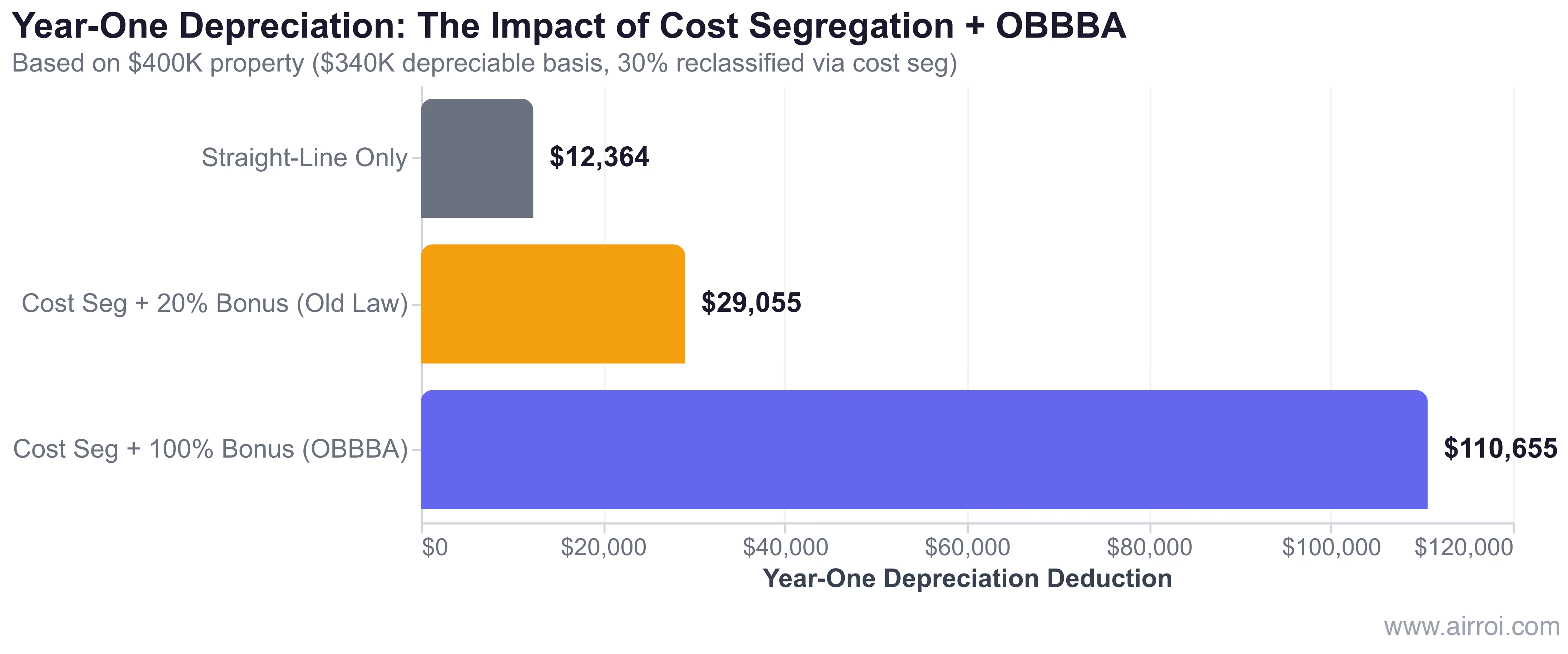

A cost segregation study is the mechanism that transforms the STR tax loophole from a modest benefit into a powerful wealth-building strategy. Without cost segregation, your $400K property depreciates over 27.5 years at roughly $12,364 per year — a useful deduction, but not large enough to generate the paper losses that offset W-2 income. With cost segregation, that same property can produce $110,000+ in year-one deductions.

How Cost Segregation Works

A cost segregation study is an engineering-based analysis that reclassifies components of a building from the standard 27.5-year MACRS depreciation schedule into shorter recovery periods. According to CSSI Services and Cut My Taxes, a typical study identifies 20-45% of a residential property's value as eligible for accelerated depreciation. These reclassified components fall into three buckets:

- 5-year property: appliances, carpeting, cabinetry, decorative lighting, window treatments

- 7-year property: office furniture, certain decorative fixtures, specialized equipment

- 15-year property: landscaping, fencing, driveways, sidewalks, parking areas

Everything that remains — the structural shell, roof, foundation, and primary systems — stays on the 27.5-year schedule. The value of cost segregation is that it front-loads depreciation, creating larger deductions in the early years of ownership.

The OBBBA's Permanent 100% Bonus Depreciation

The impact is dramatic. Before the OBBBA, the Tax Cuts and Jobs Act had set bonus depreciation on a declining schedule:

| Tax Year | Pre-OBBBA Rate | Post-OBBBA Rate (property acquired after 1/19/2025) |

|---|---|---|

| 2022 | 100% | N/A (pre-law) |

| 2023 | 80% | N/A |

| 2024 | 60% | N/A |

| 2025 (before 1/20) | 40% | 40% (grandfathered) |

| 2025 (after 1/19) | 40% | 100% |

| 2026 | 20% | 100% |

| 2027+ | 0% | 100% (permanent) |

Without the OBBBA, property placed in service in 2026 would qualify for only 20% bonus depreciation — and the benefit would vanish entirely by 2027. The permanent restoration makes cost segregation for short-term rental properties a fundamentally different proposition than it was just two years ago.

Cost and ROI of a Study

A cost segregation study for a residential rental property typically costs $5,000-$15,000, according to Patrick Accounting. For larger or more complex commercial properties, fees can reach $60,000. The return on investment is substantial: HCVT LLP's analysis found that cost segregation paired with 100% bonus depreciation delivers a 550% increase in year-one depreciation compared to straight-line alone. KDA Inc. reports that "For 2025 and beyond, owners typically see $50K to $500K+ deductions their first year alone."

Real Numbers: Tax Savings Walkthrough on a $400K Airbnb Property

Theory matters, but numbers convince. Here is a complete worked example showing how the STR tax loophole, cost segregation, and 100% bonus depreciation combine on a $400K short-term rental property.

The Setup

| Item | Amount |

|---|---|

| Purchase price | $400,000 |

| Land value | $60,000 |

| Depreciable basis | $340,000 |

| Cost segregation study fee | $7,500 |

| Percentage reclassified by cost seg | 30% |

| Reclassified into 5/7/15-year categories | $102,000 |

| Remaining structure (27.5-year) | $238,000 |

Year-One Depreciation Calculation

| Component | Calculation | Deduction |

|---|---|---|

| 5/7/15-year property (100% bonus) | $102,000 x 100% | $102,000 |

| Remaining structure (straight-line) | $238,000 / 27.5 years | $8,655 |

| Total year-one depreciation | $110,655 |

The Paper Loss

| Item | Amount |

|---|---|

| Gross rental income | $55,000 |

| Operating expenses (cleaning, utilities, insurance, repairs, management software, cost seg fee) | -$27,500 |

| Net operating income | $27,500 |

| Year-one depreciation | -$110,655 |

| Paper loss (nonpassive) | -$83,155 |

Tax Savings

At a 37% marginal federal tax rate (income above $626,350 for single filers in 2026), the $83,155 nonpassive loss offsets W-2 income and produces approximately $30,767 in federal tax savings in year one. Add state income tax savings for high-tax states like California (13.3%) or New York (10.9%), and total first-year savings can exceed $40,000.

The property generates positive cash flow — $27,500 in net operating income — while simultaneously producing a paper loss for tax purposes. This is the core mechanism of the STR tax loophole: depreciation is a non-cash deduction that creates a loss on paper without any actual economic loss.

What About a Smaller Property?

Not every investor starts at $400K. Analysis by R.E. Cost Seg shows that even a $200K rental house can yield $10,000-$15,000 in first-year tax savings from a cost segregation study costing $5,000-$7,000. That represents a 1.5-3x return on investment in year one alone — before accounting for ongoing depreciation benefits in subsequent years.

5 Pitfalls That Get the STR Tax Loophole Disqualified

The STR tax loophole is legitimate tax law, but it has precise requirements. Failing to meet any one of them can disqualify your deductions, trigger back taxes, and invite IRS scrutiny. These are the five most common mistakes.

1. Schedule C Misclassification

Most STR income belongs on Schedule E (rental income). However, if you provide "substantial services" to guests beyond basic amenities — meals, daily housekeeping, guided tours, concierge services — the IRS may reclassify the activity as a business requiring Schedule C reporting. The consequence: self-employment tax at 15.3% on top of income tax. Standard Airbnb hosting (linens, Wi-Fi, kitchen access, a welcome basket) does not trigger Schedule C. Daily maid service or a full breakfast spread might.

2. Personal Use Day Violation

Under IRC Section 280A, personal use of your rental property is limited to the greater of 14 days or 10% of the days the property is rented at fair market value. Exceed this threshold and the IRS can disallow a portion of your deductions. Every day you, your family, or friends stay at the property for free (or below market rate) counts as a personal use day. Track these meticulously.

3. Failure to Document Material Participation Hours

The IRS requires contemporaneous documentation of material participation hours. Assembling a log retroactively during an audit is a red flag that weakens your position. Investors who track hours only at tax time — or not at all — risk losing the nonpassive classification entirely, which converts all claimed losses to passive and triggers amended returns, back taxes, and interest.

4. Outsourcing Everything to a Property Manager

This is the most common disqualifier. If a full-service property management company handles all guest communication, pricing decisions, turnover coordination, and maintenance — and the owner's involvement is limited to reviewing monthly reports — material participation fails. At approximately 20 hours per year of passive oversight, the owner meets none of the seven IRS tests. Investors must retain meaningful, documented involvement even when using property managers.

One skeptic on r/tax articulated the concern directly: "You're contorting your long-term behavior in order to gain a one-time tax advantage." The critique has merit when investors fabricate participation — but it misses the mark for those who genuinely operate their STR as a business. The key distinction is between active management and passive ownership.

5. Ignoring Depreciation Recapture

Accelerated depreciation is a deferral, not an elimination. When you sell the property, the IRS recaptures previously claimed depreciation at a 25% tax rate under Section 1250 unrecaptured gains. On the $110,655 of year-one depreciation in our example, that represents $27,664 in recapture tax at sale.

The mitigation strategy: a 1031 exchange defers depreciation recapture indefinitely by rolling proceeds into a replacement investment property. The time value of money also works in your favor — $30,000 in tax savings today is worth more than $27,000 in recapture tax paid 7-10 years from now.

How AirROI Data Strengthens Your STR Tax Strategy

Qualifying for the STR tax loophole starts before you purchase a property. The right market data ensures your investment meets the 7-day rule, generates sufficient revenue to justify cost segregation, and offers a property price point that maximizes your depreciation-to-income ratio.

Average Stay Duration in AirROI Atlas

Revenue Projections via the Calculator

Market Comparison for Cost Seg ROI

Frequently Asked Questions

The short-term rental tax loophole is an IRS provision under IRC Section 469 that exempts rentals with average guest stays of 7 days or less from passive activity loss rules. When the owner materially participates, losses from the STR can offset active income like W-2 wages — something traditional long-term rental losses cannot do. The combination of this rental activity classification with cost segregation and bonus depreciation enables investors to generate paper losses that directly reduce their tax burden on employment income.

Yes. The STR loophole is based on longstanding IRS regulations under IRC Section 469 and has not been targeted for removal. According to The Real Estate CPA, "the loophole itself is not on the chopping block." The One Big Beautiful Bill Act actually made the strategy more powerful by permanently restoring 100% bonus depreciation for property acquired after January 19, 2025. As confirmed by IRS Publication 946, the depreciation rules and MACRS recovery periods that underpin this strategy remain fully in effect.

You need to pass at least one of seven IRS tests. The most common for STR hosts is Test #3: work 100+ hours on the property AND more time than any other individual, including contractors. Qualifying activities include guest communication, pricing adjustments, cleaning coordination, maintenance oversight, and listing management. Test #1 requires 500+ hours but does not require you to work more than anyone else. Keep a contemporaneous log with dates, hours, and specific activities — the IRS requires this documentation on audit.

It depends on your level of involvement. If a property management company handles all guest communication, pricing, and turnover, you likely cannot meet material participation tests. You must retain meaningful, documented involvement — such as making pricing decisions, managing the listing, and coordinating maintenance — even if you outsource some tasks. The critical factor is that your total hours must exceed 100 (for Test #3) and exceed the hours of any single other individual working on the property.

Generally yes, especially with 100% bonus depreciation restored. Analysis by R.E. Cost Seg shows a $200K rental house can yield $10,000-$15,000 in first-year tax savings from a study costing $5,000-$7,000. That is a 1.5-3x return on investment in year one alone. The break-even point occurs when the reclassifiable portion of your property value (typically 20-45% per CSSI Services) generates enough accelerated depreciation to exceed the study cost several times over — a threshold most properties above $150,000 clear comfortably.