Southeast Asia's STR Crackdown: What AirROI Data Shows About the Region's Enforcement Wave

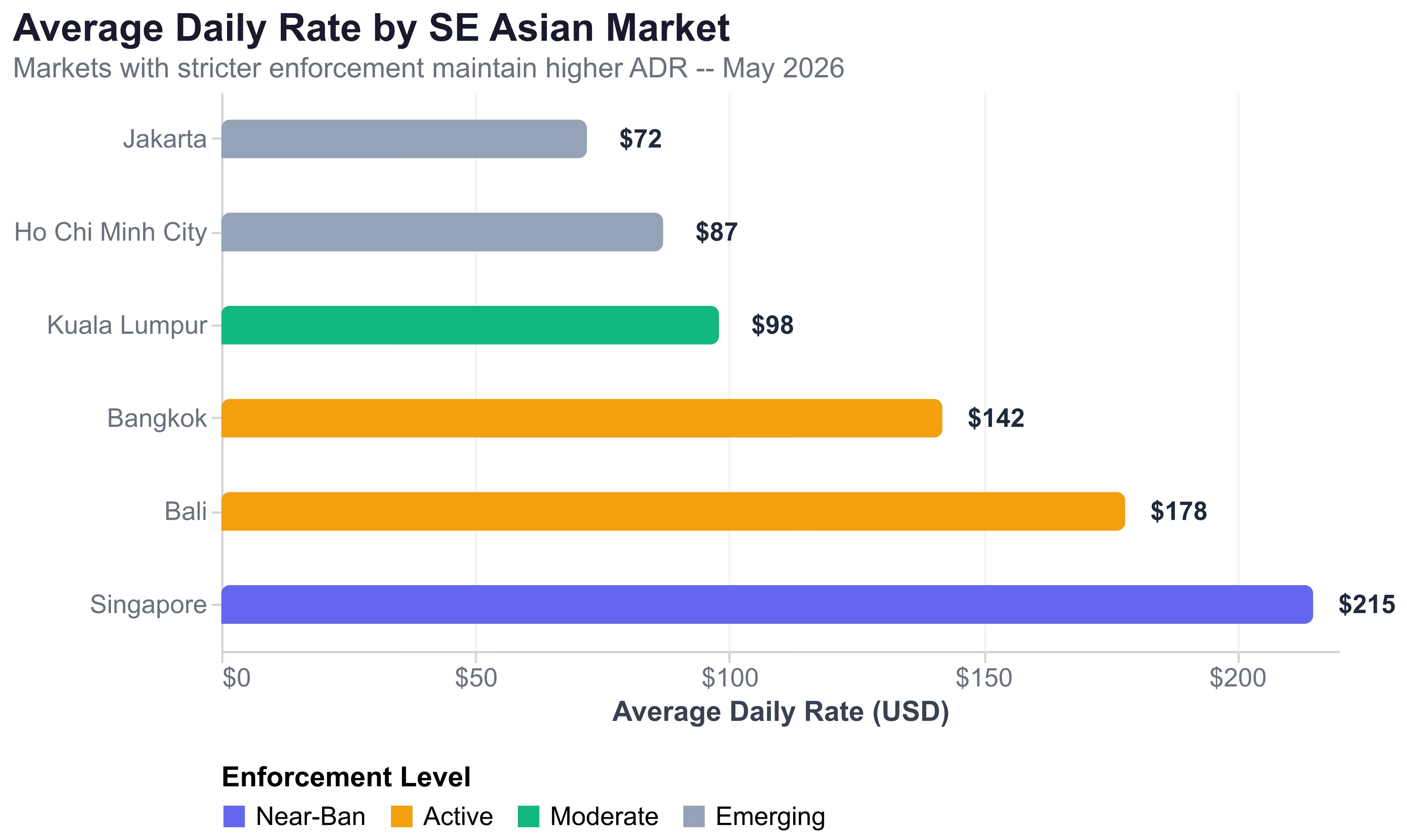

Across six major Southeast Asian markets, AirROI tracks approximately 99,000 active short-term rental listings. Five of those six markets have enacted or proposed STR restrictions in 2026. Singapore's near-ban compresses supply to just 1,240 listings -- but those listings achieve a $215 average daily rate, three times Jakarta's $72 ADR in a market where enforcement remains nascent.

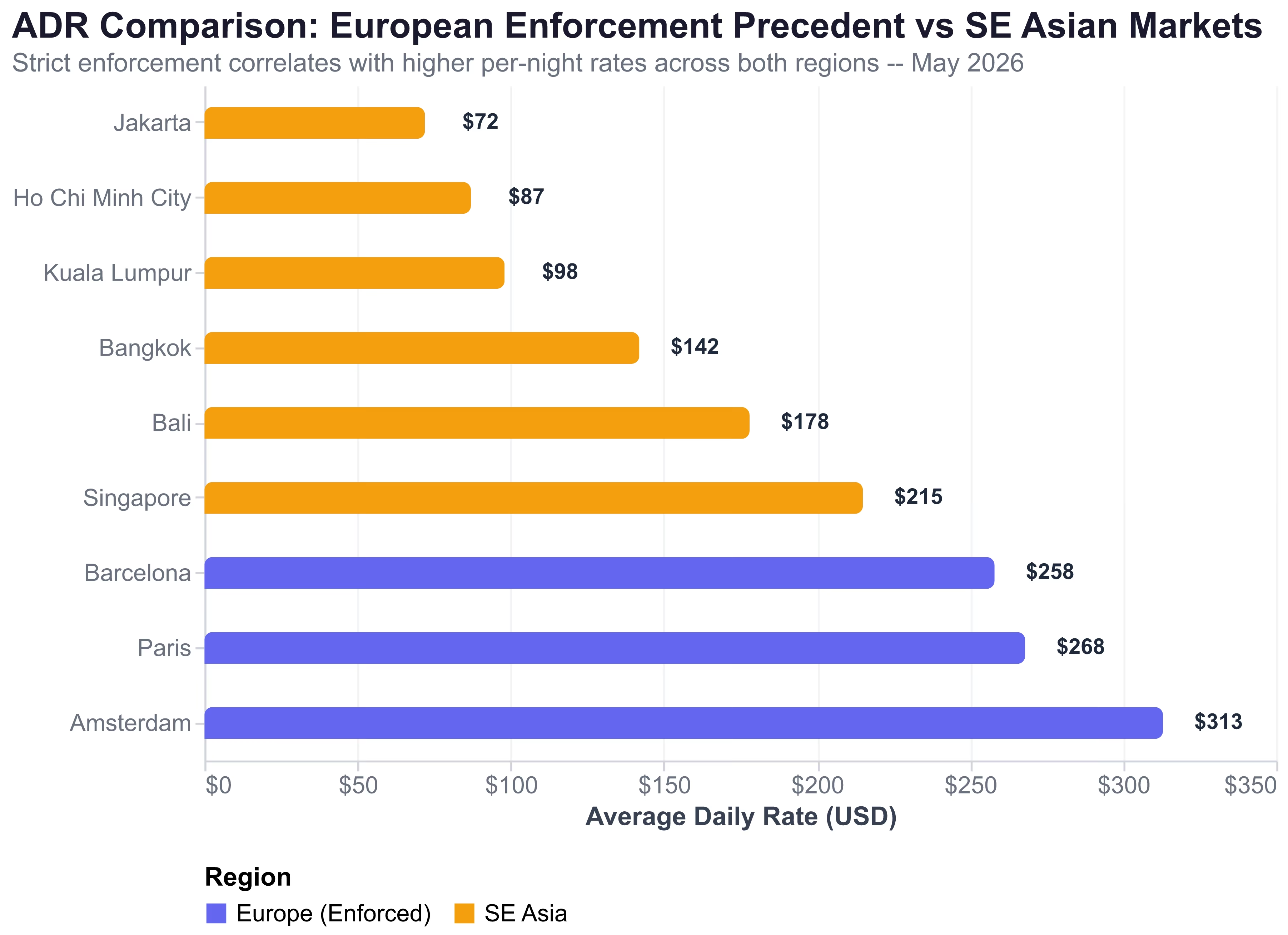

That ratio is not a coincidence. It mirrors a pattern we have documented extensively in European enforcement markets. Amsterdam, operating under a 30-night annual cap, maintains a $313 ADR -- 73% higher than Madrid's $181 in a lightly-enforced Spanish market. Barcelona, facing a complete license phaseout, still generates $36,732 in median annual revenue per listing.

Southeast Asia is running Europe's enforcement playbook in fast-forward. The question is not whether regulation will reshape these markets -- it is whether the data shows the same supply-compression dynamics already in motion.

The Enforcement Wave: Market by Market

Southeast Asia's regulatory landscape is more fragmented than Europe's, but the trajectory is clear. From outright bans to licensing mandates to registration requirements, governments across the region are moving to bring STRs under formal oversight.

| Market | Regulation Type | Key Restriction | Max Fine | Active Listings | ADR (USD) | Occupancy | Annual Revenue (USD) |

|---|---|---|---|---|---|---|---|

| Singapore | Near-ban | 3-month minimum stay | SGD 200,000 | 1,240 | $215 | 58% | $26,100 |

| Bangkok | Hotel Act enforcement | License required for <30 days | THB 40,000 | 28,450 | $142 | 62% | $22,800 |

| Bali | Licensing requirement | Pondok Wisata permit | IDR 50M | 34,200 | $178 | 67% | $28,400 |

| Kuala Lumpur | Moderate restrictions | Strata title approval required | MYR 50,000 | 18,900 | $98 | 55% | $14,200 |

| Ho Chi Minh City | Emerging registration | Tax compliance mandate | VND 100M | 9,800 | $87 | 53% | $12,600 |

| Jakarta | Emerging licensing | Business permit required | IDR 30M | 6,500 | $72 | 48% | $9,400 |

Source: AirROI market data, May 2026. Revenue and ADR in USD.

Singapore -- The Near-Ban Laboratory

Singapore operates the most restrictive STR environment in Southeast Asia. Under the Planning Act and Public Residential Property Act, short-term stays under three consecutive months are prohibited in HDB flats (public housing, which houses roughly 80% of Singapore's population) and tightly restricted in private condominiums. The Urban Redevelopment Authority (URA) enforces compliance, with violations carrying fines up to SGD 200,000 (~USD 150,000).

The result is dramatic supply compression. AirROI data shows only approximately 1,240 active listings in Singapore -- the smallest pool of any major Southeast Asian market. Yet those listings command a $215 ADR, the highest in the region. The mechanism is identical to what Amsterdam demonstrates in Europe: when regulation eliminates casual and non-compliant supply, remaining operators capture demand at premium rates.

Singapore's enforcement is also the most technologically sophisticated in the region. URA cross-references platform listings with property records and has partnered with Airbnb on a compliance framework that automatically flags listings violating minimum stay requirements.

Thailand (Bangkok) -- Hotel Act Enforcement Intensifies

Thailand's Hotel Act (B.E. 2547) requires any accommodation offering stays under 30 days to hold a valid hotel license. For years, enforcement was inconsistent. That changed in 2025-2026 as the Department of Provincial Administration expanded inspections, particularly in Bangkok's high-tourism districts like Sukhumvit, Silom, and the Old City.

The Hotel Act creates a clear binary: operators either hold a license or face fines up to THB 40,000 (~USD 1,100) and potential criminal penalties. Licensed operators must meet fire safety, building code, and insurance standards. Bangkok has also explored a dedicated "home-sharing" licensing category, but no formal framework has been finalized as of May 2026.

AirROI data shows Bangkok's 28,450 active listings maintain a $142 ADR with 62% occupancy, generating $22,800 in median annual revenue. The market's size suggests enforcement remains partial -- many operators continue to list without proper licensing. But the trend is toward formalization, and operators who invest in compliance early position themselves for the premium pricing that typically follows supply compression.

Malaysia (Penang) -- Strata Title Battles

Malaysia's STR regulation is geographically fragmented. Penang has moved most aggressively, with the state government and local strata management corporations actively restricting short-term rentals in residential buildings. Strata titles in many Penang condominiums now explicitly prohibit stays under 30 days, enforceable through management body bylaws.

Kuala Lumpur takes a more permissive approach but still requires strata management approval for STR operations. The Strata Management Act 2013 gives management bodies the authority to restrict short-term rentals through special resolutions, and several high-profile KL developments have exercised this power.

AirROI data shows Kuala Lumpur's 18,900 listings at a $98 ADR and 55% occupancy -- modest figures that reflect a market where regulation has not yet compressed supply significantly. The gap between KL's $98 ADR and Singapore's $215 illustrates how enforcement intensity maps directly to per-night pricing.

Vietnam (Ho Chi Minh City) -- Registration and Tax Compliance

Vietnam's regulatory framework for STRs is evolving rapidly. Ho Chi Minh City authorities introduced registration requirements for short-term rental operators in late 2025, requiring hosts to register with local ward-level authorities and comply with tourist accommodation reporting obligations under Decree 168/2017.

The real enforcement lever is tax compliance. Vietnam's General Department of Taxation has stepped up monitoring of digital platform income, requiring hosts to declare STR revenue and pay personal income tax (typically 5-7% of gross rental income). Cross-referencing platform data with tax filings is still manual and inconsistent, but the direction mirrors Greece's pioneering approach in Europe.

AirROI data shows Ho Chi Minh City's 9,800 listings at an $87 ADR and 53% occupancy, generating $12,600 in median annual revenue. The market is at an early enforcement stage -- comparable to where many European markets sat before the EU framework standardized data-sharing obligations.

Indonesia (Bali and Jakarta) -- The Dual-Track System

Indonesia operates a dual-track regulatory system that differs sharply between Bali and Jakarta. In Bali, STR operators must obtain a Pondok Wisata (homestay) permit from the local regency government. The permit requires fire safety compliance, environmental impact assessments, and community association approval. Foreign ownership of properties used for STR purposes faces additional restrictions under Indonesia's land ownership laws.

Jakarta requires business permits (Izin Usaha) for accommodation services, but enforcement has been sporadic. The city government has signaled intentions to strengthen oversight, particularly in apartment complexes where STR operations conflict with residential zoning.

Bali's numbers tell a distinctive story. With 34,200 active listings and a $178 ADR, Bali achieves the highest per-listing annual revenue in Southeast Asia at $28,400 -- driven by strong international tourism demand and 67% occupancy. Jakarta's 6,500 listings at $72 ADR reflect a market where both demand and enforcement are less mature.

AirROI Data: How Enforcement Intensity Shapes SE Asian Markets

The data across 99,000+ listings reveals a clear correlation between enforcement intensity and per-night pricing. The three markets with the most active enforcement -- Singapore ($215), Bali ($178), and Bangkok ($142) -- command ADR levels 2x to 3x higher than the two markets with emerging regulation (Ho Chi Minh City at $87 and Jakarta at $72).

This is not simply a cost-of-living effect. Singapore's ADR exceeds what its market size would predict, given only 1,240 listings serve one of Asia's most visited cities. Bali's $178 ADR outperforms Kuala Lumpur's $98 despite both markets drawing similar tourist demographics. The variable that separates the top tier from the bottom tier is enforcement -- and enforcement's downstream effect on supply.

The occupancy data reinforces this. Singapore (58%), Bangkok (62%), and Bali (67%) all maintain occupancy rates above the regional average, indicating that demand in enforced markets is not destroyed by regulation but concentrated among fewer, compliant operators.

The European Precedent: What Amsterdam, Barcelona, and Paris Taught Us

Amsterdam demonstrates the extreme case. Under a 30-night annual cap with proposals to reduce to 15 nights, the city maintains just 8,371 active listings but achieves a $313 ADR -- the highest among major European markets and 73% higher than Madrid's $181. Barcelona, facing a complete phase-out of all 10,101 tourist apartment licenses by November 2028, still generates $36,732 in median annual revenue per listing.

The parallel with Southeast Asia is structural, not coincidental:

- Singapore ($215 ADR, 1,240 listings) mirrors Amsterdam ($313 ADR, 8,371 listings) -- both represent near-ban environments where severe supply compression drives extreme ADR premiums

- Bangkok ($142 ADR, 28,450 listings) parallels Paris ($268 ADR, 59,421 listings) -- both enforce licensing requirements within high-demand tourism markets, resulting in above-average ADR without eliminating supply

- Jakarta ($72 ADR, 6,500 listings) resembles pre-enforcement European markets -- emerging regulation has not yet compressed supply or driven pricing premiums

Where SE Asia Diverges from the European Playbook

The parallels are strong, but Southeast Asia's enforcement wave differs from Europe's in three important ways.

First, enforcement infrastructure is fragmented. Europe is converging on a unified framework through EU Regulation 2024/1028, which standardizes host registration, platform data-sharing, and enforcement tools across 27 member states. Southeast Asia has no equivalent regional body -- ASEAN has not proposed harmonized STR regulation, and enforcement varies not just by country but by province, city, and even building-level strata management decisions.

Second, the informal economy is larger. In markets like Bangkok, Ho Chi Minh City, and Jakarta, a significant portion of STR activity operates outside any formal registration system. Tax compliance mechanisms are less developed than Europe's (Greece's AADE cross-referencing platform data with bank accounts remains far ahead of anything in Southeast Asia). This means supply compression from enforcement takes longer to materialize and is less consistent.

Third, tourism dependency creates political pressure. Bali's economy depends heavily on tourism -- far more than Amsterdam's or Barcelona's. This creates political resistance to aggressive enforcement that could reduce visitor accommodation options. The Pondok Wisata permitting system reflects this tension: it formalizes STR operations rather than restricting them, aiming to capture tax revenue and ensure safety standards without reducing supply.

These differences suggest Southeast Asian enforcement will follow a slower, more uneven trajectory than Europe's. But the economic fundamentals are identical: when regulation does compress supply, pricing and revenue for compliant operators rise.

What This Means for Hosts and Investors

The data from both regions supports a single strategic conclusion: compliance is a competitive moat, not a cost center.

For hosts currently operating in SE Asian markets: The enforcement trajectory is clear. Operators who obtain proper licensing, register with local authorities, and maintain tax compliance are positioning themselves on the right side of supply compression. As enforcement tightens -- and the regional trend is unambiguously toward tightening -- unlicensed competitors will exit. The remaining compliant supply absorbs demand at higher rates.

For investors evaluating SE Asian STR opportunities: Enforcement intensity should be a positive signal, not a deterrent. Singapore's $215 ADR and Bali's $28,400 annual revenue demonstrate that regulated markets can support strong returns. The key metrics to evaluate:

- Compliance cost vs. ADR premium -- What does licensing, registration, and tax compliance cost relative to the per-night pricing premium in enforced markets?

- Supply trend -- Is listing count stable, growing, or declining? Declining supply in the face of stable demand is the precursor to ADR increases.

- Enforcement trajectory -- Is the market moving toward stricter enforcement (Bangkok, HCMC) or maintaining the status quo? Early compliance in markets trending stricter offers first-mover advantage.

- Tourism demand resilience -- Markets with strong, diversified tourism demand (Bali, Bangkok, Singapore) sustain occupancy even as supply compresses. Single-source demand markets carry more risk.

Frequently Asked Questions

Short-term rentals under three consecutive months are effectively banned in Singapore's public housing (HDB flats) and restricted in private residential properties. The Urban Redevelopment Authority (URA) enforces minimum stay requirements. Violations carry fines up to SGD 200,000. AirROI data shows only approximately 1,240 active listings remain in Singapore, but those that operate compliantly achieve a $215 ADR -- the highest in Southeast Asia.

Thailand's Hotel Act (B.E. 2547) requires any property offering stays under 30 days to hold a hotel license. Enforcement has intensified in 2026, with the Department of Provincial Administration conducting inspections in high-tourism districts. Unlicensed operators face fines up to THB 40,000 and potential imprisonment. Compliant operators in Bangkok maintain a $142 ADR with 62% occupancy across approximately 28,450 active listings.

AirROI data shows Bali leads Southeast Asia in median annual revenue at $28,400 per listing, followed by Singapore at $26,100 and Bangkok at $22,800. Singapore achieves the highest ADR ($215) due to severe supply constraints, while Bali generates top revenue through a combination of $178 ADR and 67% occupancy driven by sustained international tourism demand.

The pattern is strikingly similar. Singapore's near-ban mirrors Amsterdam's approach -- both maintain the smallest supply (1,240 and 8,371 listings respectively) and the highest ADR ($215 and $313) in their regions. The key difference is infrastructure: European enforcement is increasingly centralized under EU Regulation 2024/1028's data-sharing framework, while Southeast Asian enforcement remains fragmented across national and local authorities.

No -- the data suggests the opposite. AirROI analysis of both European and Southeast Asian markets shows strict enforcement concentrates revenue among compliant operators rather than destroying markets. Singapore's $215 ADR and Bali's $28,400 annual revenue demonstrate that compliance creates a competitive moat. The key is selecting markets where you can operate within the legal framework and treating regulatory compliance as an operating cost rather than a barrier.