Spring Break 2026 Airbnb Data: Where Fill Rates Are Surging and What Hosts Should Do Now

Savannah hit 99% fill rate on March 27. South Padre Island reached 79% on March 19. Nashville crossed 77% the same weekend. Spring break 2026 Airbnb demand is generating concentrated booking spikes that rival -- and in some markets exceed -- summer season peaks. AirROI's real-time pacing data across 50,000+ active listings in 9 key markets reveals a sharply split landscape: traditional beach destinations are performing well, but the biggest surprises are coming from markets nobody pegged as "spring break towns." For hosts with remaining inventory, the data points to a narrow pricing window over the next 3 weeks. Here is exactly what the spring break short term rental data shows -- market by market, rate by rate, and day by day.

Spring Break 2026 Market Pacing: The Full Picture

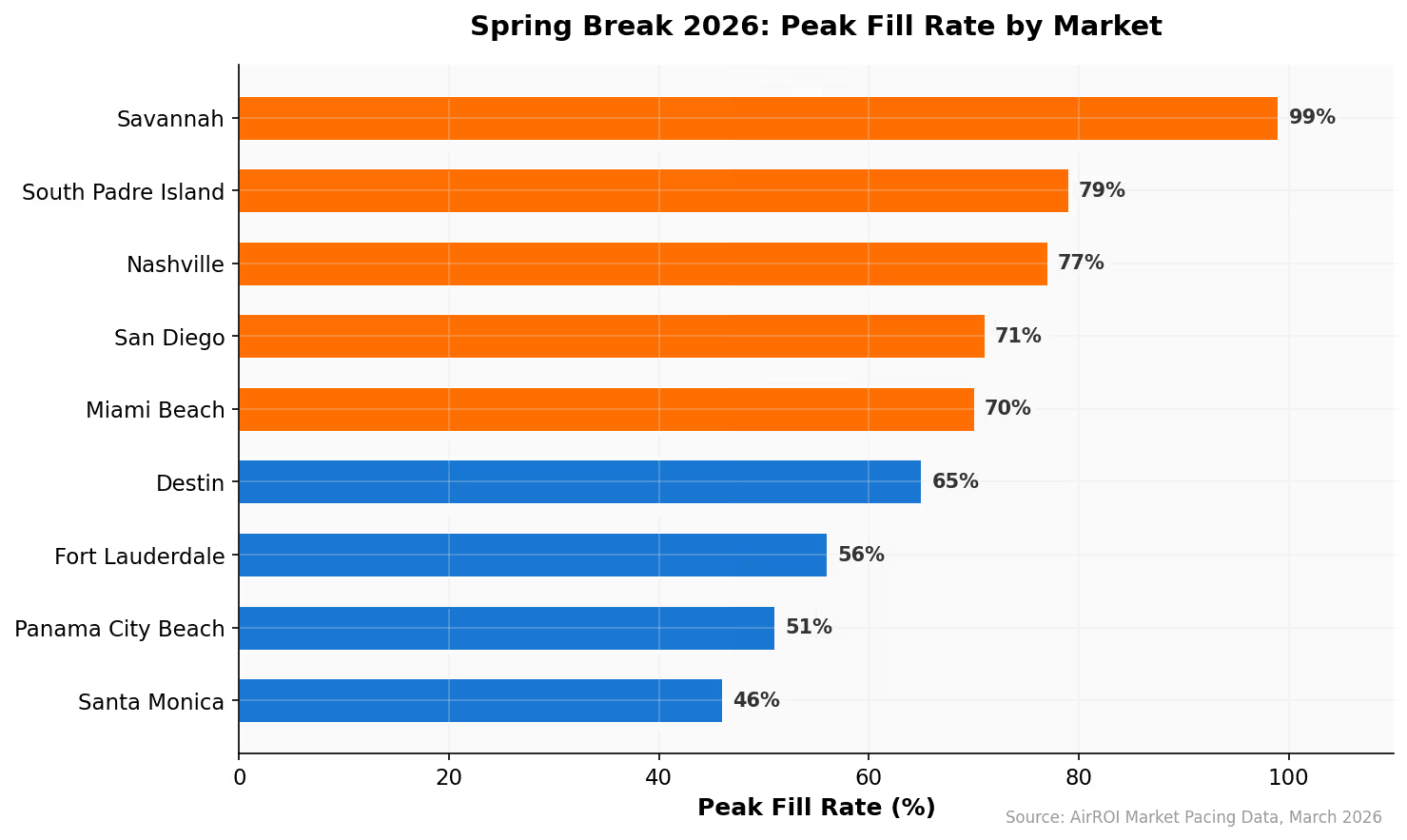

Savannah, Georgia posts the highest peak fill rate of any market AirROI tracks during spring break 2026 -- 99% on March 27, with 1,512 of 1,526 available listing-nights booked at an average rate of $403. That is not a typo. A city better known for its historic squares than its beach scene is outperforming every traditional spring break destination in the country.

Nashville follows at 77% fill rate on March 27, with booked rates averaging $424/night -- a 22% premium over its trailing twelve-month ADR of $347. Both markets share a pattern: weekend-heavy demand that compresses bookings into Friday-Saturday, creating sharp peaks that mask lower midweek occupancy.

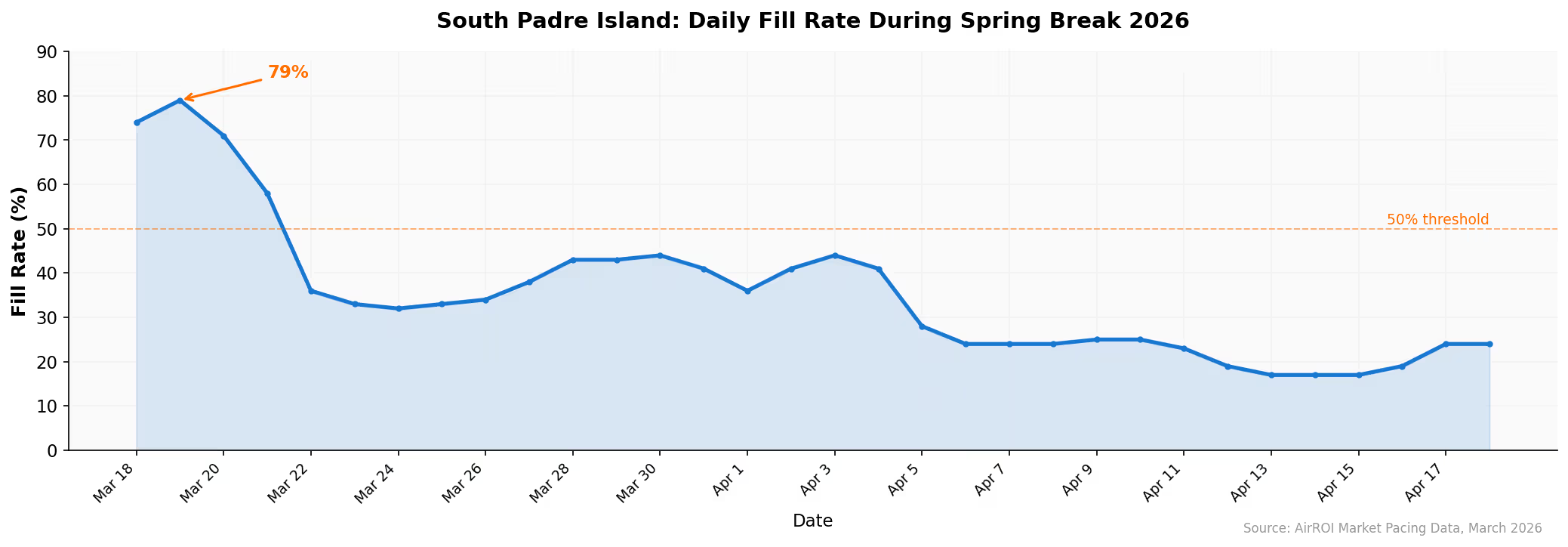

Among beach markets, South Padre Island leads at 79% fill rate on March 19, with 1,243 listings booked at $385/night. San Diego reaches 71% on March 20, and Miami Beach hits 70% on March 27 with the highest booked ADR of any market at $481/night.

| Market | Peak Date | Fill Rate | Booked ADR | Active Listings |

|---|---|---|---|---|

| Savannah, GA | Mar 27 | 99% | $403 | 2,564 |

| South Padre Island, TX | Mar 19 | 79% | $385 | 2,485 |

| Nashville, TN | Mar 27 | 77% | $424 | 6,845 |

| San Diego, CA | Mar 20 | 71% | $422 | 10,449 |

| Miami Beach, FL | Mar 27 | 70% | $481 | 4,528 |

| Destin, FL | Mar 18 | 65% | $510 | 3,985 |

| Fort Lauderdale, FL | Mar 20 | 56% | $435 | 3,987 |

| Panama City Beach, FL | Mar 18 | 51% | $382 | 10,418 |

| Santa Monica, CA | Mar 20 | 46% | $282 | 988 |

The pattern is clear: smaller markets with constrained supply (Savannah at 2,564 listings, South Padre at 2,485) hit higher fill rates faster. Large-inventory markets like Panama City Beach (10,418 listings) and San Diego (10,449) absorb demand without the same fill-rate spikes, which translates to more pricing power for hosts in supply-constrained markets.

Where Spring Break ADR Premiums Are Highest

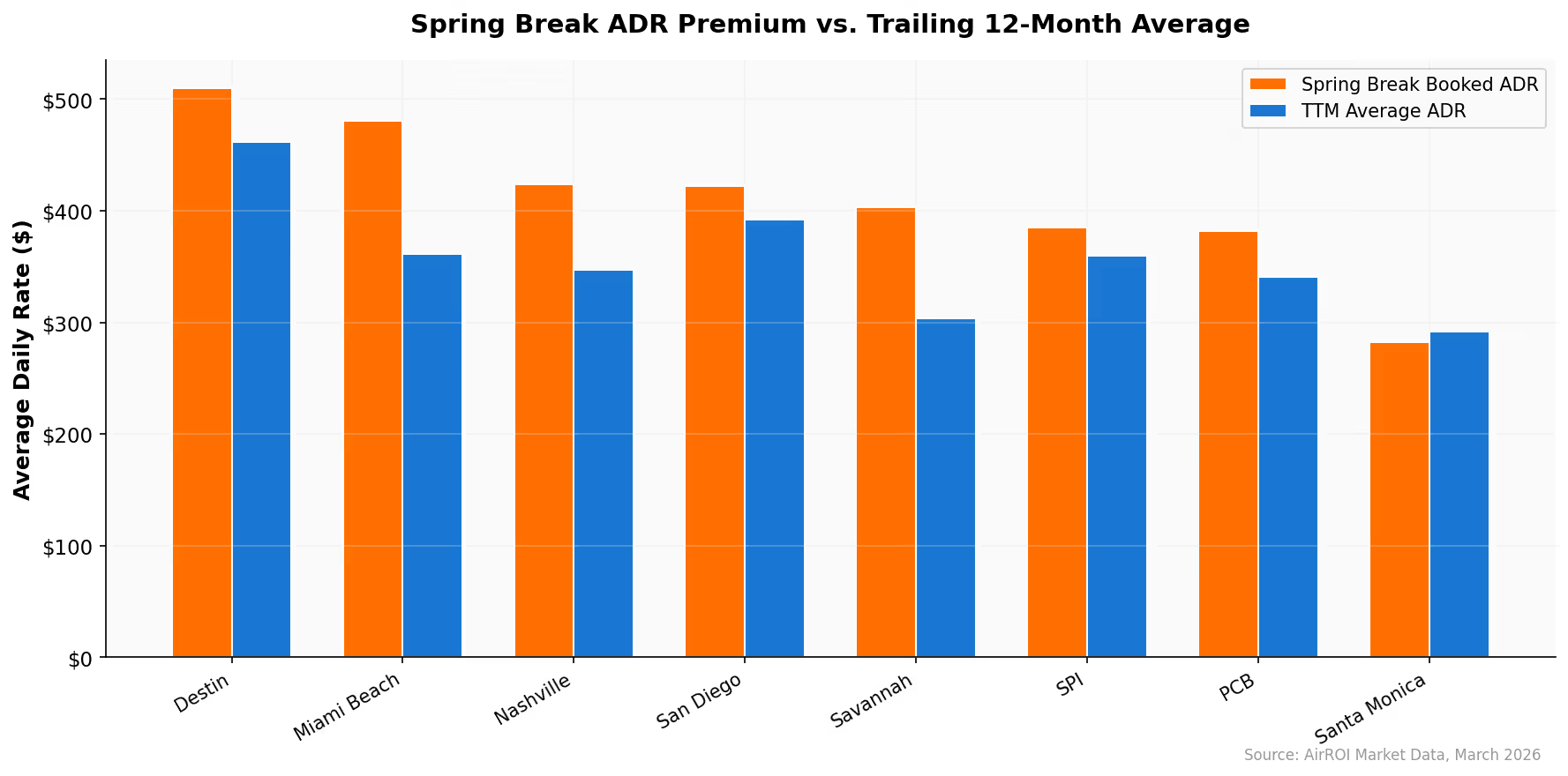

Destin commands the highest absolute spring break rate at $510/night for booked stays during peak week -- a 10% premium over its $462 trailing twelve-month ADR. But the largest percentage premiums appear in markets where spring break demand represents a seasonal outlier rather than the norm.

Savannah's spring break booked rate of $403 represents a 33% premium over its $304 TTM ADR, the widest gap of any market analyzed. Nashville's $424 spring break rate runs 22% above its $347 baseline. These are markets where spring break demand hits a supply base that is not calibrated for seasonal peaks the way Florida beach markets are.

| Market | Spring Break Booked ADR | TTM ADR | Premium |

|---|---|---|---|

| Savannah | $403 | $304 | +33% |

| Nashville | $424 | $347 | +22% |

| Destin | $510 | $462 | +10% |

| Miami Beach | $481 | $361 | +33% |

| South Padre Island | $385 | $360 | +7% |

| Panama City Beach | $382 | $341 | +12% |

| San Diego | $422 | $392 | +8% |

| Santa Monica | $282 | $292 | -3% |

Santa Monica is the only market where spring break booked rates actually trail the TTM average. This aligns with the market's identity as a year-round destination where spring break demand blends into normal seasonal flow rather than creating a distinct spike.

"Spring Break is the single biggest earning window of the year for short-term rental owners... an eight-week revenue machine that requires surgical precision to maximize." -- Emperor Rentals, Tampa Bay spring break analysis

For hosts in premium markets, the data reinforces holding firm on rates during peak dates. With Destin booked rates running $48/night above TTM and Miami Beach at $120/night above, discounting peak-demand nights leaves real money on the table.

The Booking Window Is Shrinking: Lead Time Data

Destin tells a different story. Its median lead time dropped from 57 days in October to 36 days in February, meaning the booking window for remaining spring break inventory is compressing fast. Guests who haven't booked yet are deciding within 3-5 weeks of check-in.

"Guests are booking later, with shorter booking windows meaning guests are deciding and committing closer to arrival. With booking windows this short, pricing needs to be dynamic and change daily." -- RedAwning, 2026 Short-Term Rental Market Forecast

What this means for the remaining weeks: the guests still booking spring break stays are last-minute decision-makers. They are less price-sensitive than early planners (they had months to compare) but more spontaneous. Hosts with available inventory should focus on visibility -- instant booking enabled, updated photos, competitive pricing relative to the available-rate average in their market -- rather than holding out for premium-rate guests who have already booked elsewhere.

Family Beaches vs. Party Towns: Two Pricing Playbooks

The spring break data splits cleanly into two demand profiles that require fundamentally different pricing strategies.

Party markets -- South Padre Island, Miami Beach, Panama City Beach -- show extreme fill-rate volatility. South Padre's fill rate swings from 79% on March 19 to 32% on March 24, a 47-point drop in five days. Miami Beach shows a similar pattern: 70% on the March 27 weekend collapsing to 36-38% by Monday-Tuesday. These markets generate intense, concentrated demand around peak dates with sharp midweek valleys.

Family markets -- Santa Monica, San Diego, Savannah -- show steadier, more predictable demand curves. Santa Monica maintains a 43-46% fill rate throughout the March 18-28 window with minimal daily swings. San Diego ranges from 45-71%, with the variation driven primarily by weekend vs. weekday rather than volatile week-to-week shifts.

| Dimension | Party Markets (SPI, Miami, PCB) | Family Markets (SM, SD, Savannah) |

|---|---|---|

| Fill rate volatility | High (47-point swings in 5 days) | Low (10-15 point range) |

| Avg length of stay | 4.3-5.1 days | 4.0-6.3 days |

| Weekend vs midweek gap | 20-30% fill rate differential | 10-15% differential |

| ADR premium over TTM | 7-33% | 0-33% |

| Pricing strategy | Aggressive weekend surge, midweek discounts | Stable rates, longer minimum stays |

The practical takeaway: if you host in a party market, your pricing should move daily. Surge pricing on Thursday-Saturday, discounted gap-fill rates Sunday-Wednesday. If you host in a family market, set a stable weekly rate with a 4-5 night minimum stay to match the 6.3-day average length of stay that family travelers prefer.

Florida Gulf Coast: Destin, Panama City Beach, and the Remaining Weeks

AirROI's pacing data shows a second wave building in Destin for March 28 through April 9. Fill rates for that window sit at 55-62%, with booked rates averaging $540-560/night. That is above the market's TTM ADR of $462, confirming that premium pricing remains viable for the second half of spring break.

Fort Lauderdale and Miami Beach show strong late-March performance. Miami Beach's fill rate hits 59% on March 26, climbing to 70% by March 27-28. Booked rates during that surge average $463-481/night, driven by a combination of college spring breakers and international tourists. The market's 4,528 active listings provide enough supply to prevent the fill-rate extremes seen in smaller markets.

How to Price the Remaining Spring Break Weeks

The data points to a clear framework for pricing the final 3 weeks of spring break 2026, based on your market's current fill rate for specific dates.

Fill Rate Above 60%: Hold or Increase

Markets like Destin (55-62% for late March), Savannah (51-54% for early April), and Nashville (55-57% for upcoming weekends) still have pricing power. If your listing is priced near the available-rate average, consider increasing 5-10% for remaining peak dates. AirROI data shows booked rates in Destin are running $50-70/night above available rates, meaning guests are selecting higher-priced listings first.

Fill Rate 40-60%: Maintain and Optimize

Miami Beach, San Diego, and Fort Lauderdale fall in this band for the March 28-April 11 window. Maintain current pricing but reduce minimum night stays from 5+ to 3 nights to capture shorter bookings. Review your listing for instant book status -- last-minute travelers overwhelmingly prefer instant confirmation.

Fill Rate Below 40%: Capture the Gap

A broader trend underlies these market-level patterns: according to RetailMeNot, 61% of Americans plan to travel this spring break (up from 48% last year), but average trip spending dropped 11% to $1,219. More travelers, smaller budgets. That favors midrange STR properties over premium ones and rewards hosts who price competitively rather than aspirationally.

Frequently Asked Questions

Savannah leads all markets with a 99% fill rate on March 27, followed by South Padre Island at 79% (March 19), Nashville at 77% (March 27), San Diego at 71% (March 20), and Miami Beach at 70% (March 27). These figures come from AirROI's real-time pacing data across 50,000+ active listings.

Spring break ADR premiums range from 5% to 33% above trailing twelve-month averages. Destin commands the highest absolute rate at $510/night (10% over its $462 TTM ADR), while Savannah shows the largest percentage premium at 33% ($403 spring break vs $304 TTM). Nashville's peak weekend rate of $424 represents a 22% premium.

No. Even top-demand markets have remaining inventory for late March and April dates. Destin has 2,700+ available listings for the March 28-April 9 window, Panama City Beach has 7,800+, and Miami Beach has 3,100+. Booking lead times are compressing, meaning last-minute guests represent real demand. List now and price competitively to capture the final spring break waves.

Set minimum stays based on your market's average length of stay and current fill rates. Santa Monica averages 6.3-day stays (set 4-5 night minimum for peak dates), while Nashville averages 3.8 days (2-3 night minimum works). For any dates within 10 days with fill rates below 40%, drop to 2-night minimums to capture gap-fill bookings.

AirROI's Atlas tool provides free market-level pacing data showing daily fill rates, average booked and available rates, and active listing counts for any US market. Enter your city to see exactly how spring break demand is trending and benchmark your pricing against competitors in real time.