Airbnb Hotels 2026: Which STR Hosts Face Real Competition (and Which Don't)

Airbnb's hotel vertical is growing 2x the rest of the business -- and 55% of guests who book a hotel on the platform come back to book a home. Those two data points, buried in Airbnb's Q1 2026 earnings call, tell a more nuanced story than the "Airbnb adds hotels, hosts lose" headlines suggest. AirROI data across six markets reveals that the competitive threat from airbnb hotels 2026 concentrates on one specific listing segment while leaving most hosts untouched. The question is not whether hotels on Airbnb are growing. It is whether that growth takes your guests or brings new ones.

What Airbnb's Hotel Push Actually Looks Like in 2026

The inventory is deliberately curated. Airbnb targets boutique and independent hotels exclusively -- not Marriotts or Hiltons. Independent hotels face higher OTA commissions and lack franchise loyalty programs, making Airbnb an appealing distribution channel. The platform is not trying to out-Booking Booking.com. It is filling specific gaps.

CEO Brian Chesky added the strategic ambition: hotels could become a "multibillion-dollar revenue business." He teased further announcements at the May 20, 2026 Summer Release, and hiring data shows hotel-specific roles open in Tokyo, Sydney, and Singapore -- signaling Asia-Pacific expansion of the hotel vertical beyond its US and European pilot markets.

CFO Mertz's Three Reasons -- and What Each Means for Hosts

Mertz laid out the strategic logic in three parts. Understanding each one clarifies where the competitive pressure actually lands.

"It allows us to satisfy demand in markets where we do not have sufficient supply. Second, it allows us to fill in travel nights when a hotel is a better offering. Third, having hotels on the platform is a nice onboarding ramp for global travelers." -- Ellie Mertz, CFO, Airbnb, Q1 2026 Earnings Call

Reason 1: Fill supply gaps in regulation-constrained markets. Hotels serve demand where STR hosts legally cannot operate. In NYC, where Local Law 18 wiped out thousands of non-compliant listings, hotel inventory plugs the hole. This is not competitive with existing hosts -- it captures demand that would otherwise go to Booking.com or Expedia. For compliant hosts in these cities, hotels may actually boost platform traffic and brand visibility.

Reason 2: Cover trip types where a hotel is the better product. Last-minute one-night stays, solo business travel, and airport layovers are use cases where hotels win structurally. Most STR hosts do not want one-night bookings -- the turnover cost makes them unprofitable. This reason is largely incremental demand that STR hosts were not capturing anyway.

Reason 3: Onboard new guests via hotels. This is the stat that matters most for hosts:

"Over 55% of people who book a hotel on the platform come back to book a home." -- Ellie Mertz, CFO, Airbnb, Q1 2026 Earnings Call

If the 55% return rate holds at scale, hotels function as a guest acquisition funnel for the STR ecosystem. The business traveler who discovers Airbnb through a hotel booking in Madrid returns six months later to book a villa in Tulum with their family. Net effect: more guests in the STR pipeline, not fewer.

The competitive overlap is narrow: only Reason 2 creates direct competition, and only for urban listings that compete on the same convenience/price proposition as boutique hotels. For 2 of 3 stated reasons, hotels are demand-additive.

The Competitive Overlap Zone: AirROI Data from 6 Markets

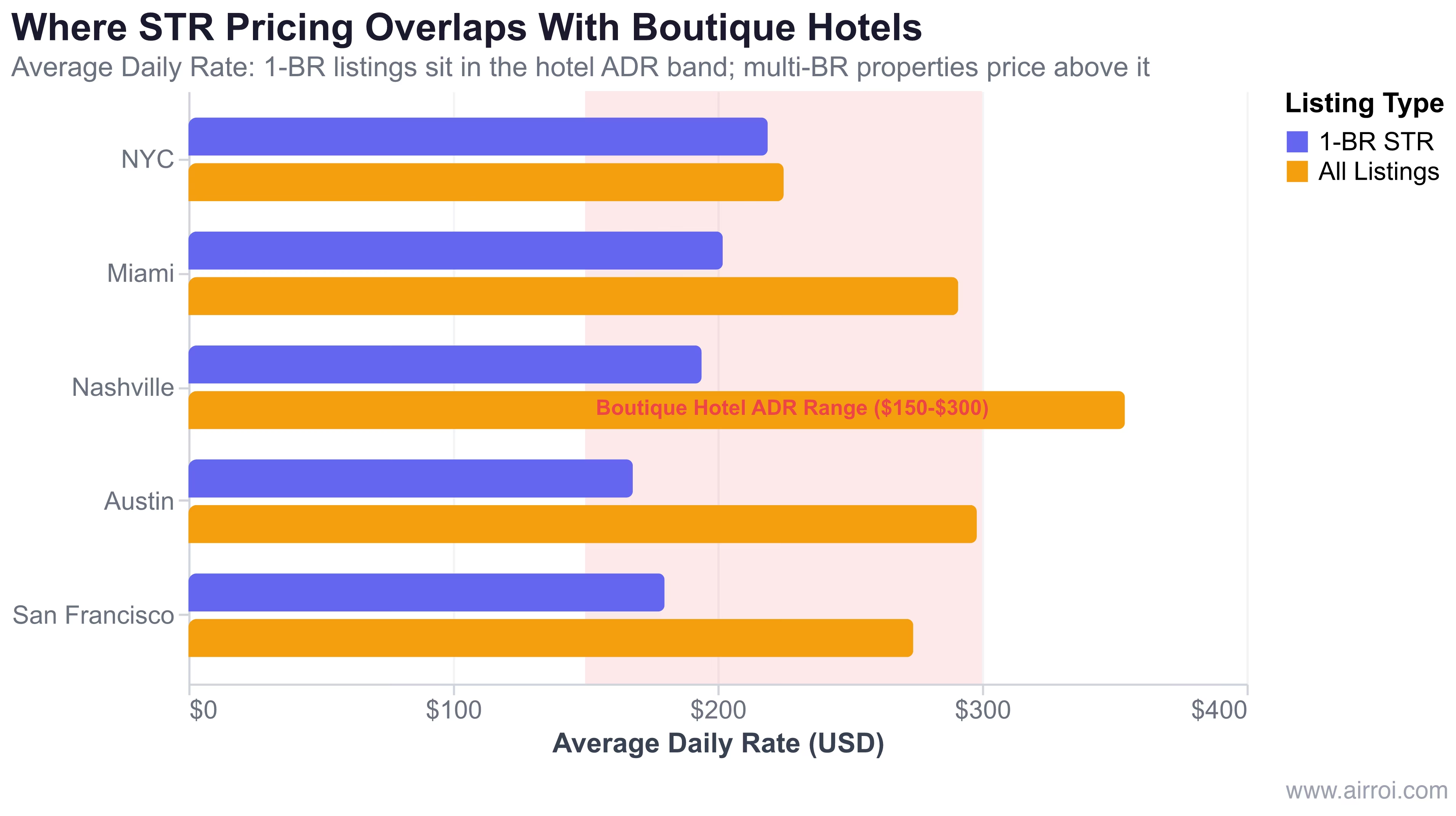

Theory is useful. Data is better. AirROI analyzed STR performance metrics across six markets where Airbnb is actively scaling airbnb hotel listings -- filtering for 1-bedroom properties to isolate the segment most exposed to hotel competition.

| Market | 1-BR ADR | All-Listing ADR | 1-BR Occupancy | 1-BR Revenue | Active 1-BR Listings |

|---|---|---|---|---|---|

| NYC | $219 | $225 | 46% | $19,297 | 3,888 |

| Miami | $202 | $291 | 50% | $25,049 | 3,088 |

| Nashville | $194 | $354 | 49% | $25,559 | 1,646 |

| Austin | $168 | $298 | 44% | $29,474 | 8,774* |

| San Francisco | $180 | $274 | 55% | $33,932 | 4,355* |

| Madrid | $127 | $181 | 56% | $25,352 | 17,026* |

*Austin, SF, and Madrid figures reflect all-listing counts; 1-BR subset is a portion of total.

The pattern is clear. 1-BR STR ADRs range from $127 to $219 -- sitting squarely in the $150-$300 pricing band where boutique hotels operate. These listings compete on the identical value proposition: a convenient urban location for a short stay.

The broader industry metrics reinforce the overlap:

| Metric | US Hotels | US STRs | Source |

|---|---|---|---|

| Occupancy Rate | ~63% | ~50% | CBRE / Engine.com |

| ADR Trend (2026) | Stable | +1.5% YoY | CBRE / AirDNA |

| RevPAR Growth | -0.6% (H2 2025) | +5-6% | CBRE / Engine.com |

| Supply Change | -4% urban | +4.6% total | AirDNA |

Hotels command higher absolute occupancy (63% vs. 50%), but STRs are growing RevPAR faster. The convergence zone is where these two lines cross -- urban 1-BR listings that compete on convenience and price against hotels that now appear in the same Airbnb search results.

Which STR Hosts Are Structurally Insulated

The data also reveals which hosts can disregard the hotel headlines entirely. The insulation factors are structural, not strategic -- hotels simply cannot serve these segments.

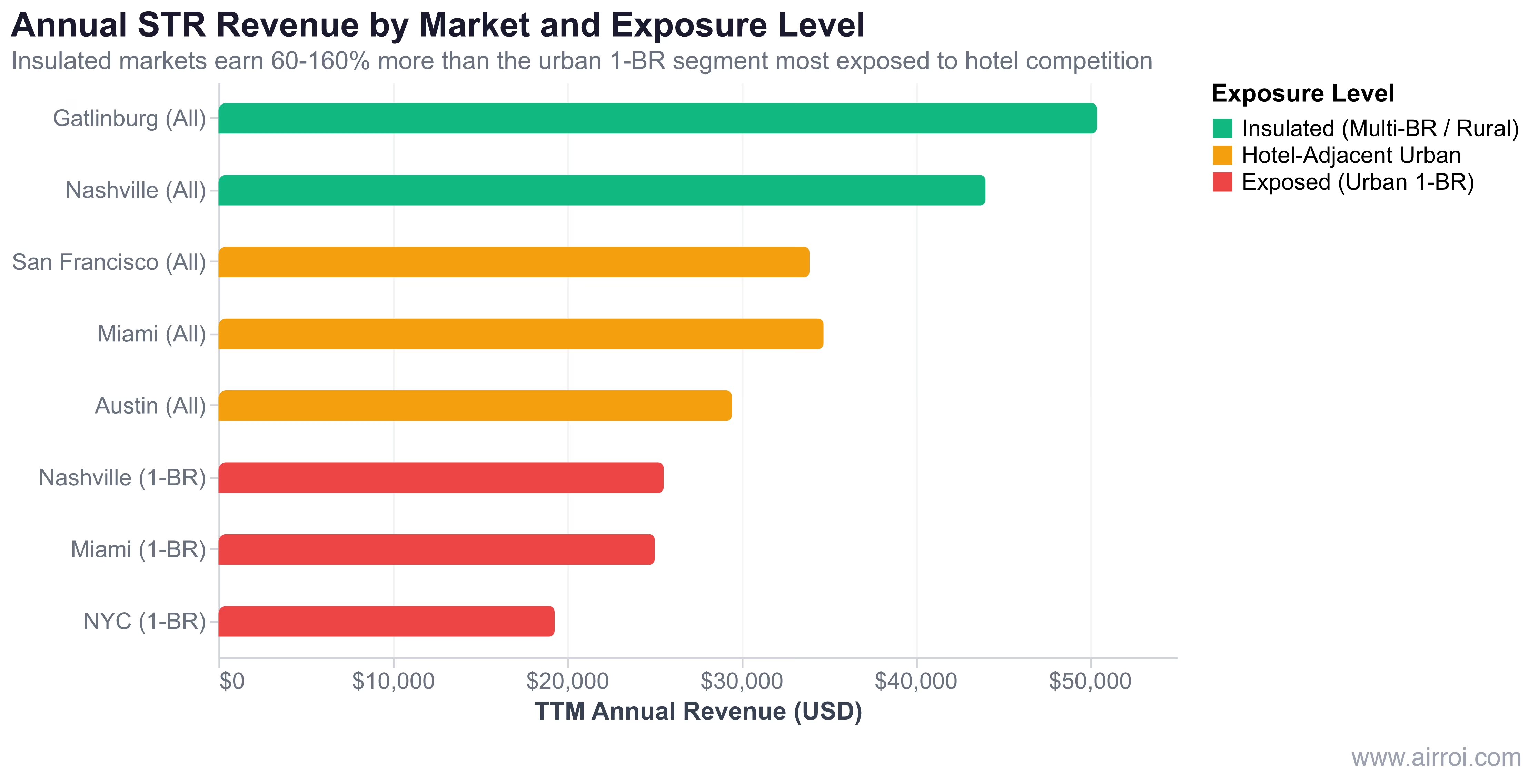

Gatlinburg, TN earns a $377 ADR and $50,438 in annual revenue per listing across 3,622 active properties. The entire value proposition -- Smoky Mountains cabins with hot tubs, game rooms, and mountain views -- has zero hotel equivalent on Airbnb. Hotels solve urban convenience problems. Cabins solve experiential travel demands. These are different products serving different guests.

Nashville's broader market (all bedroom types) achieves a $354 ADR and $44,039 annual revenue -- 72% more than its own 1-BR segment ($25,559). The premium comes from 3+ bedroom properties serving bachelorette parties, family reunions, and group travel. A boutique hotel cannot accommodate eight guests who want to cook together, play yard games, and split $354 per night six ways.

Four structural insulation factors:

- Group capacity (3+ bedrooms). Half of all nights booked on STR platforms are for stays of a week or longer, often by groups. Hotels cannot serve a family of eight sharing a house.

- Unique architecture. Treehouses, A-frames, converted barns, and houseboats have no hotel analogue. These listings win on distinctiveness, not convenience.

- Rural and nature destinations. Rural STR supply is growing 23% year-over-year, but hotels are not entering Gatlinburg, Broken Bow, or Big Bear. The economics do not support it.

- Extended-stay amenities. Full kitchens, laundry, and dedicated workspaces serve the 30-day digital nomad in ways a hotel room with a minibar never will.

If your listing checks two or more of these boxes, hotel expansion on Airbnb is not your competitive problem. Supply growth from other STR operators is.

The Differentiation Playbook for Exposed Hosts

Urban 1-BR hosts facing direct hotel competition on Airbnb need a deliberate response -- not panic, but strategy.

Lean into the space advantage. A 1-BR apartment offers what a hotel room structurally cannot: a full kitchen, a living room, in-unit laundry, and a separate sleeping area. For stays of 3+ nights, these amenities deliver tangible guest savings on dining and services. Emphasize them in your listing title and first photo.

Target the extended-stay segment. Nashville's 1-BR average length of stay is 3.9 nights. Guests booking 5-7+ nights are choosing STRs precisely because hotels become prohibitively expensive for longer stays. Offer weekly discounts and monthly rates to capture this segment that hotels serve poorly.

Invest in review quality and Superhost status. With 800+ factors influencing Airbnb search visibility and AI-driven personalization becoming the core search strategy, review velocity and quality are the strongest ranking signals a host controls. Hotels start with zero reviews on Airbnb. Your review history is a competitive moat -- protect it with hospitality that matches or exceeds hotel standards.

"Our competition is hotels. If a guest treats your property as they would a hotel, that is wholly appropriate. Like it or not, you are in the hospitality business, be hospitable." -- Multi-property host on r/airbnb_hosts (28,000+ upvotes)

Watch the fee structure. Over 25% of active Airbnb listings have migrated to the 15.5% single host service fee, replacing the old split-fee model. This effectively raises the guest-visible price of STRs relative to hotels on the platform. Hosts need to account for this when benchmarking their rates against hotel room rates in the same search results.

Diversify distribution. The arrival of hotels on Airbnb reinforces a broader trend: platform dependence is risk. Seventy percent of STR operators now have a direct-booking website, but nearly two-thirds still generate less than 25% of bookings through direct channels. Hosts who build guest email lists, list on multiple platforms, and develop repeat-guest relationships are insulated from any single platform's strategic shifts.

Frequently Asked Questions

For most hosts, no. Hotel inventory on Airbnb targets urban supply gaps in regulation-restricted cities like NYC, SF, LA, and Madrid. AirROI data shows the direct competitive overlap is limited to urban 1-BR listings with $194-$219 ADRs that sit in the same pricing band as boutique hotels. Hosts with 2+ bedrooms, unique properties, or non-urban locations face no measurable hotel competition.

Hotel room nights on Airbnb are growing more than 2x the rest of the business, according to CFO Ellie Mertz on the Q1 2026 earnings call. Despite that growth rate, hotels still represent a single-digit percentage of total nights booked, so the absolute numbers remain small relative to Airbnb's 8+ million global listings.

Urban markets with high concentrations of 1-BR and studio listings face the most pressure. AirROI data shows NYC (3,888 one-bedroom listings at $219 ADR), Miami (3,088 at $202 ADR), and Nashville (1,646 at $194 ADR) sit in the direct competitive path of boutique hotel pricing between $150-$300 per night.

Differentiate on what hotels cannot offer: full kitchens, in-unit laundry, living space, flexible cancellation policies, and local neighborhood character. Shift target guest segments from solo business travelers toward couples, remote workers, and extended-stay guests. Invest in Superhost status, review quality, and dynamic pricing to avoid racing to the bottom on nightly rate.

Unlikely for most hosts. CFO Mertz stated that 55% of hotel bookers return to book a home on Airbnb, suggesting hotels expand the overall guest pool rather than redistribute existing demand. However, in urban markets where 1-BR STRs and hotels compete head-to-head on price and convenience, some occupancy pressure is possible.