Airbnb Rental Arbitrage 2026: 9 Markets Exposed -- Where the Margins Still Work

Airbnb rental arbitrage -- leasing a property long-term and subletting it as a short-term rental -- still works in 2026. But the gap between markets where it works and markets where it destroys capital has never been wider.

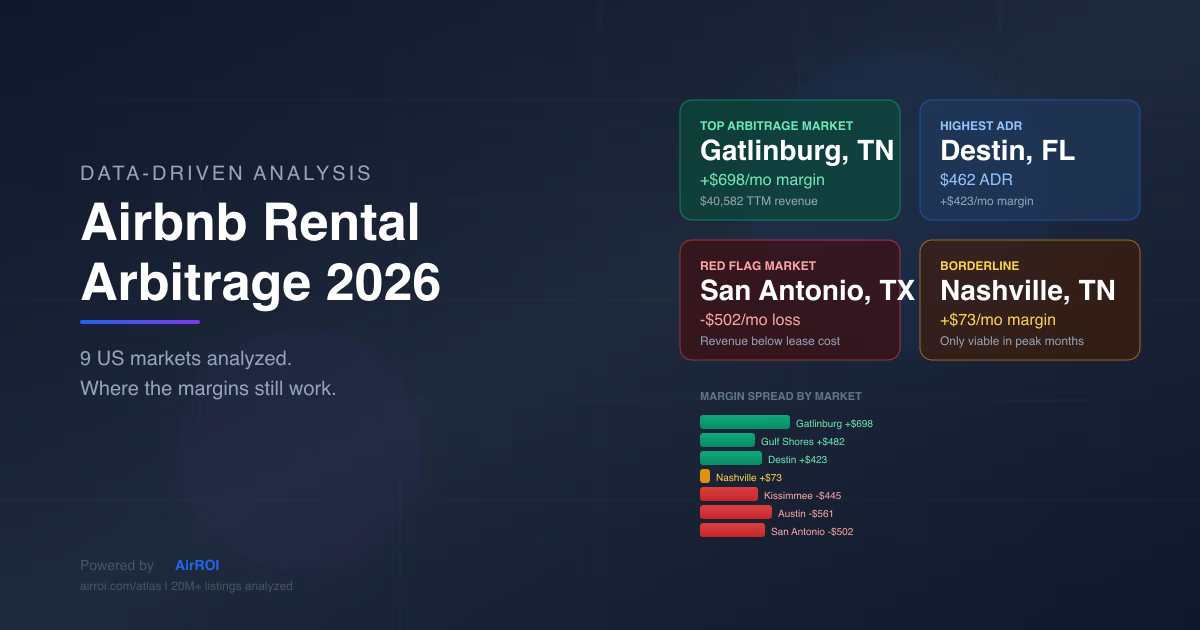

We pulled AirROI data for 9 popular US arbitrage markets -- Nashville, Scottsdale, Gulf Shores, Gatlinburg, Destin, San Antonio, Kissimmee, Myrtle Beach, and Austin -- and overlaid estimated lease costs to find which cities still pencil out. The results are stark: only 3 markets produce reliable positive margins. Here is the full breakdown.

What Rental Arbitrage Is and Why 2026 Conditions Favor It

Rental arbitrage is straightforward: you sign a long-term lease on a property (typically 12 months), furnish it, and list it on Airbnb or VRBO as a short-term rental. The bet is that nightly STR revenue exceeds your monthly rent plus operating costs, generating profit without property ownership.

Three 2026 conditions make the arbitrage window wider than it has been in years:

STR revenue is stabilizing. After two years of compression from pandemic-era highs, ADR is projected to grow 1.5% in 2026 according to AirDNA. Supply growth has decelerated to 4.6% -- a fraction of the 20%+ annual expansion in 2021-2022. Less new supply means less downward pressure on occupancy.

The spread is what matters. When rent growth slows but STR revenue holds steady (or grows), the gap between income and expenses widens. That is exactly the environment we are entering in 2026 -- but only in markets where STR demand fundamentals are strong enough to sustain above-average revenue per listing.

The Unit Economics: How to Calculate an Arbitrage Deal

Every arbitrage deal reduces to one formula:

Monthly STR Revenue - Monthly Rent - Operating Costs = Net Margin

Operating costs for a furnished short-term rental typically run 30-40% of gross revenue. This includes:

- Airbnb service fees: 3% host fee (or 14-16% if using split-fee pricing)

- Cleaning costs: $75-$150 per turnover, the single largest variable expense

- Utilities: $150-$300/month (electricity, water, internet, streaming)

- Insurance: $50-$100/month for short-term rental coverage

- Supplies: $50-$100/month (toiletries, linens replacement, consumables)

- Furnishing amortization: $150-$250/month (spreading $5K-$15K initial investment over 3-5 years)

- Maintenance/repairs: $50-$100/month reserve

The 2.5x rule of thumb: For a deal to produce a viable margin, your monthly STR revenue should be at least 2.5 times your monthly lease payment. At $1,500/month rent, you need $3,750/month in STR revenue to cover rent, 35% operating costs, and still leave a reasonable margin. Below 2x, you are almost certainly losing money.

9 US Markets Analyzed: Revenue vs. Lease Cost

| Market | ADR | Occupancy | Monthly Revenue | 2BR Lease | Operating Costs (35%) | Net Margin |

|---|---|---|---|---|---|---|

| Gatlinburg, TN | $367 | 48% | $3,382 | $1,500 | $1,184 | +$698 |

| Gulf Shores, AL | $405 | 43% | $2,896 | $1,400 | $1,014 | +$482 |

| Destin, FL | $462 | 44% | $3,266 | $1,700 | $1,143 | +$423 |

| Nashville, TN | $347 | 47% | $2,882 | $1,800 | $1,009 | +$73 |

| Scottsdale, AZ | $413 | 49% | $2,854 | $1,900 | $999 | -$45 |

| Kissimmee, FL | $275 | 51% | $2,084 | $1,800 | $729 | -$445 |

| Myrtle Beach, SC | $247 | 42% | $1,469 | $1,400 | $514 | -$445 |

| San Antonio, TX | $207 | 45% | $1,305 | $1,350 | $457 | -$502 |

| Austin, TX | $294 | 45% | $1,753 | $1,700 | $614 | -$561 |

Source: AirROI market analytics, TTM as of March 2026. Monthly revenue = TTM revenue / 12. Lease costs from Zillow median 2BR rents. Operating costs estimated at 35% of gross revenue.

The pattern is clear: tourism-driven markets with moderate lease costs produce viable arbitrage margins, while urban markets with high listing counts and moderate ADR do not.

The Winners: Top Arbitrage Markets for 2026

Gatlinburg, TN -- The Arbitrage Sweet Spot

Gatlinburg produces the highest arbitrage margin of any market we analyzed at +$698/month net profit per unit. The math works because Great Smoky Mountains tourism drives a $367 ADR and 48% occupancy -- producing $40,582 in TTM revenue per listing -- while 2-bedroom lease costs remain around $1,500/month in the broader Sevier County area.

With just 3,787 active listings (compared to Nashville's 6,845), Gatlinburg avoids the oversupply pressure that compresses margins in larger metros. Regulation is minimal: Tennessee does not restrict STR subletting at the state level, and Sevier County operates with a permissive framework.

The risk is seasonality. Gatlinburg's monthly revenue swings from a peak of $7,740 in December (holiday cabin demand) and $7,439 in October (fall foliage) down to $2,982 in February. That means 2-3 months per year will likely run below breakeven -- you need the peak months to carry the annual total.

Gulf Shores, AL -- Affordable Leases, Strong Beach Revenue

Gulf Shores delivers +$482/month net margin driven by the lowest lease costs in our analysis ($1,400/month for a 2-bedroom) paired with $405 ADR from beach tourism. The 5,195-listing market is sizable but spread across the Alabama Gulf Coast, and regulation is permissive -- Baldwin County does not restrict short-term rental subletting.

The 68.4-day average booking lead time (the longest in our dataset) reveals that Gulf Shores caters to planned family vacations booked weeks in advance. This is actually favorable for arbitrage operators: longer lead times mean more predictable occupancy and less reliance on last-minute bookings.

Summer months (June-August) drive 55-65% occupancy, while winter drops to 25-30%. Budget for 3-4 negative months in the off-season.

Destin, FL -- High ADR Carries the Margin

Destin commands the highest ADR in our analysis at $462 -- a reflection of Emerald Coast premium pricing. Combined with 44% occupancy, that produces $39,186 in TTM revenue and a +$423/month net margin after a $1,700 lease and 35% operating costs.

The 4.9-day average length of stay and 64.7-day booking lead time confirm this is a planned-vacation market with lower turnover than urban destinations. Fewer turnovers mean lower cleaning costs per dollar of revenue -- a structural advantage for arbitrage operators.

Destin's risk is concentrated revenue: summer months can produce $5,000-$7,000+ while winter months drop below $2,000. Investors must stress-test against worst-month scenarios.

The Borderline Cases

Scottsdale, AZ shows a -$45/month loss at average performance, but its extreme seasonality creates an interesting dynamic. Scottsdale's March revenue averages $10,316 per listing -- nearly 3x the summer months. An arbitrage operator who signs a lease timed to capture winter/spring season (October-April) and sublets or vacates for summer could potentially make the math work. But at $1,900/month in lease costs, the margin for error is razor-thin.

The Red Flags: Markets Where Arbitrage No Longer Works

San Antonio, TX -- Revenue Below Lease Cost

San Antonio is the clearest arbitrage trap in our dataset. At $207 ADR and 45% occupancy, the average listing produces just $1,305/month in revenue -- which is $45 less than the median lease cost before you even account for operating expenses. With 5,891 active listings saturating the market and no major seasonal demand spike, San Antonio's STR revenue simply cannot support an arbitrage operation at current lease rates.

Myrtle Beach, SC -- Oversupply Crushing Margins

Myrtle Beach's 8,146 active listings make it one of the most oversaturated STR markets in America relative to demand. The result: $247 ADR and 42% occupancy produce just $1,469/month in revenue. After $1,400 in rent and $514 in operating costs, operators lose $445/month on every unit. The volume of listings has driven a race to the bottom on pricing.

Austin, TX -- The Poster Child for Margin Compression

Austin's once-vibrant arbitrage market has been crushed by a combination of 9,964 active listings (double Scottsdale's supply in a city with lower tourism demand) and $1,700 lease costs. At $294 ADR and 45% occupancy, the average listing generates $1,753/month -- barely covering the lease, with nothing left for the 35% operating cost load. The -$561/month loss makes Austin one of the worst arbitrage markets in the country.

Revenue Seasonality: The Hidden Risk in Arbitrage Math

Annual averages can mask the reality of month-to-month cash flow. Arbitrage operators pay rent 12 months a year, but STR revenue fluctuates dramatically by season.

Key insights from the seasonality data:

- Gatlinburg peaks in October ($7,439) and December ($7,740) but drops to $2,982 in February -- a 61% swing from peak to trough

- Scottsdale has the most extreme seasonality: $10,316 in March versus $4,004 in July -- a 61% decline in summer

- Nashville is the most consistent, ranging from $3,182 (January) to $6,318 (October) -- still a significant 50% swing but more manageable than beach and mountain markets

Regulatory Risk by Market

Arbitrage adds a regulatory layer beyond standard STR investing: you need both STR legality and landlord permission to sublet. Here is the regulatory landscape for each market:

| Market | STR Regulation | Subletting | Key Restrictions |

|---|---|---|---|

| Gatlinburg, TN | Low | Generally allowed | State-level permissive framework; county business license required |

| Gulf Shores, AL | Low | Generally allowed | Baldwin County permits required; no STR subletting ban |

| Destin, FL | Medium | Landlord dependent | Okaloosa County requires STR registration; Florida law preempts local STR bans |

| Nashville, TN | Medium | Restricted by zone | Permit required; non-owner-occupied permits limited in residential zones |

| Scottsdale, AZ | Low | Generally allowed | Arizona preempts local STR bans; city requires TPT tax license |

| San Antonio, TX | Medium | Landlord dependent | Type 2 STR license required for non-owner-occupied; no subletting-specific ban |

| Kissimmee, FL | Medium | Landlord dependent | Osceola County STR registration; HOA restrictions common in resort communities |

| Myrtle Beach, SC | Medium | Landlord dependent | City requires STR business license; zoning restrictions in some areas |

| Austin, TX | High | Restricted | Type 2 STR license required; density limits in residential zones; politically uncertain |

The safest arbitrage markets for regulatory risk are Gatlinburg, Gulf Shores, and Scottsdale -- all three operate under state frameworks that preempt aggressive local restrictions. Nashville and Austin carry the highest regulatory uncertainty for arbitrage operators.

Getting Started: From Research to First Booking

If the data points to a viable market, here is the practical path from research to revenue:

Step 2: Negotiate with landlords. Transparency is non-negotiable. Disclose your intent to operate a short-term rental and offer landlords incentives: higher monthly rent (10-15% premium), larger security deposits, or quarterly property inspections. Get subletting permission in writing as a lease addendum.

Step 3: Budget for furnishing. A 2-bedroom unit typically costs $5,000-$15,000 to furnish for Airbnb guests. Budget $3,000-$5,000 for furniture (bed frames, mattresses, sofa, dining set), $1,000-$2,000 for kitchen/bath essentials, and $1,000-$3,000 for decor, linens, and smart home devices. Amortize this over 3-4 years when calculating your monthly operating costs.

Step 4: Optimize your listing before launching. Professional photography ($200-$500), a keyword-optimized title, and competitive initial pricing (10-15% below market for the first 30 days to generate reviews) are essential for fast ramp-up.

Timeline: Expect 4-8 weeks from lease signing to first booking -- 1-2 weeks for furnishing, 1 week for professional photos and listing creation, and 1-4 weeks for booking ramp-up. Your first 60 days will likely run below average revenue as the listing builds review history and algorithmic ranking.

Frequently Asked Questions

Yes, but only in select markets. AirROI data shows 3 out of 9 major US markets still produce positive arbitrage margins after operating costs: Gatlinburg, TN (+$698/mo), Gulf Shores, AL (+$482/mo), and Destin, FL (+$423/mo). Markets like San Antonio, Austin, and Myrtle Beach now lose money because average STR revenue no longer covers lease plus operating costs. The key threshold: monthly STR revenue must be at least 2.5x your monthly lease for viable margins.

Typical startup costs for a 2-bedroom rental arbitrage unit run $7,000-$18,000. This includes first month's rent plus deposit ($2,800-$3,800), furnishing and supplies ($5,000-$15,000), professional photography ($200-$500), and initial supplies ($300-$500). Some operators reduce furnishing costs to $3,000-$5,000 by sourcing from Facebook Marketplace and estate sales. You should also have 2-3 months of operating reserves to cover the ramp-up period before bookings stabilize.

A healthy arbitrage margin is 15-25% of gross STR revenue after all costs (rent, cleaning, supplies, Airbnb fees, utilities, insurance, and furnishing amortization). In dollar terms, the top arbitrage markets produce $400-$700 per month net profit per unit. Margins below 10% are too thin to absorb unexpected vacancies or maintenance costs. The rule of thumb: your monthly STR revenue should be at least 2.5 times your monthly lease payment.

Based on AirROI's analysis of TTM revenue versus lease costs, the best US cities for rental arbitrage in 2026 are Gatlinburg, TN (highest margin at +$698/mo with $40,582 annual revenue and low regulation), Gulf Shores, AL (+$482/mo with affordable $1,400 leases), and Destin, FL (+$423/mo with $462 ADR). These markets share low lease costs relative to STR revenue, manageable regulation, and strong tourism demand.

The five biggest risks are: (1) Regulatory changes -- cities can ban or restrict STR subletting mid-lease, leaving you locked into a lease without rental income. (2) Seasonality -- markets like Gatlinburg and Destin earn 60-70% of annual revenue in just 4-5 peak months, meaning 3-4 months may run at a loss. (3) Landlord termination -- even with permission, landlords can decline to renew leases. (4) Oversupply -- markets with 5,000+ active listings face downward pressure on ADR and occupancy. (5) Operating cost creep -- cleaning costs, Airbnb fee increases, and turnover expenses can erode slim margins quickly.