While Cities Crack Down on Airbnb, These 3 States Just Opened the Door

The dominant narrative in short-term rental regulation during 2026 is one of tightening restrictions — NYC levying $72 million in STR fines, Sacramento imposing a primary residence rule, Barcelona phasing out tourist apartment licenses entirely. But in March 2026, three U.S. states moved in the opposite direction simultaneously. Indiana's legislature passed a rental cap ban 91-3. Idaho's governor signed one of the most sweeping state short-term rental preemption laws in the country. And Pennsylvania introduced its first-ever uniform STR framework. AirROI data across 12 markets in these three states — representing 14,800+ active listings and over $300 million in annual rental revenue — reveals what this deregulation counter-current actually means for investors and operators.

The March 2026 Preemption Wave: What Each State Actually Changed

Three bills, three strategies, one month. Here is what each state did — and what it means for the STR markets within their borders.

| Dimension | Indiana (HEA 1210) | Idaho (HB 583) | Pennsylvania (HB 2303) |

|---|---|---|---|

| Approach | Ban on rental caps | Broad preemption of local STR rules | Uniform statewide framework |

| Status | Signed March 12, effective July 1 | Signed March 16 | In committee (hearing March 25) |

| Cities can still do | Safety standards; HOA rules (homestead-only voting) | Public safety measures (smoke detectors, CO, fire extinguishers) | Comply within tiered framework |

| Cities cannot do | Cap rental property numbers | Owner-occupancy mandates, day caps, CUPs, structural mods, STR-specific fees | TBD |

| Political margin | 91-3 House, 48-0 Senate | 23-12 Senate | Democratic sponsors, early stage |

Why States Are Overriding Their Cities

What is new is the pace. Three states in a single month represents the most concentrated burst of pro-STR state legislation since Arizona's 2016 law.

The Idaho pathway illustrates how these laws build on each other. In May 2025, the Idaho Supreme Court unanimously overturned a Lava Hot Springs ordinance that banned non-owner-occupied STRs in residential zones. The town — with fewer than 400 permanent residents but 400,000+ annual tourists — had approximately 30% of its housing units listed as short-term rentals. The court ruled the ordinance violated Idaho's Short-term Rental and Vacation Rental Act. HB 583 extended that legal reasoning statewide.

"[HB 583] prevents local governments from imposing excessive or discriminatory requirements such as owner-occupied mandates, arbitrary caps on rental days, burdensome parking rules, or conditional use permits that go beyond what is required of other residential properties." — Heather Andrews, Americans for Prosperity, Idaho Senate testimony

The opposition perspective is equally direct. In Indiana, an IndyStar opinion column argued that "Indiana legislators have cleared the way for wealthy landlords to gobble up local housing" and that "state leaders say they want to protect the rights of property owners — that's not very helpful if the average person can't afford to own property at all." Carmel and Fishers had passed their 10% rental cap ordinances unanimously, reflecting genuine community concern about investor-owned properties displacing owner-occupied homes.

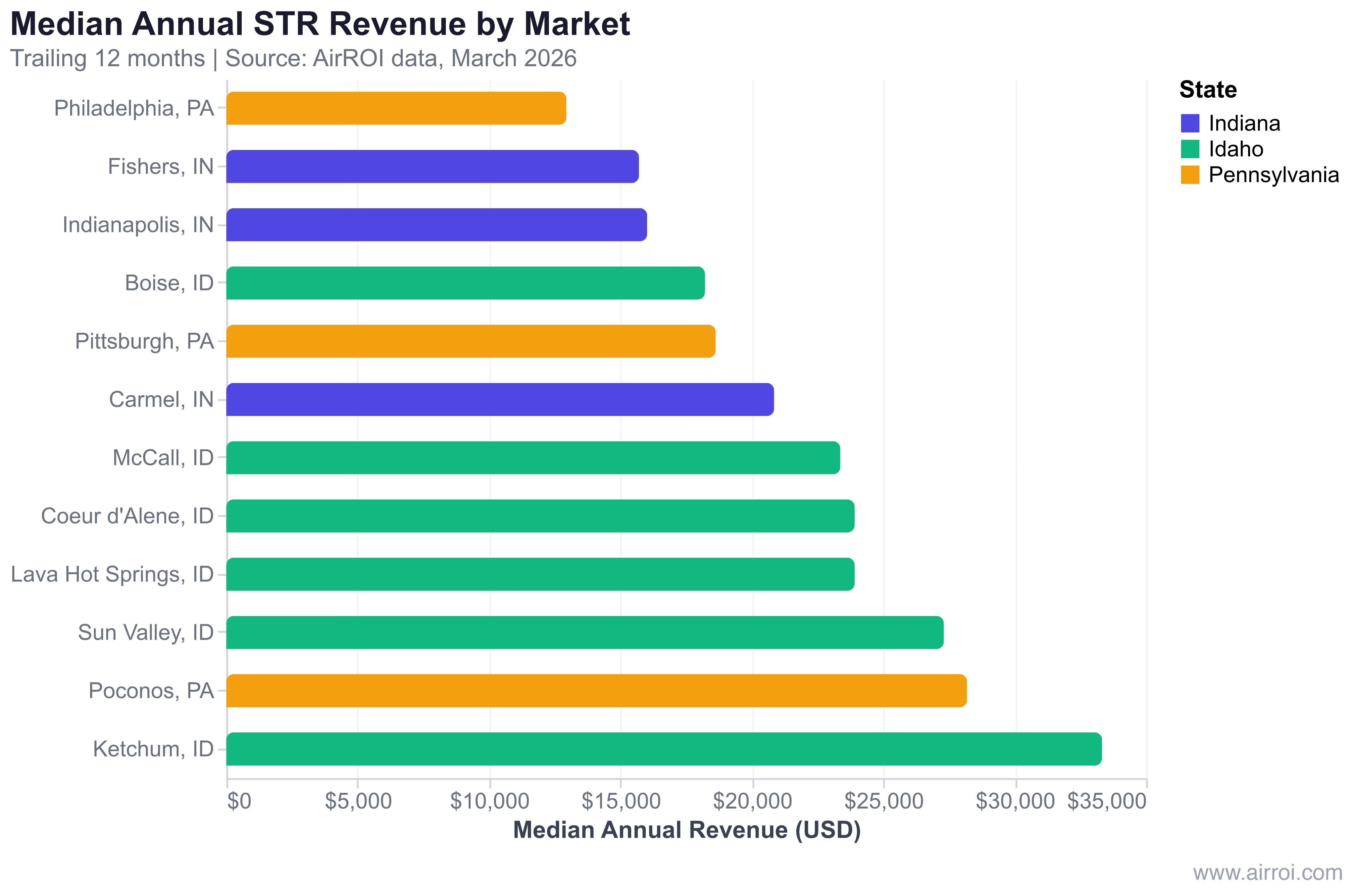

AirROI Data: How These 12 Markets Actually Perform

The legislative picture is only half the story. AirROI data across 12 markets in all three states reveals the operational reality behind the regulation.

| Market | Active Listings | Occupancy | ADR | Median Annual Revenue | RevPAR |

|---|---|---|---|---|---|

| Indianapolis, IN | 3,615 | 42% | $217 | $16,018 | $91 |

| Carmel, IN | 87 | 49% | $279 | $20,847 | $145 |

| Fishers, IN | 95 | 47% | $196 | $15,705 | $93 |

| Boise, ID | 1,596 | 54% | $185 | $18,214 | $100 |

| McCall, ID | 637 | 37% | $347 | $23,366 | $130 |

| Sun Valley, ID | 355 | 33% | $475 | $27,302 | $156 |

| Ketchum, ID | 476 | 37% | $531 | $33,326 | $193 |

| Coeur d'Alene, ID | 921 | 47% | $301 | $23,910 | $145 |

| Lava Hot Springs, ID | 153 | 35% | $283 | $23,910 | $109 |

| Philadelphia, PA | 5,766 | 44% | $181 | $12,943 | $82 |

| Pittsburgh, PA | 2,653 | 47% | $207 | $18,622 | $97 |

| Poconos, PA | 1,130 | 38% | $378 | $28,188 | $147 |

Three patterns emerge from the data. First, Idaho's resort corridor commands the highest nightly rates — Ketchum at $531 ADR, Sun Valley at $475, McCall at $347 — but runs the lowest occupancy (33-37%). These markets are built for peak-season pricing, not year-round consistency. Second, Indiana's suburban markets punch above their weight: Carmel generates $20,847 in median annual revenue from just 87 listings with 49% occupancy, outperforming Indianapolis proper by 30% on a per-listing basis. Third, Pennsylvania's largest market, Philadelphia, has the most listings (5,766) but the lowest median revenue ($12,943) — a sign of existing competitive saturation.

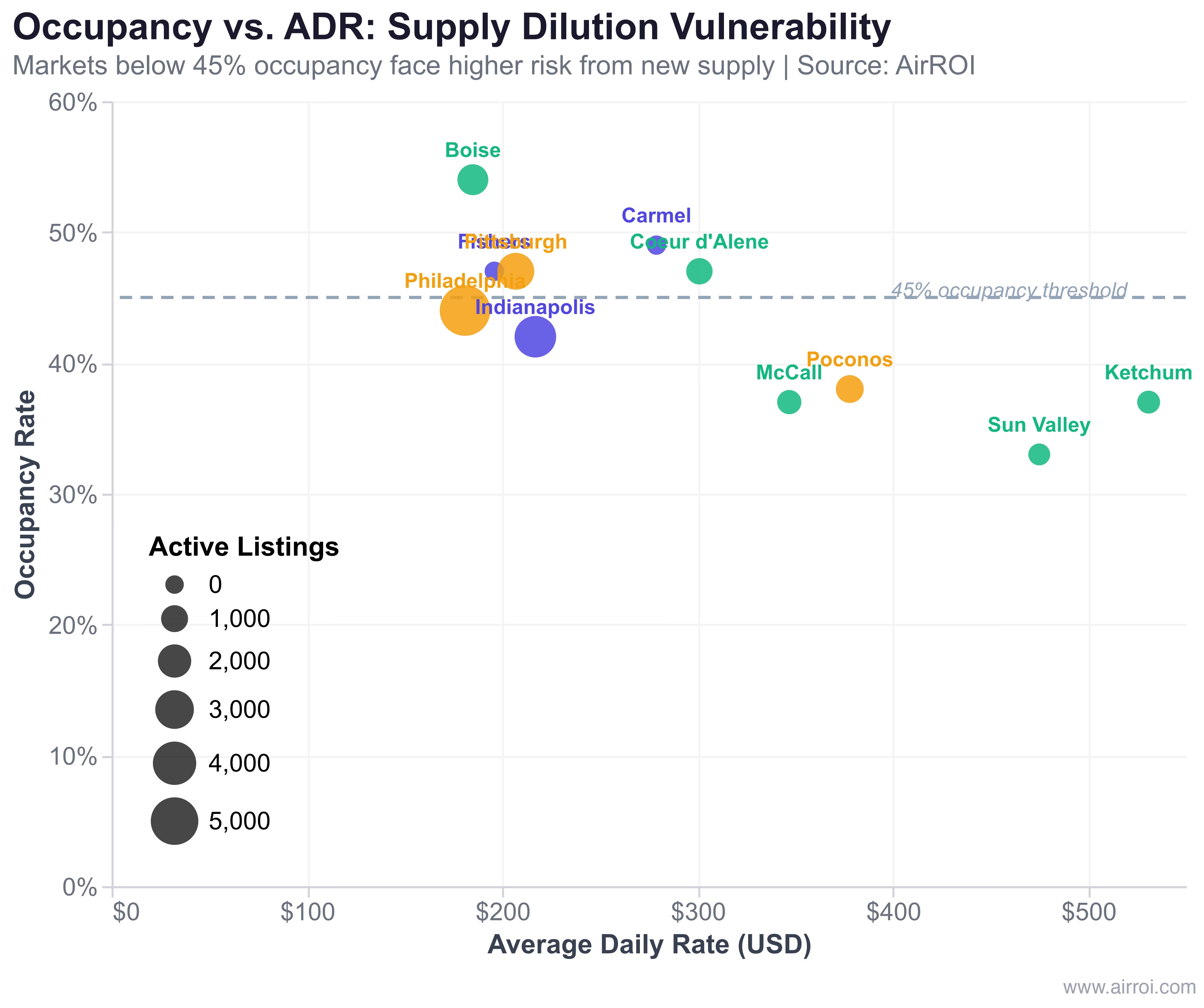

The Double Edge of Deregulation: Supply Dilution Risk

State preemption removes barriers to entry. That benefits new investors entering a market. But for existing operators, more supply without proportional demand growth means one thing: RevPAR compression.

The scatter plot above reveals a clear vulnerability gradient. Markets below the 45% occupancy threshold — Sun Valley (33%), Lava Hot Springs (35%), McCall (37%), Ketchum (37%), and the Poconos (38%) — already operate with more available nights than booked ones. Additional supply in these markets risks pushing occupancy lower, forcing operators to discount rates or accept extended vacancy periods.

Markets above 45% occupancy — Boise (54%), Carmel (49%), Fishers (47%), Pittsburgh (47%), and Coeur d'Alene (47%) — have demonstrated demand absorption capacity. New listings in these markets are more likely to find guests without cannibalizing existing operators' bookings.

The historical precedent supports this framework. When Arizona enacted its 2016 preemption law, Phoenix-area STR supply grew substantially in the following two years. Markets with strong urban demand absorbed the growth. But leisure-only destinations — already dependent on seasonal tourism — saw more competitive pressure.

For Idaho's resort markets specifically, the risk is real. Sun Valley and Ketchum operate at 33% and 37% occupancy respectively, with booking lead times of 73-78 days — indicating concentrated seasonal demand. If HB 583 encourages a wave of new listings from property owners who previously faced regulatory barriers, existing operators could see their annual revenue diluted even as nightly rates remain high.

Where Deregulation Creates Genuine Opportunity

Not all deregulated markets face supply dilution. AirROI data points to five signals that a newly opened market is worth entering:

- Occupancy above 45% — the market can absorb new supply without immediate RevPAR compression

- ADR-to-median-home-price ratio that justifies investment — higher ADR per dollar of property value signals better returns

- Booking lead time above 40 days — indicates planned travel demand, not distressed last-minute bookings

- Professional management penetration below 25% — room for the professionalization premium (AirROI data shows professionally managed listings earn 46-113% more revenue)

- Event-driven demand catalysts — Indianapolis 500, Pittsburgh's hosting of the 2026 NFL Draft, Boise's growth as a tech and outdoor recreation hub

Based on these criteria, three markets stand out:

Carmel, Indiana — With just 87 active listings, 49% occupancy, and a $279 ADR that exceeds Indianapolis by 29%, Carmel represents the tightest supply in the dataset relative to demand. HEA 1210's removal of the rental cap opens this market to new entrants, but the small base means even modest supply growth will take years to saturate.

Boise, Idaho — The highest occupancy in the dataset at 54%, combined with a diversified demand base (tech workers, outdoor recreation, university events), gives Boise the strongest demand absorption profile. At $185 ADR and $18,214 median revenue, it offers a lower entry point than Idaho's resort markets with more consistent cash flow.

Pittsburgh, Pennsylvania — At 47% occupancy and $18,622 median revenue, Pittsburgh benefits from event-driven demand (the 2026 NFL Draft is a near-term catalyst) and a comparatively affordable housing market. If HB 2303 creates standardized rules, it could actually benefit Pittsburgh operators by replacing uncertainty with a clear compliance framework.

The Counter-Current: Why Some Cities Keep Cracking Down

State preemption is not the universal direction. While Indiana, Idaho, and Pennsylvania moved to limit or standardize local STR regulation, cities in other states are intensifying restrictions.

The local-control argument has legitimate grounding. Lava Hot Springs — the Idaho town at the center of the Supreme Court case that preceded HB 583 — had nearly 30% of its housing listed as short-term rentals for a permanent population of fewer than 400 people. When tourism overwhelms housing supply at that ratio, community displacement is not hypothetical.

The question for investors is not whether preemption is "good" or "bad" — it is where the balance lies in each specific market. States tend to preempt when they view local restrictions as excessive barriers to property rights and economic growth. Cities tend to restrict when they view unchecked STR growth as a threat to housing affordability and neighborhood character. The operator who succeeds in 2026 is the one who monitors both levels and positions accordingly.

Disclaimer: This analysis is for informational purposes only and does not constitute investment or legal advice. Regulatory environments change rapidly. Consult local legal counsel before making STR investment decisions based on legislative changes.

Frequently Asked Questions

State preemption occurs when a state legislature passes a law that overrides local governments' ability to regulate short-term rentals. States like Arizona (2016), Florida (2011), and now Indiana and Idaho (2026) prevent cities from banning or capping STRs while allowing basic safety regulations. As of 2026, at least six states have enacted STR preemption laws.

No. HEA 1210 specifically prohibits cities and counties from capping the number of residential rental properties. Cities can still impose safety standards and other non-cap regulations. HOAs can still restrict rentals, but only homestead (owner-occupied) residents can vote on those restrictions under the new law.

HB 583 prevents local governments from imposing owner-occupancy mandates, caps on rental days, conditional use permits, parking rules beyond what other residential properties face, structural modification requirements, and STR-specific taxes or fees. Cities can still enforce general noise, nuisance, and traffic ordinances.

As of 2026, states with STR preemption laws include Arizona (2016), Florida (2011), Indiana (2026), Idaho (2017, expanded 2026), Tennessee, and Alabama (2024). Arizona and Ohio have additional preemption bills moving through their 2026 legislative sessions.

Focus on differentiation. As supply barriers drop, operators who invest in professional management, dynamic pricing, and superior guest experience maintain revenue. AirROI data shows professionally managed listings earn 46-113% more than individual hosts. Preemption rewards professional operators disproportionately.