Cash Flow

Key Takeaways

- Cash flow equals total rental income minus all expenses including mortgage payments — distinguishing it from NOI, which excludes debt service

- Positive cash flow is the primary objective for income-focused STR investors; negative cash flow requires subsidizing the property from other income

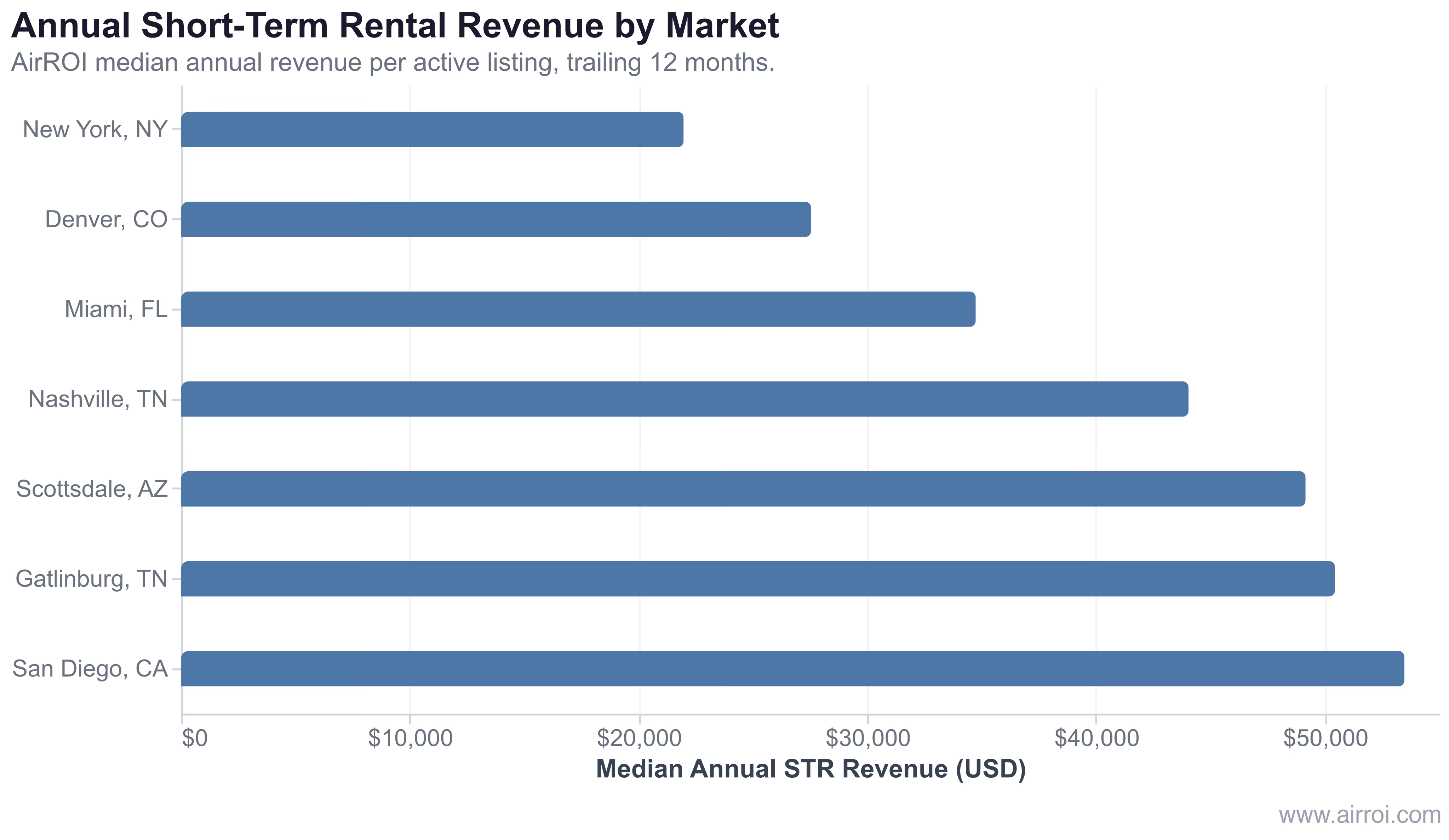

- Annual gross revenue — the ceiling on possible cash flow — ranges from roughly $22,000 in New York to $53,000 in San Diego based on AirROI trailing-12-month data

- Seasonal volatility makes monthly snapshots unreliable; use full-year cash flow for investment decisions

- Both the revenue and expense sides must be managed actively: pricing discipline drives income while expense control preserves the margin

How to Calculate Cash Flow

Monthly Cash Flow = Total Monthly Income − Total Monthly Expenses

Annual Cash Flow = Annual Gross Revenue − Annual Operating Expenses − Annual Debt Service

Or equivalently:

Cash Flow = NOI − Annual Debt Service

Example Calculation:

| Income (Monthly) | Amount |

|---|---|

| Nightly rental revenue | $5,800 |

| Cleaning fee income | $640 |

| Pet fees and extras | $120 |

| Total monthly income | $6,560 |

| Expenses (Monthly) | Amount |

|---|---|

| Mortgage (P&I) | $2,200 |

| Property management (20%) | $1,312 |

| Cleaning costs | $680 |

| Property taxes | $450 |

| Insurance | $200 |

| Utilities | $320 |

| Maintenance reserve | $330 |

| Platform fees | $197 |

| Supplies | $120 |

| Total monthly expenses | $5,809 |

| Monthly Cash Flow | $751 |

|---|---|

| Annual Cash Flow | $9,012 |

Annual Revenue: The Cash Flow Ceiling

Cash flow can only be as strong as the revenue base supporting it. AirROI's trailing-12-month data across 46,510 active listings in seven major US markets shows the range of median annual STR revenue — the gross income before expenses and debt service — that frames what cash flow is realistically achievable per market.

In AirROI's analysis of 46,510 active listings across San Diego, Gatlinburg, Scottsdale, Nashville, Miami, Denver, and New York, median annual revenue ranges from $21,970 (New York) to $53,472 (San Diego). Applying a typical 55% expense ratio (operating costs only, excluding mortgage) and a $26,400 annual mortgage payment on a median-priced property, a San Diego STR might produce $3,000+ per month in cash flow while a New York listing — under that city's 30-night minimum restriction — commonly runs at break-even or below.

Revenue sets the ceiling; expenses determine whether you clear it. Markets with the highest gross revenue don't always produce the best cash flow — purchase price and regulatory burden are the hidden variables that most investors underestimate.

Cash Flow Performance Benchmarks

| Monthly Cash Flow | Assessment | Context |

|---|---|---|

| Negative | Subsidizing the property | Acceptable only if strong appreciation expected |

| $0–$300 | Break-even to marginal | May not justify time and risk |

| $300–$800 | Moderate | Acceptable for appreciating markets |

| $800–$1,500 | Good | Solid income-producing asset |

| $1,500–$3,000 | Very good | Strong performer |

| $3,000+ | Excellent | Top-tier property or multi-unit |

Seasonal Cash Flow Considerations

STR cash flow varies significantly by season. Smart hosts plan for this:

| Season | Typical Revenue Impact | Cash Flow Strategy |

|---|---|---|

| Peak season | +30% to +60% above average | Build reserves for off-season |

| Shoulder season | −10% to +10% of average | Maintain pricing discipline |

| Off-season | −20% to −40% below average | Draw from reserves if needed |

Why Cash Flow Matters for STR Investors

- Financial sustainability: Positive cash flow means the property pays for itself and generates income, rather than requiring out-of-pocket subsidies

- Portfolio growth fuel: Monthly surpluses can be reinvested into additional properties — the compounding mechanism behind most successful STR portfolios

- Risk buffer: Strong cash flow creates reserves for unexpected repairs, vacancy spikes, and regulatory changes without forcing an emergency sale

- Leverage scorecard: Cash-on-cash return converts annual cash flow into a percentage of equity deployed, making it the correct metric for comparing leveraged investments; strong cash flow is its prerequisite

Tips for Maximizing Cash Flow

- Price dynamically: Revenue management discipline — adjusting nightly rates by demand, events, and lead time — is the single highest-leverage action an STR owner can take. AirROI data shows ADRs ranging from $221 (Denver) to $421 (Scottsdale); closing even half the gap between a market's median and top-quartile ADR adds thousands annually.

- Attack the largest expense first: Mortgage payments and management fees typically consume 50–60% of gross revenue. Refinancing, negotiating a lower management rate, or self-managing can add $300–$600 per month.

- Minimize vacancy: Reduce minimum-stay requirements during slow seasons, offer mid-week discounts, and maintain excellent reviews to keep occupancy above break-even. Every unbooked night is a permanent revenue loss.

- Build a maintenance reserve: Set aside 5–10% of revenue monthly. The alternative — deferring repairs — creates larger, costlier problems that crater cash flow when they can no longer be ignored.

- Evaluate with DSCR: Debt-service coverage ratio quantifies whether cash flow covers loan payments. Lenders typically require a DSCR above 1.25; falling below 1.0 means the property cannot service its own debt. Our STR investment analysis guide walks through how to model DSCR before acquisition.

- Compare Airbnb vs. long-term: In some markets, long-term rental income produces a superior risk-adjusted cash flow after accounting for STR expense load and vacancy. Use our Airbnb vs. long-term rental calculator to run both scenarios side by side before committing.

Frequently Asked Questions

Positive cash flow means your short-term rental generates more income than it costs to operate after all expenses, including mortgage payments. If your property collects $6,000 per month in revenue and total costs (operating expenses plus mortgage) are $4,500, you have $1,500 in positive monthly cash flow. Positive cash flow is the primary goal for income-focused STR investors.

A healthy Airbnb should generate $500 to $3,000+ in monthly cash flow after all expenses and mortgage payments, depending on the property size, market, and investment amount. As a rule of thumb, aim for at least $200–$300 per month per bedroom. Properties generating less than $300 total monthly cash flow may not adequately compensate for the time and risk involved in STR management.

Yes, this happens when a property's net operating income is positive but not large enough to cover mortgage payments. For example, a property with $30,000 NOI but $36,000 in annual mortgage payments has negative cash flow of $6,000 per year despite being operationally profitable. This typically occurs when the buyer made a small down payment, has a high interest rate, or overpaid for the property.