Hurricane Season 2026 Airbnb Impact: Why Below Average Isn't Safer

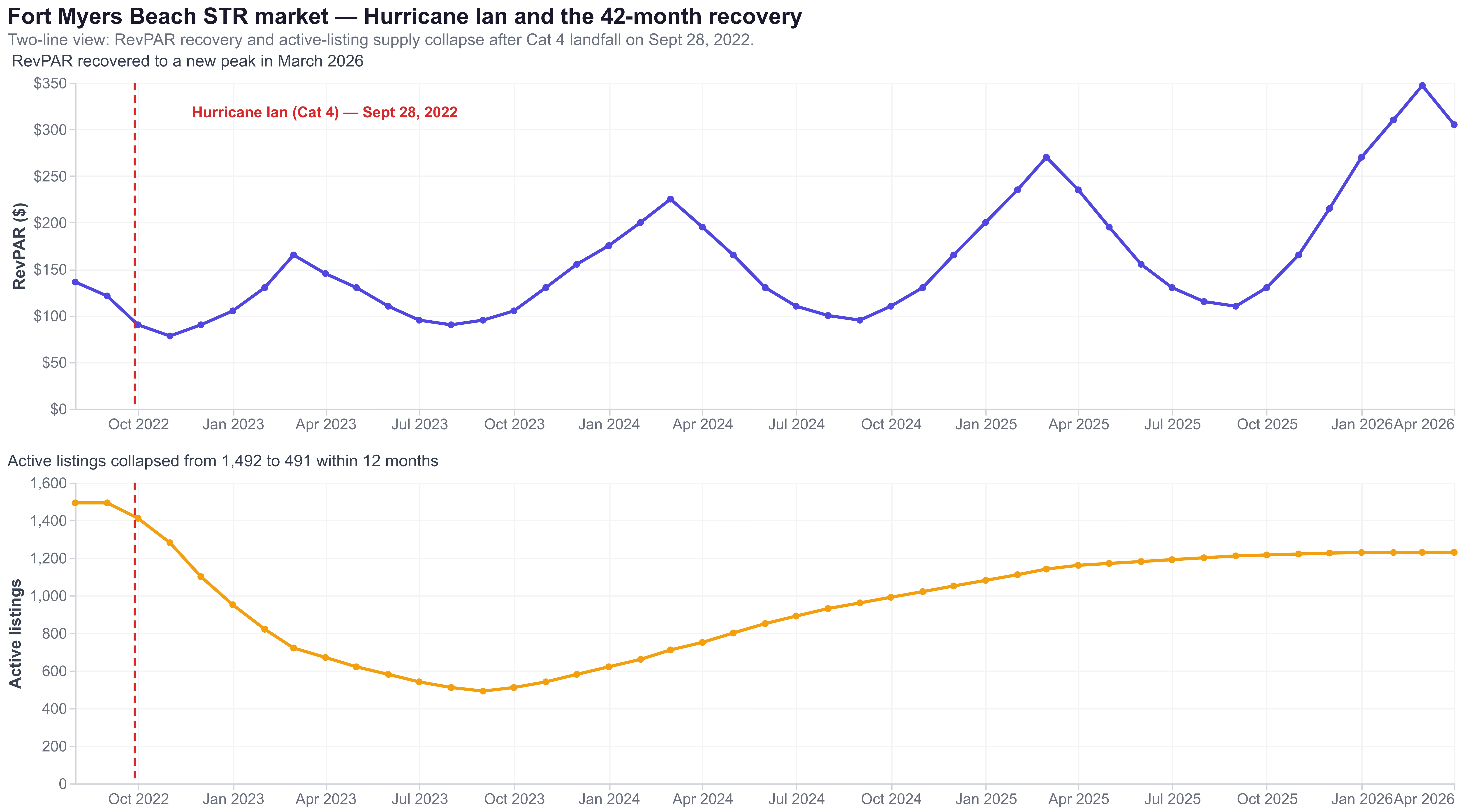

The hurricane season 2026 airbnb impact picture begins with one number from the last cycle: when Hurricane Ian made landfall on Fort Myers Beach as a Category 4 on September 28, 2022, AirROI data shows market occupancy dropped from 47% in September to 23% in November and active listings collapsed from 1,492 to 491 within twelve months. Fort Myers Beach RevPAR did not surpass its pre-Ian peak until March 2026 — 42 months later.

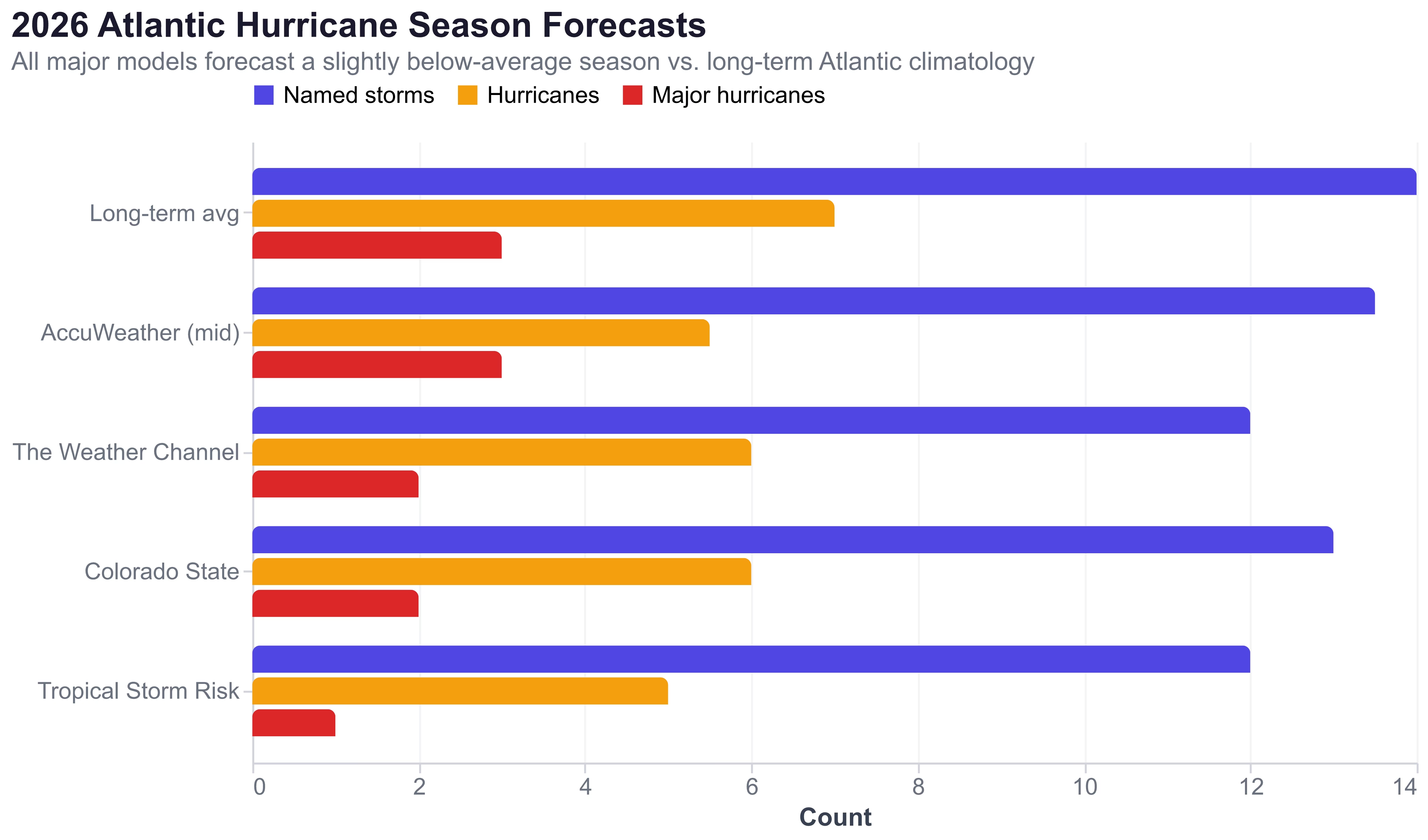

The 2026 Atlantic hurricane season opens June 1. AccuWeather forecasts 11 to 16 named storms with 3 to 5 expected US direct impacts. Colorado State University forecasts 13 named storms versus the long-term average of 14. The basin should be quieter than usual because a robust El Niño will increase vertical wind shear over the Atlantic. Almost everyone reading those numbers is reading them wrong.

A "below-average" basin forecast is a point estimate of total Atlantic activity. It is not a risk estimate for any single coastal property. The 3-5 expected US direct impacts have to make landfall somewhere — and when they concentrate in a 200-mile coastal stretch, the markets in that stretch absorb the full cliff while the basin average looks tame. Across nine coastal STR markets where AirROI has data on past direct hits, near-misses, and displacement events, the coastal vacation rental hurricane risk distribution is bimodal: a single storm either erases a quarter of revenue or, in some markets, drives it 40-70% above baseline.

This piece quantifies the per-storm cliff and recovery curve from past hurricanes, walks through what the 2026 forecast means by market, and lays out the four pre-season decisions that separate hosts who absorb a direct hit from hosts who don't.

What the 2026 hurricane forecast actually says

Three major forecast models converge on a slightly below-average 2026 Atlantic hurricane season. AccuWeather, Colorado State University (CSU), and Tropical Storm Risk (TSR) all expect the basin to produce fewer named storms than the long-term climatological average of 14, primarily because of an expected El Niño pattern that increases vertical wind shear and suppresses Atlantic storm formation.

| Forecaster | Named Storms | Hurricanes | Major Hurricanes | ACE Index |

|---|---|---|---|---|

| Long-term Atlantic average | 14 | 7 | 3 | ~120 |

| AccuWeather (March 2026) | 11-16 | 4-7 | 2-4 | n/a |

| Colorado State (April 2026) | 13 | 6 | 2 | 90 |

| Tropical Storm Risk (April 2026) | 12 | 5 | 1 | 66 |

| The Weather Channel | 12 | 6 | 2 | n/a |

| NOAA expected US direct impacts | 3-5 | n/a | n/a | n/a |

Phil Klotzbach, the senior research scientist who leads CSU's hurricane forecasting team, attributes the suppression to "high likelihood of robust El Niño and associated increases in vertical wind shear." That is the textbook mechanism: when Pacific waters warm and the Walker Circulation shifts, upper-level winds across the Atlantic strengthen, and tropical disturbances that would have organized into named storms get sheared apart before they consolidate.

The mistake almost every coastal STR investor is making this month is reading "robust El Niño" as a risk-reduction signal for their specific property. It is not. It reduces the expected basin total. It does not reduce the variance of where a storm makes landfall.

Why "below average" is a point estimate, not a risk estimate

The math behind that caveat is the part STR investors need to internalize. If NOAA's central estimate is 3-5 direct US hurricane impacts in 2026, that is the basin total. It is not the per-market probability of being hit. If four hurricanes make landfall and three of them concentrate in the Florida Panhandle and Big Bend, then a Destin or Tampa property carries roughly the same direct-hit probability it would have in an above-average season. Conversely, an Outer Banks property that gets through October without a Carolina-track storm captures the upside of a quiet season at full season pricing.

"Our analog seasons ranged from well below-average Atlantic hurricane activity to somewhat above average. There are curveballs that could come our way." — Phil Klotzbach, Colorado State University, on the 2026 forecast

This is what bimodal distribution means in practice. A coastal STR's annual revenue from a hurricane season is not a single number with mild seasonal noise. It is two numbers: the full-season uplift if no storm hits the property's stretch of coast, or a 40-90% revenue cliff for the affected month and a multi-month or multi-year recovery if one does. The expected value sits between them, but no host actually realizes the expected value — every host realizes one tail or the other.

The forecast tells you the basin probability. It does not tell you where the variance lands on your specific 30 miles of coast. Florida emergency management captured the same idea more pithily during Hurricane Preparedness Week (May 3-9, 2026): "Quiet forecast, loud warning."

What past hurricanes actually did to coastal STR revenue

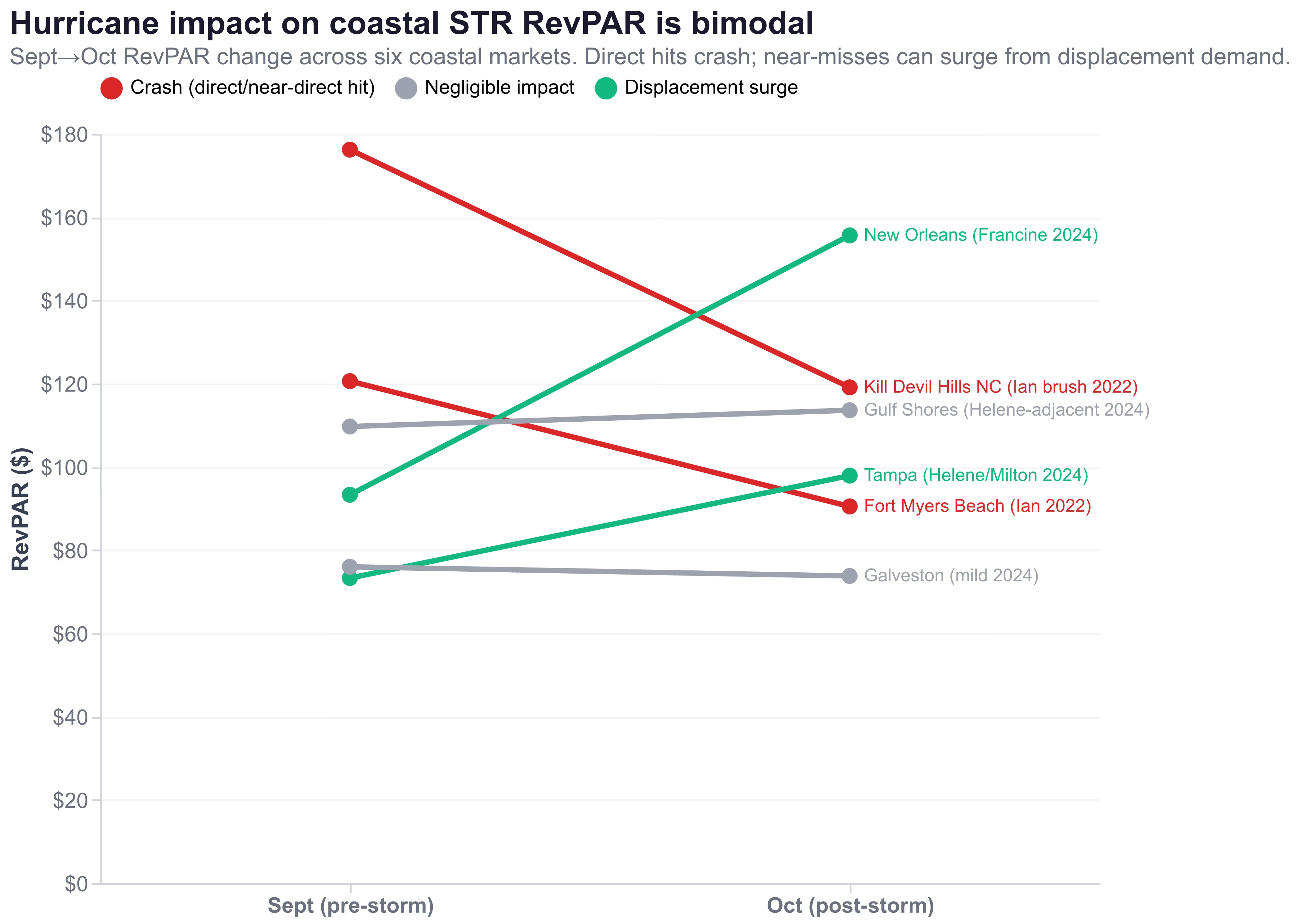

Forecasts are predictions. AirROI's market data is the actual receipt. Looking at September-to-October RevPAR shifts across six coastal markets in their respective storm-impact years, the bimodal pattern is unmistakable.

| Market | Storm | Sep RevPAR | Oct RevPAR | Single-Month Change |

|---|---|---|---|---|

| Fort Myers Beach (FL) | Ian, Sept 28, 2022 (Cat 4) | $120.6 | $90.5 | -25% |

| Kill Devil Hills NC (Outer Banks) | Ian brush + cancellations 2022 | $176.2 | $119.1 | -32% |

| Tampa (FL) | Helene + Milton, Sept-Oct 2024 | $73.3 | $97.9 | +34% (displacement) |

| New Orleans (LA) | Francine, Sept 11, 2024 | $93.3 | $155.6 | +67% (displacement) |

| Galveston (TX) | Mild 2024 season | $76.0 | $73.8 | -3% |

| Gulf Shores (AL) | Helene-adjacent 2024 | $109.7 | $113.6 | +4% |

Same calendar month. Six different markets. Six different outcomes. The two markets in the storm's direct path (Fort Myers Beach in 2022, Kill Devil Hills via cancellation cascade) lost a quarter to a third of their RevPAR in a single month. The two markets adjacent to the storm but spared direct damage (Tampa, New Orleans) gained 34% to 67% as evacuees, insurance adjusters, and contractors absorbed inventory at premium pricing. The two markets fully outside the impact zone (Galveston, Gulf Shores) saw only normal seasonal noise.

This is what the contrarian framing gives you that the forecast does not. The 2026 season will produce some markets that look like Fort Myers Beach 2022, some that look like Tampa 2024, and most that look like Destin in any year — undisturbed. The forecast tells you how many storms. It does not tell you which markets.

Coastal STR market profiles — five hurricane scenarios from the AirROI dataset

Fort Myers Beach — the direct-hit cliff

Hurricane Ian was the costliest hurricane in Florida history, with total damage estimated at $112 billion per the National Hurricane Center. The eye crossed Fort Myers Beach as a high-end Category 4 with sustained winds of 150 mph and a storm surge of approximately 16 feet. The market's STR economics did not just disrupt — they rebuilt from a smaller base.

AirROI's monthly metrics for Fort Myers Beach show the cliff in granular detail. Average market occupancy was 0.48 in August 2022, 0.47 in September, then 0.35 in October, 0.23 in November, and 0.22 in December — the bottom of the cliff hit roughly 75 days after landfall. RevPAR dropped from $136 in August 2022 to $77.6 in November 2022. But the more telling number is supply: the active listing count fell from 1,492 in September 2022 to 491 in October 2023, a 67% loss of operating inventory within twelve months as homes were destroyed, displaced families chose not to relist, and structural rebuilds pulled hundreds of properties offline for a year or more.

The recovery curve is real but partial. By March 2026 — 42 months after Ian — Fort Myers Beach RevPAR finally surpassed pre-storm peaks at $347 (versus $121 in September 2022). Active listings have rebuilt to 1,229, still 18% below the pre-Ian universe. Survivors who reopened at higher ADRs against constrained supply are doing well. The two-thirds of operators who never reopened are simply gone.

Tampa — the displacement surge after Helene and Milton

Tampa absorbed Hurricane Helene (landfall September 26, 2024) and Hurricane Milton (October 9, 2024) within two weeks. AirROI data shows the evacuation-driven drop and the displacement bounce in adjacent months: market occupancy fell from 0.50 in August to 0.44 in September, then surged to 0.59 in October as displaced residents, adjusters, and relief workers absorbed inventory at premium rates.

Outer Banks (Kill Devil Hills) — the brush perception cliff

The Outer Banks did not absorb a direct hit from Hurricane Ian — the eye was in southwest Florida, more than 700 miles away. Yet AirROI data shows Kill Devil Hills RevPAR fell from $176 in September 2022 to $119 in October 2022 — a 32% drop in a single month with no direct landfall. The same pattern repeats whenever a Carolina-track threat develops: Hurricane Florence in 2018 cost the Outer Banks a chunk of October revenue without significant local damage, and Hurricane Lee's 2023 brush did the same on a smaller scale.

This is the brush risk, and it is structurally different from the direct-hit risk. Travelers cancel because the news shows "Carolinas" inside the storm cone, not because the rental is uninhabitable. The mitigation is operational, not structural — an explicit hurricane addendum offering credit-for-future-stay (rather than refund) protects revenue and review scores, and proactive guest communication during named-storm windows turns confused travelers into rebooked travelers. The Outer Banks market consistently recovers within 60-90 days from a brush event, but only for hosts who actively work the recovery.

Destin (FL Panhandle) — what undisturbed looks like

Destin is the control case. The market saw no major direct hurricane impact between 2022 and 2025. AirROI data shows what an undisturbed Panhandle season delivers: June 2024 RevPAR of $290.8 grew to $372.4 in June 2025 (+28% year-over-year), with peak ADR hitting $493 in July 2025. Destin had the same pre-season hurricane-risk profile as Fort Myers Beach in 2022 — same coastline, same forecast, similar statistical exposure. Different outcome, different P&L. Destin pulled the upside tail; Fort Myers Beach pulled the catastrophic tail. Neither was knowable in May.

New Orleans — the displacement-only case

Hurricane Francine made landfall as a Category 1 well west of New Orleans on September 11, 2024. The city avoided significant damage. AirROI data shows the cleanest displacement-surge case in the dataset: September 2024 occupancy was 0.41 with $93 RevPAR; October jumped to 0.54 occupancy and $155.6 RevPAR — a 67% RevPAR increase in a single month as adjusters, contractors, and relief workers absorbed inventory at premium pricing. Even when a market avoids direct damage, regional storms can drive revenue UP if hosts are configured to convert quickly. Hosts who didn't capture the surge were the ones whose minimum-stay rules and rate floors blocked the inquiries.

Florida's insurance squeeze isn't getting better in 2026

The arithmetic most STR investors don't run before buying coastal Florida looks like this. A standard Florida named-storm deductible runs 2% to 5% of dwelling value, applied separately each time the National Hurricane Center names a storm that affects the property. On a $500,000 dwelling, a 5% named-storm deductible is $25,000 out-of-pocket per named storm — per event, not per season.

STR-specific coverage is harder. The dominant view across high-engagement r/airbnb_hosts threads is consistent: AirCover is not insurance, hurricane-prone Florida hosts pay $5,000 to $13,000+ annually for specialty STR coverage, and umbrella riders that cover STR business use are increasingly hard to find without specialty placement.

"Insurance in Florida right now absolutely sucks and short-term rental insurance in Florida is an absolute disaster... I went through about 12 companies before I was able to find one that would insure my STR. Most insurance companies are looking for reasons to not insure you." — u/lancert, top-voted comment in r/airbnb_hosts Florida STR insurance thread

A second host on the same subreddit captures the rider-vs-policy distinction that catches operators after the first claim: "I had a rider from Allstate but when I looked closer it was garbage. If a guest burned down my house they claimed a limit of $20k. Thus, I switched to Proper insurance — it is quite a bit more expensive but it is specifically designed for STR." Specialty carriers most often cited in the host community include Proper Insurance, NREIG, Steadily, and Safely.

Three things to verify on your declarations page before June 1: the named-storm deductible amount and trigger language, the business-use endorsement (a homeowner's policy without it can be voided when the carrier discovers STR activity), and the wind-versus-water exclusion structure. This is general information, not personalized insurance advice — work with a licensed broker who specializes in coastal STR coverage.

Airbnb's Major Disruptive Events Policy — what's covered, what isn't

The exception that matters: a foreseeable weather event becomes a covered event when it triggers another covered event — specifically a mandatory evacuation order or a large-scale outage of essential utilities. When a county issues a mandatory evacuation for the property's address, affected reservations during the evacuation period qualify for refunds.

For hosts, this has three implications. Listings in coastal markets need explicit hurricane-addendum language so guests know that Florida hurricane season is foreseeable, refunds outside of mandatory evacuation are at host discretion, and trip insurance is the right hedge. When a mandatory evacuation order drops, hosts should pre-approve refunds for evacuation-zone bookings rather than waiting for escalations — review preservation matters more than the marginal night revenue when the property cannot be safely occupied. And hosts should monitor National Hurricane Center advisories during the season the way they monitor pacing during the rest of the year, because the legal trigger that shifts financial liability is binary and can be issued 36-72 hours before landfall.

The four pieces of paper that decide your hurricane quarter

The hosts who outperform their coastal market in a hurricane year are not the ones with the best storm shutters. They are the ones who have already converted four pieces of paperwork — the insurance declarations page, the listing's hurricane addendum, the PMS pricing tier, and the property manager service agreement — that decide whether a named storm becomes a $25,000 deductible event or a 67% RevPAR surge. None of the four can be meaningfully edited once a tropical wave is 36 hours offshore.

Insurance is the highest-leverage of the four because the asymmetry is so violent. A 5% named-storm deductible on a $500,000 dwelling means a single landfalling storm costs $25,000 out of pocket before the policy pays anything. A 2% deductible on the same dwelling costs $10,000, a $15,000 swing per event driven by one line on the declarations page. Specialty STR carriers (Proper, NREIG, Steadily, Safely are the four most often cited in r/airbnb_hosts) typically negotiate the lower deductible at a higher annual premium, and breakeven is usually a single named-storm event over the policy life. A brokered switch runs $300-$800 in commission and pays back the first time a tropical system crosses your 30-mile coastline.

The hurricane addendum is the cheapest piece of the stack and the most overlooked. Airbnb's Major Disruptive Events Policy already excludes foreseeable Florida hurricanes, but only for the host whose listing copy explicitly establishes hurricane season as foreseeable and offers credit-for-future-stay as the alternative to a refund. Hosts without the addendum either eat the refund (revenue loss) or contest it (review-score loss). Hosts who add it before season spend almost no time on cancellation negotiation once a storm is in the cone, because the policy is already on the listing page the guest read at booking. One hour of editing.

The property manager service agreement is the only document with no mid-season substitute. If the contract does not specify a hurricane response protocol (board-up trigger, photo-documentation cadence, communication SLA, vendor pre-arrangement), the time to negotiate one is not the week the storm forms. Most PM agreements include some version of the language. Most owners have not actually read theirs.

The forecast says 11 to 16 named storms and 3 to 5 expected US direct impacts. That is a useful aggregate and a poor risk model. A below-average season still concentrates somewhere, and the four documents above are what separate the hosts who absorb a direct hit from the hosts who don't. They matter more in a quiet year than the forecast does, because the hosts who skip them are betting their stretch of coast won't be one of the three or five.

Frequently Asked Questions

The 2026 Atlantic hurricane season runs June 1 through November 30. AccuWeather forecasts 11-16 named storms with 3-5 expected US direct impacts; Colorado State forecasts 13 named storms, 6 hurricanes, and 2 major hurricanes; Tropical Storm Risk forecasts 12 named storms. All major models call for a slightly below-average year because of an expected robust El Niño that suppresses Atlantic activity through increased vertical wind shear.

Airbnb's Major Disruptive Events Policy explicitly excludes hurricanes during Florida's June-November season as "foreseeable" weather. Refunds are only triggered when the storm causes a mandatory evacuation order or a large-scale outage of essential utilities. Hosts should add an explicit hurricane addendum to their listing copy for the season, and pre-approve refunds when evacuation orders are issued for the property's address.

Florida property insurance policies typically carry a named-storm deductible of 2% to 5% of the dwelling value, triggered whenever the National Hurricane Center names a storm. On a $500,000 dwelling, a 5% named-storm deductible is $25,000 out-of-pocket per event — a number most short-term rental owners discover only after their first claim. The deductible applies separately to each named storm, not per season.

Recovery time scales with damage severity. Tampa's RevPAR returned to baseline three months after Hurricanes Helene and Milton in 2024 thanks to displacement demand offsetting the evacuation drop. Fort Myers Beach RevPAR did not surpass its pre-Ian peak until March 2026 — 42 months after the 2022 landfall — and active-listing count remains roughly 18% below pre-storm levels per AirROI data. A near-miss like the Outer Banks during Hurricane Florence typically recovers in 60-90 days from the perception cliff alone.

Review your insurance policy declarations page for the named-storm deductible, business-use endorsement, and wind/water exclusions. Update your listing's hurricane addendum, pre-write guest communication templates for the four NHC alert stages, pre-position storm shutters and supplies, and load a 30-day medium-term pricing tier into your property management system in case a storm forces a pivot to displacement bookings. Use AirROI Atlas to benchmark your current pacing against your market.