LA28 Olympics Airbnb Lodging Shortfall: Why Airbnb's 320,000-Visitor Math Runs Into LA's 120-Day Cap

A Deloitte report released in February 2026 and commissioned by Airbnb projects a peak-day shortfall of up to 320,000 visitors across 13 of the 19 competition days at the LA28 Olympic and Paralympic Games. The report's headline solution: double Los Angeles and Orange County short-term rental capacity and close 88% of the gap, unlocking $488 million in local economic activity. Every LA news outlet ran the number. Almost none of them ran the number against LA's own rulebook.

We did. Using live AirROI data for 11 LA-region submarkets and the plain text of LA's Home-Sharing Ordinance, this article asks a question Airbnb's PR cycle studiously avoids: can LA actually double STR supply by July 2028, or is the 120-day cap a hard ceiling no amount of demand can break?

The short answer — and the one embedded in the math below — is that the Deloitte projection is an industry-funded wish, not an operating plan. LA city has 14,201 active Airbnb listings. On the default Home-Sharing Ordinance, every one of them is legally rentable only 120 nights per year. That is 32.9% of a full calendar year. The Olympic window sits deep in summer peak, which is exactly when a capped host is most likely to have already burned through their nights. Doubling that base requires loosening the cap, dramatically expanding Extended Home-Sharing permits, or getting lucky with informal hosting that will be very hard to square with the January 2026 LAPD background-check rule.

What is possible is a very different story — one written mostly in Orange County, Long Beach, and a handful of LA County cities where the regulation supports full-year operation. Here is the data, submarket by submarket.

The Deloitte/Airbnb Headline in Plain English

- Visitor inflow. LA28 will attract roughly 3.4 million incremental visitor-days across the Olympic and Paralympic windows (July 14 – July 30, 2028 for the Olympic Games and August 15 – August 27, 2028 for the Paralympics).

- Peak-day shortfall. On 13 of the 19 Olympic competition days, projected visitor volume exceeds available lodging supply by up to 320,000 visitors per peak day.

- STR uplift opportunity. If Los Angeles and Orange County short-term rental capacity were to double over 2024 levels, 88% of the peak-day shortfall could be absorbed by STRs rather than pushed to displaced trips.

- Economic activity. That absorbed demand, counting direct spending on lodging, food, transportation, and spectator services, represents roughly $488 million in additional Los Angeles County economic activity.

The report is careful to note that it models capacity potential, not capacity certainty, and it flags LA's current regulatory environment as a constraint on its own forecast. Where the PR cycle leaves that nuance behind is when the "doubling" claim gets restated as if it were an operational plan. It isn't. Doubling 14,201 LA-city listings to ~28,400 is not a supply-side problem Airbnb can solve with marketing. It is a municipal-ordinance problem the Los Angeles City Council would have to solve, and it has no current appetite to do so.

Let's look at what is actually on the ground right now.

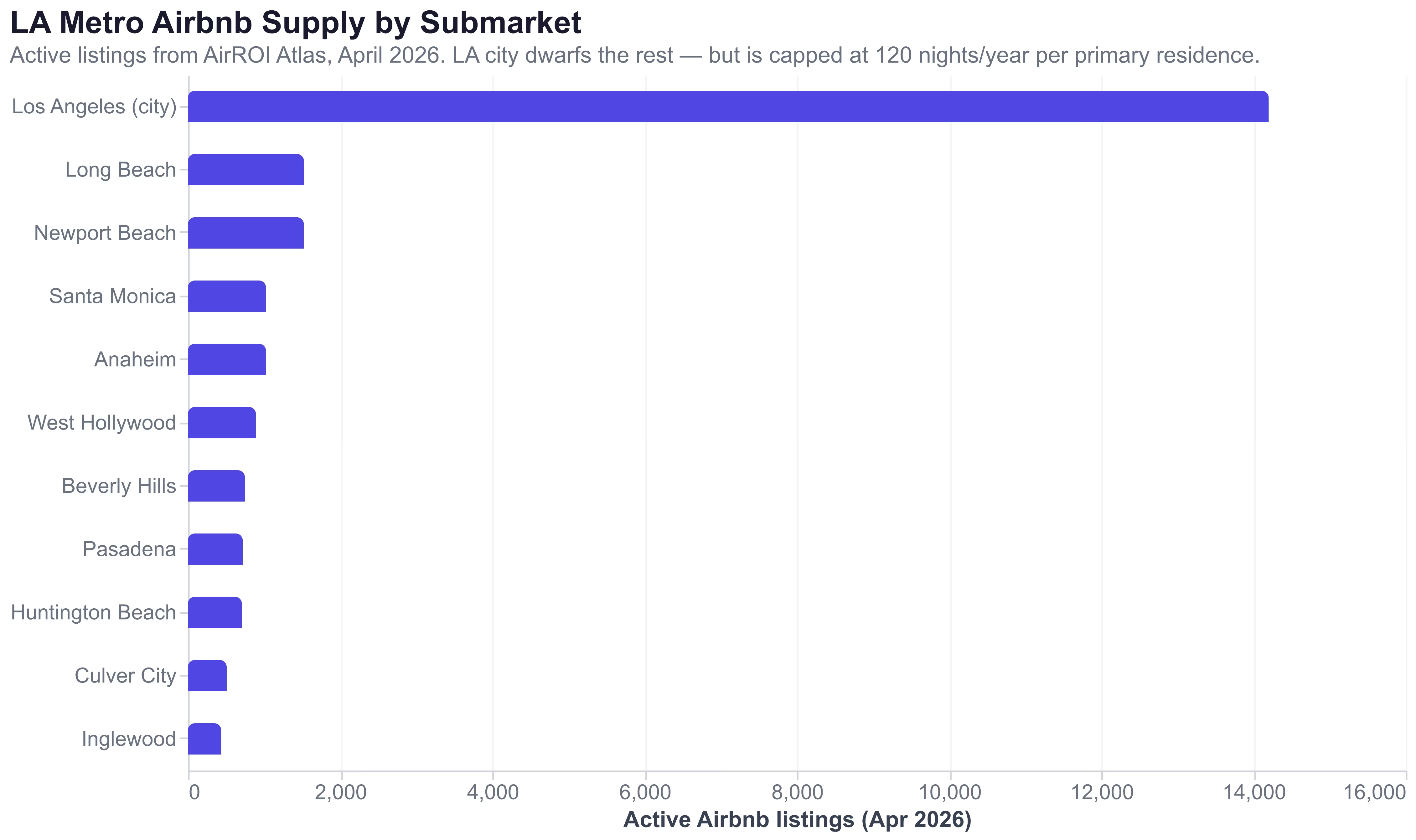

LA Metro STR Supply, Submarket by Submarket

AirROI's Atlas inventory across the LA region as of April 2026 lines up like this:

| Submarket | Active listings | ADR (2BR/2BA) | Occupancy | RevPAR | Olympic context |

|---|---|---|---|---|---|

| Los Angeles (city) | 14,201 | $215 | 49.0% | $105 | Cryto.com Arena (gymnastics), LA Convention Center (weightlifting), citywide host regime |

| Long Beach | 1,525 | $254 | 52.7% | $134 | Sailing, handball, water polo cluster |

| Newport Beach | 1,524 | $364 | 53.1% | $193 | OC beach spillover lodging |

| Santa Monica | 1,026 | $273 | 59.3% | $162 | Beach volleyball spillover, coastal transit hub |

| Anaheim | 1,026 | $249 | 59.9% | $149 | Anaheim Convention Center (handball) |

| West Hollywood | 894 | $223 | 54.7% | $122 | Hospitality/entertainment spillover |

| Beverly Hills | 749 | $265 | 55.3% | $147 | Premium visitor housing, hotel-heavy |

| Pasadena | 721 | $237 | 55.3% | $131 | Rose Bowl (soccer finals) |

| Huntington Beach | 710 | $349 | 55.8% | $195 | OC beach spillover |

| Culver City | 510 | $234 | 55.7% | $130 | Westside transit spillover |

| Inglewood | 438 | $200 | 53.8% | $107 | SoFi Stadium (opening ceremony + swimming) |

Source: AirROI Atlas, April 2026. ADR, occupancy, and RevPAR calculated from trailing-twelve-month comps for a 2BR/2BA/4-guest baseline.

Two numbers jump out immediately.

The first is the headline asymmetry: LA city alone is ~61% of the regional STR supply in this 11-market sample. Doubling the regional base means, in practice, doubling or nearly doubling LA city. Every smaller market would have to roughly double as well, but LA city is doing the heavy lifting simply because it is six to thirty times the size of its neighbors.

The second, which the table does not show directly, is that Inglewood — the host of LA28's opening ceremony and swimming events at SoFi Stadium and the Intuit Dome — has only 438 active Airbnb listings. SoFi seats 70,000+. The Intuit Dome seats 18,000+. The ratio of seats-within-one-mile to Airbnb-listings is the worst in the LA region, and it sits inside a 120-day-cap jurisdiction. This is the specific geography where the Deloitte supply-side argument matters most, and it is the specific geography where LA's Home-Sharing Ordinance bites hardest.

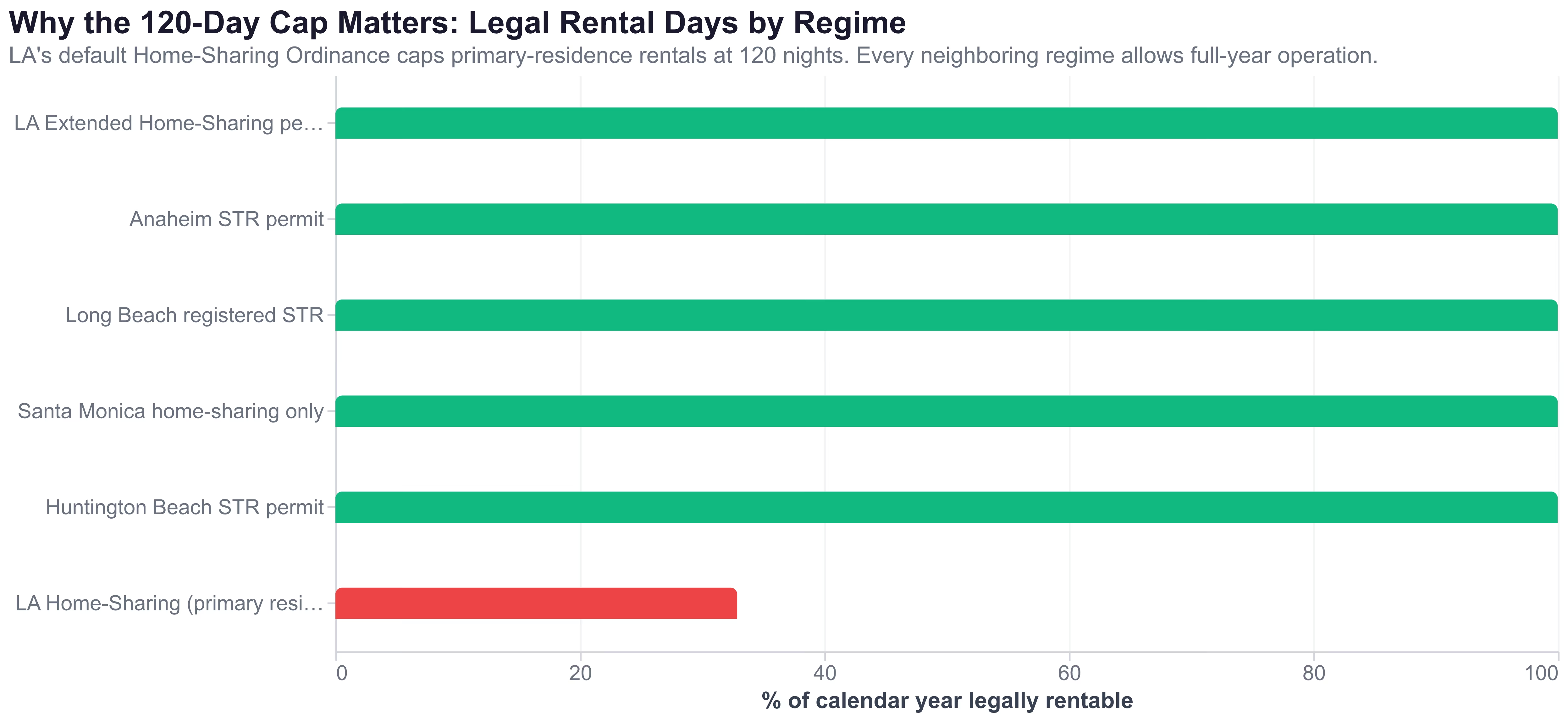

The 120-Day Cap Math: Why LA Listings Don't Count Like Other Cities' Listings

LA's Home-Sharing Ordinance (HSO), codified under Los Angeles Municipal Code §12.22.A.32, does two things that most out-of-town analysts routinely miss:

- It restricts short-term rentals to a primary residence only — the host must be physically present for the majority of the year and cannot operate a non-owner-occupied STR.

- It caps rentals at 120 nights per calendar year unless the host obtains an Extended Home-Sharing (EHS) permit, which, in the city's own Planning Department language, requires the property to "meet all additional application, inspection, and eligibility criteria" and, as of January 2026, to clear an LAPD background check tied to the Department's new STR registration workflow.

The 120-night figure sounds generous. It isn't. Here is the comparison against the regimes in LA's neighboring submarkets:

Every city that borders LA — including Anaheim, Long Beach, Huntington Beach, and Santa Monica under its registered home-sharing regime — allows a properly permitted listing to operate 365 days per year. LA, in its default configuration, allows 120. That is the ordinance, not our editorial. A full-year-equivalent listing in Anaheim is worth three full-year-equivalent LA primary-residence listings purely on a legal-capacity basis.

Now overlay the Olympic calendar. The 2028 Olympic Games run July 14 through July 30 — 17 days sitting squarely inside the single most valuable three-week STR window of the year in LA. Deloitte's "13 of 19 peak competition days" framing spans Olympic plus Paralympic peak-demand days; either way, a capped host operating normally will have already allocated 40-60 of their 120 nights to spring and early-summer demand. A host specifically saving their cap for the Games forgoes the April-June booking revenue and bets the 120 remaining nights can be covered by Olympic premiums — a bet that pencils out only for a small sliver of hosts in SoFi-adjacent ZIP codes.

The honest accounting is this: a 120-day-capped LA listing can, in the best case, deliver every peak-demand night of the LA28 window, and in the realistic case delivers 8-12 nights. That realistic number — not the full peak window — is what belongs in any supply-side projection. Deloitte's "doubling" number assumes unrestricted capacity. LA's ordinance is the opposite of unrestricted.

The Extended Home-Sharing path is the release valve the city designed, and in principle it allows a qualifying host to rent beyond 120 nights. In practice, EHS permit holders are a small minority of the listed base: the LA Planning Department's most recent public count puts registered EHS permits in the low thousands against a citywide active-listings count of 14,201. That means even if every EHS permit holder maximized availability for LA28, the marginal room-nights they add are a fraction of what the PR number implies.

The 2026 LAPD Permit Update: Supply Is Tightening, Not Loosening

The January 2026 rule change was understated at the time. The LA Planning Department added an LAPD background-check clearance step to the EHS permit workflow, citing an uptick in party-house and nuisance complaints during 2024-2025. On paper, it closed a loophole. In practice, it introduced a multi-week processing delay to an already-slow pipeline, added a fee-equivalent administrative burden, and moved new EHS approvals from "routine" to "case-by-case."

We don't have a clean month-over-month delta on LA-city listing counts at time of writing, but the directional evidence is clear: AirROI's 14,201 LA-city active-listings count is meaningfully below the city's estimated 2019 peak of 20,000+ listings. The regulatory environment has been net-contractionary for five consecutive years. The 27-month runway to July 2028 is not long enough to reverse a half-decade trend — particularly when the newest regulatory change slows rather than accelerates new permits.

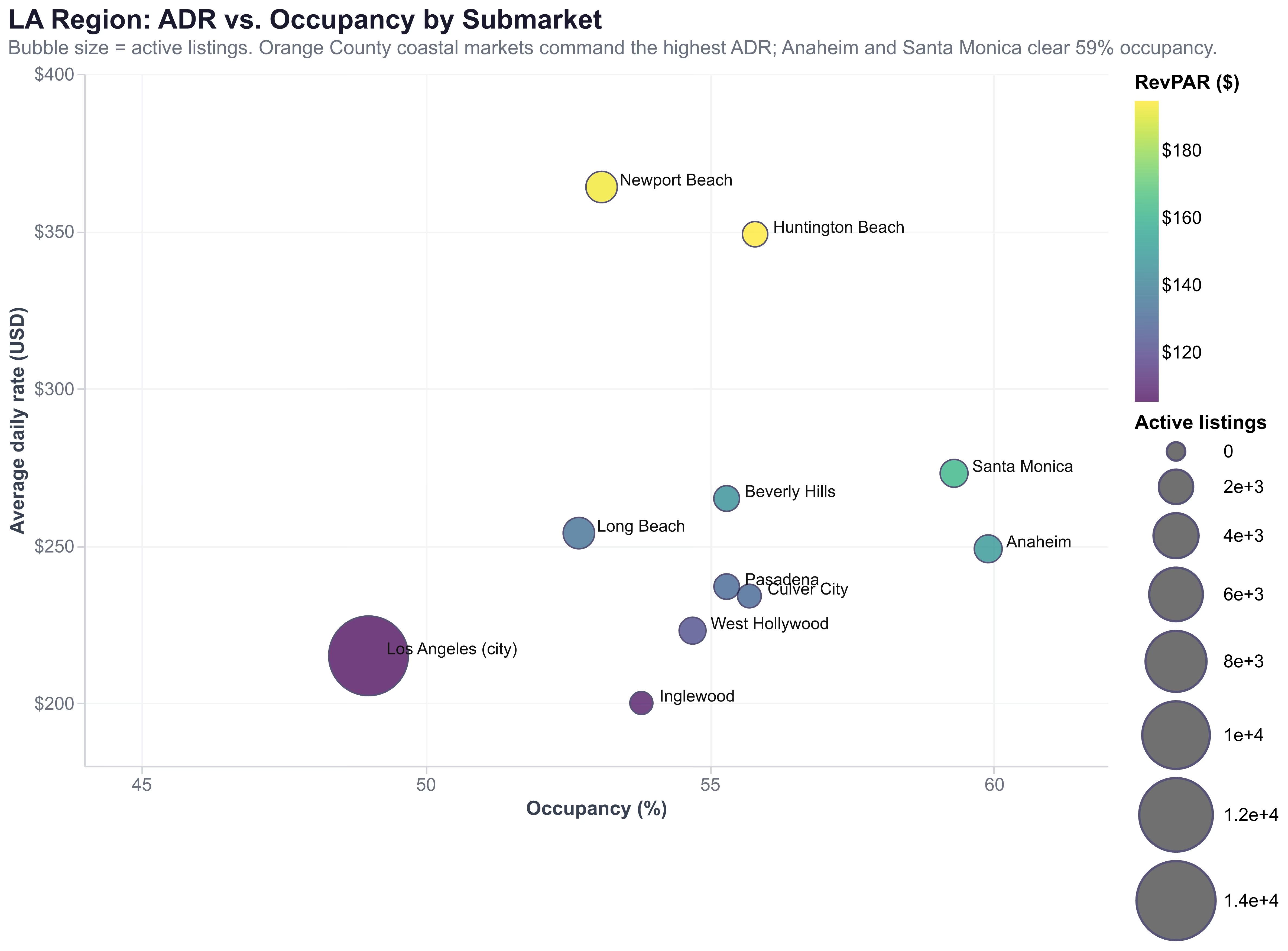

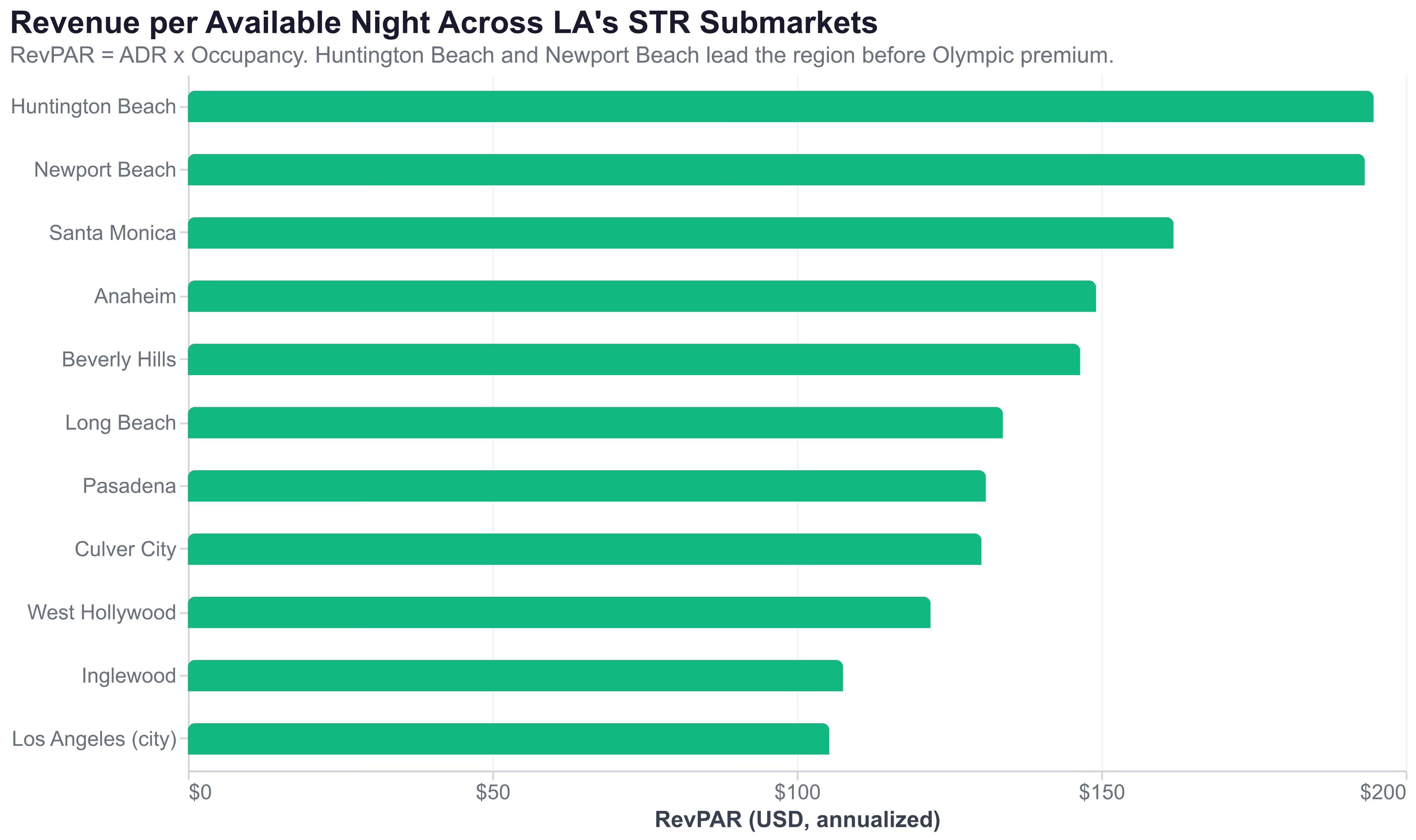

The RevPAR Landscape: Where the Money Actually Lives

If the supply question is structural, the revenue question is geographical. The scatter below plots average daily rate against occupancy for our 11 submarkets, with bubble size representing active-listings inventory and color representing RevPAR.

Three things stand out:

-

Orange County coastal premium is real. Huntington Beach ($349 ADR, 55.8% occupancy, $195 RevPAR) and Newport Beach ($364 ADR, 53.1% occupancy, $193 RevPAR) lead the region on a per-available-night basis — and they sit in a regulatory regime that allows full-year operation. These are the submarkets where a new investor can legally acquire, permit, and scale between now and LA28.

-

Santa Monica and Anaheim are the occupancy leaders. Both clear 59% on our baseline comp. Santa Monica's listings operate under the city's home-sharing regime (primary-residence only), but the absolute 1,026-listing base is already being bid up by beach volleyball, coastal transit, and spectator overflow planning. Anaheim's 59.9% occupancy, combined with a 1,026-listing base and a handball-venue designation at the Convention Center, is the sleeper LA28 submarket.

-

Inglewood is underpriced for its venue proximity. SoFi Stadium hosts the opening ceremony and swimming; the Intuit Dome sits adjacent. And yet Inglewood carries the region's lowest ADR ($200) and lowest RevPAR ($107) among the 11 submarkets we sampled. That is partly because the neighborhood is still in a long-running STR normalization arc and partly because primary-residence supply simply cannot match the Stadium's seating demand. Whether you read it as "upside" or "structural floor" depends on your view of LA's willingness to adjust the HSO before the Games.

The same story in a cleaner cut:

Orange County as the Pressure Valve

Here is where the Deloitte analysis gets closest to being operationally right, and it is worth steelmanning it. The OC cluster — Anaheim, Long Beach, Huntington Beach, Newport Beach — has the following characteristics:

- No 120-day cap. Each city operates a registered STR permit system that allows full-year operation for hosts meeting zoning, parking, and TOT-remittance requirements.

- Permit pipelines are finite but moving. Anaheim's STR moratorium history (2016 passage, 2019 clarifications) created a grandfathered permit pool plus ongoing case-by-case additions. Long Beach's permit count has grown modestly every year since 2021. Huntington Beach and Newport Beach operate capped permit pools with multi-year pipelines.

- Total OC-cluster listing count is 4,785 — about one-third of LA city's 14,201, but with full-year legal capacity each listing represents a materially greater share of effective Olympic-window supply than a capped LA primary residence.

- Venue adjacency is real. Long Beach hosts sailing, handball, and water polo venues. Anaheim Convention Center hosts handball. Huntington Beach and Newport Beach absorb the coastal visitor flow that Santa Monica and Venice can no longer fully house.

If the region doubles OC cluster capacity — which would mean expanding permit pools by roughly 4,785 listings — that adds on the order of 90,000 room-nights across the 19-day window before even accounting for higher occupancy. That is a meaningful share of the Deloitte target, and it is the realistic upside for LA28 supply planning.

The catch: OC cities have their own political economics. Anaheim residents have historically opposed STR expansion; Huntington Beach passed a strict permit ordinance in 2019; Newport Beach caps its permit count. None of these cities is going to wake up in 2027 and unilaterally double permits for an event. What will happen — and what is already happening — is that existing permit holders will price aggressively for LA28, new permits will trickle in at a normal rate, and the effective supply-side expansion will be on the order of 10-20% rather than the 100% Deloitte's report embeds.

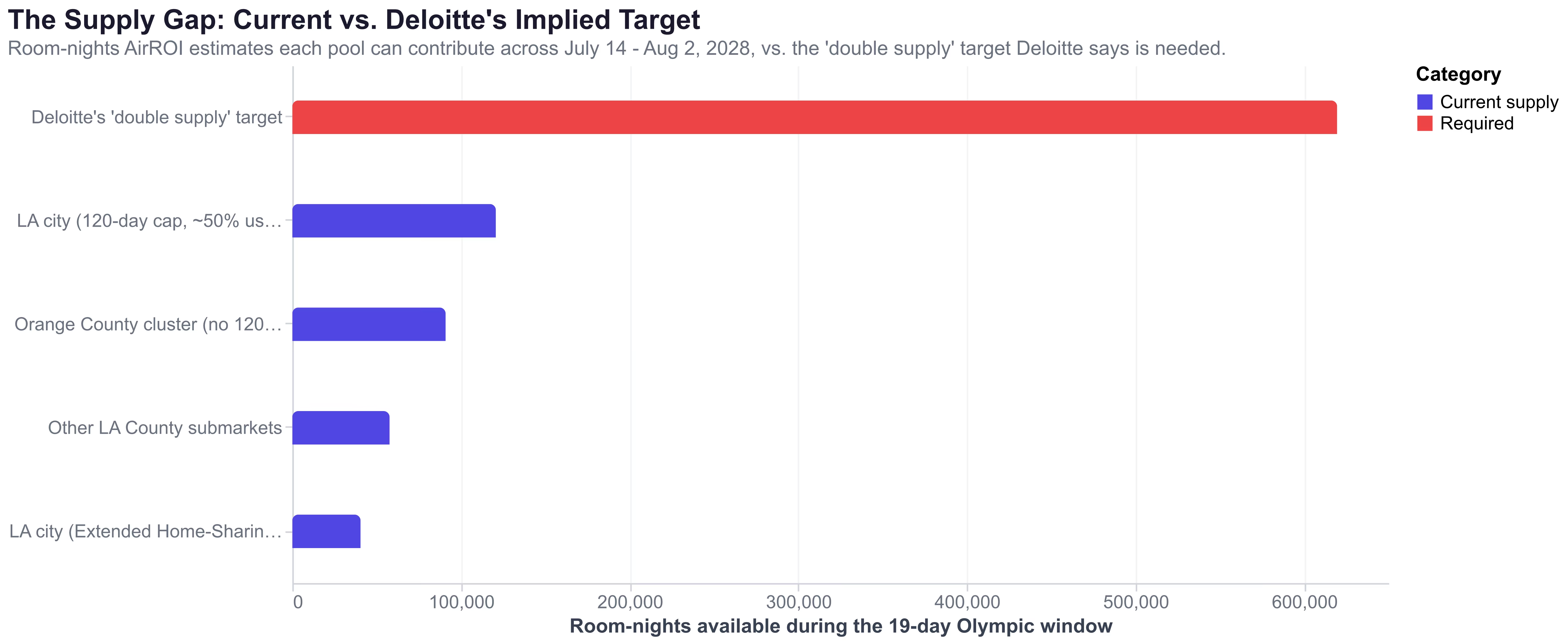

Scenario Model: Can LA Actually Double Supply?

Putting the pieces together, here is our quantified scenario model of room-nights available across Deloitte's 19-day peak-demand window (the peak competition-day subset spanning both the Olympic and Paralympic Games) for the LA region:

The assumptions:

- LA city, capped primary residences (~85% of 14,201 = 12,071 listings). Assume each capped listing contributes an average of ~10 nights during the peak window — a realistic blended number given most hosts will have spent some of their 120-day budget on earlier 2028 demand but can still prioritize the Olympic premium. Effective room-nights: 12,071 × 10 ≈ 120,710.

- LA city, Extended Home-Sharing permit holders (~15% of 14,201 = 2,130 listings). Full 19-night window. Effective room-nights: ~40,470.

- Other LA County submarkets (Santa Monica, WeHo, Beverly Hills, Pasadena, Culver City, Inglewood = 4,338 listings). Blended 70% utilization across city rules. Effective room-nights: ~57,700.

- Orange County cluster (Anaheim, HB, NB, Long Beach = 4,785 listings). No 120-day cap, full 19-night window. Effective room-nights: ~90,915.

Sum of current effective supply: ~309,795 room-nights across the 19-day window.

Deloitte's "double supply" target requires reaching roughly 2× that pool, or 619,590 room-nights. That is the red bar in the chart above. Reaching it means adding approximately 310,000 net new room-nights across the LA-OC region between April 2026 and July 2028.

Under current ordinances, that gap closes only if one or more of the following happens:

- LA City Council votes to raise the 120-day cap to 180 or 240 nights (no current agenda).

- LA reduces Extended Home-Sharing permit friction and triples the EHS pool (the January 2026 rule moved in the opposite direction).

- OC cities unilaterally expand permit pools by 50%+ (no current political momentum).

- Hotels expand LA-county room inventory by 10,000+ keys (multi-year process; some growth, but not at this scale).

Our honest read on the probability-weighted outcome is 10-20% incremental supply by July 2028, which maps to roughly 30,000-60,000 incremental room-nights — not the 310,000 the Deloitte doubling implies. That covers 10-20% of the visitor gap, not 88%.

What This Means for Hosts on the 27-Month Runway

We've laid out the pessimistic case on the macro. But LA28 remains a once-in-a-generation pricing event for individual hosts. Here is how the data reshapes the playbook:

1. Register now — in every jurisdiction. Whether you own a primary residence in LA city or a non-owner-occupied unit in Long Beach, the permit pipelines will lengthen in 2027. Applications submitted in 2026 will clear ahead of the Olympic scrum. Waiting costs you the event entirely.

3. Consider the OC acquisition case. A non-primary-residence investment in Anaheim, Long Beach, Huntington Beach, or Newport Beach — acquired in 2026, permitted in 2026-2027, and review-built through 2027 — is the cleanest regulatory path to LA28 revenue. OC permit systems allow full-year operation, and the current RevPAR baseline ($134-$195 depending on city) is a healthy floor to build an Olympic premium on top of.

4. Do not buy specifically for LA28 in LA city. Non-owner-occupied STR operation is explicitly prohibited under the HSO. The Extended Home-Sharing permit path requires primary-residence status, which means you have to live there. A "buy for the Olympics" purchase in LA city proper is a regulatory dead end, no matter how strong the demand forecast looks.

5. Price off submarket comps, not citywide averages. RevPAR in Huntington Beach ($195) is 82% higher than RevPAR in Inglewood ($107). Olympic premiums will compound that gap. Hosts who price off a citywide LA average will systematically under-price the OC coastal cluster and over-price inland submarkets.

6. Watch the hotel supply closely. If LA hotels expand toward the Deloitte target on their own, the marginal Olympic visitor Airbnb needs to capture will be the lowest-paying segment. The highest-paying tranche — corporate hospitality, media rights holders, NOC delegations — will book hotels first. Hosts who calibrate expectations around the leisure-traveler tranche will set more realistic (and ultimately more profitable) rates.

Our Realistic Prediction

Will LA actually double STR supply by July 2028?

No. Not under current ordinances, and not even under plausible loosening scenarios. The 120-day cap plus the January 2026 LAPD permit rule act as a structural ceiling on LA-city supply expansion. Orange County absorbs some of the overflow, but OC's own permit pools are finite and politically contested. Hotels add rooms at a normal pace. The remainder of the Deloitte-modeled shortfall — probably 60-70% of it — resolves not through added supply but through displaced trips (visitors who attend a single day and commute in from San Diego, Palm Springs, or San Bernardino), compressed room occupancy (two families per unit instead of one), and un-booked demand (visitors who wanted to come but couldn't find lodging and cancelled).

The Deloitte number is not wrong about the demand. It is wrong about the supply side's capacity to respond. And that distinction — demand forecast minus regulatory ceiling — is the number every LA28 host, investor, and policymaker should be underlining in red.

What AirROI Tracks Next

We'll be updating the LA-region supply data monthly through LA28. The three signals we're watching:

- Monthly change in LA-city EHS permit count — a leading indicator of whether the January 2026 rule is loosening or tightening the supply pipeline.

- OC cluster permit growth — the realistic upside for marginal Olympic-window capacity.

- Booking-window behavior for July 2028 dates — when corporate and media bookings begin compressing the calendar, submarket ADR premiums will materialize in the data.

The LA28 lodging story is not the one Airbnb's Deloitte report tells. It is tighter, weirder, and more geographically specific — and the hosts who understand it first will be the ones earning the Olympic premium the rest of the market was priced out of.