DSCR Loans for Airbnb: Which Markets Actually Qualify in 2026 (18-Market Scorecard)

Every search result for "DSCR loan airbnb" is a lender trying to sell you a loan. Griffin Funding, Rabbu, Newfi, HomeAbroad, Beeline — they all explain what a DSCR loan is and how to apply. None of them answer the question investors actually need answered: will my target market's short-term rental revenue support a 1.25x DSCR ratio?

We did the math. Using AirROI's trailing-twelve-month revenue data for 18 US markets combined with current median home prices from Zillow and Redfin, we calculated the actual debt service coverage ratio for each market at a 7.25% DSCR loan rate with 25% down and 30-year amortization. The result: 12 of 18 popular STR markets clear the 1.25x threshold that most lenders require — but expensive coastal and luxury markets like San Francisco, Denver, and Scottsdale still fail badly.

This is the independent, data-driven DSCR loan short term rental analysis that does not exist anywhere else online.

What Is a DSCR Loan and Why Should Airbnb Investors Care?

A DSCR (Debt Service Coverage Ratio) loan qualifies borrowers based on the property's rental income rather than personal income. The formula is straightforward: annual gross rental income divided by annual debt service (PITIA — principal, interest, taxes, insurance, and association fees). As Defy Mortgage puts it: "You don't need to show your tax returns, W-2s, or personal income to qualify — the property qualifies itself."

The magic number for most lenders is 1.25x. That means the property must generate 25% more annual income than the total annual mortgage payment. A ratio of 1.0 is breakeven — the property covers the debt but produces zero cash flow. Anything below 1.0 means the investor pays out of pocket every month.

For Airbnb investors specifically, DSCR loans solve a critical scaling problem. Conventional mortgages cap borrowers at 10 financed properties (the Fannie/Freddie limit) and require extensive income documentation. DSCR loans have no property count limit — each property qualifies independently on its own rental income.

| Feature | DSCR Loan | Conventional Mortgage |

|---|---|---|

| Income qualification | Property rental income | Borrower W-2 / tax returns |

| Typical rate (2026) | 6.0%–7.99% | 6.5%–7.0% |

| Down payment | 20%–25% (up to 35% sub-1.0) | 15%–25% |

| Max properties | Unlimited | 10 (Fannie/Freddie cap) |

| STR income accepted | Yes (projected or actual) | Requires 2-year rental history |

| Credit minimum | 640–680 FICO | 620–660 FICO |

Key takeaway: DSCR loans are purpose-built for STR investors scaling beyond 2–3 properties. The trade-off is a 0.5–1.5% rate premium — worthwhile when DTI limits block conventional financing, but only if your target market's revenue clears the 1.25x threshold.

The Calculation Nobody Does: Market-Level DSCR Math

Lenders tell you to "research your market" before applying for a DSCR loan for Airbnb — but none of them actually do that research for you. Here is the exact calculation:

DSCR = Annual STR Revenue ÷ Annual Mortgage Payment (P&I)

Our methodology:

- Revenue: AirROI trailing-twelve-month (TTM) median revenue per market

- Home price: Median home price from Zillow and Redfin (April 2026)

- Down payment: 25% (standard for STR DSCR loans)

- Interest rate: 7.25% (mid-range for STR DSCR loans in 2026)

- Term: 30-year fixed amortization

- Monthly P&I per $1,000 at 7.25%: $6.82

A Market That Passes: Logan OH (Hocking Hills)

A 3-bedroom cabin near Hocking Hills State Park carries a median home price of $280,000. At 25% down, the loan is $210,000. Monthly P&I at 7.25% is $1,432, or $17,186 annually. AirROI data shows Logan OH cabins earn a median $60,374 per year in STR revenue.

DSCR = $60,374 ÷ $17,186 = 3.51x — the strongest pass in our analysis. This property generates more than three and a half dollars for every dollar of debt service.

A Market That Fails: San Francisco CA

San Francisco's median home price is $1,300,000. At 25% down, the loan is $975,000. Annual P&I: $79,814. But AirROI data shows San Francisco's median STR revenue is only $36,218 — constrained by a 90-day annual cap on non-primary-residence short-term rentals.

DSCR = $36,218 ÷ $79,814 = 0.45x — a clear fail. The property generates only 45 cents for every dollar of debt service. No DSCR lender approves this at standard terms.

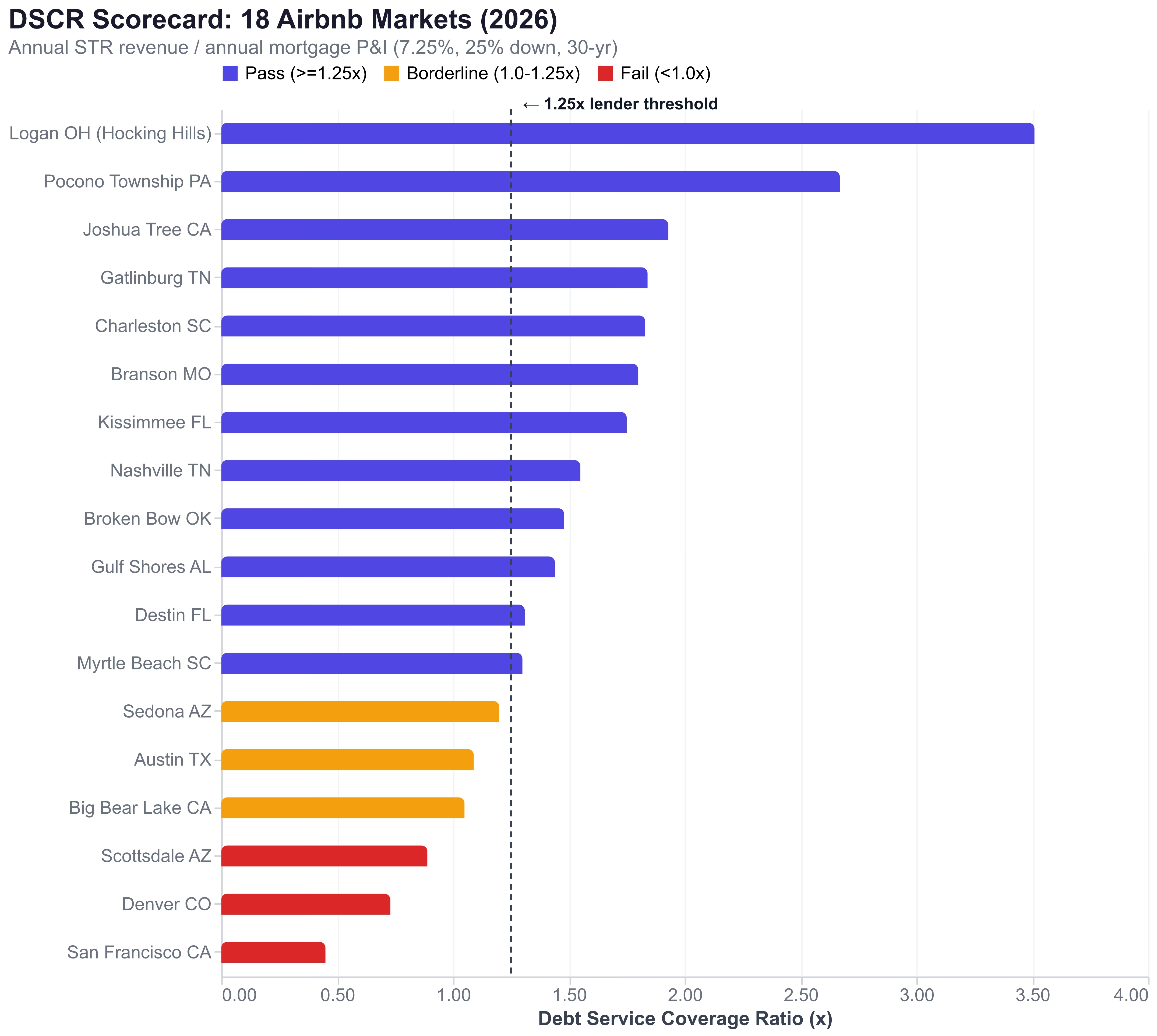

The 18-Market DSCR Scorecard

Here is the complete scorecard for 18 US short-term rental markets, ranked by DSCR ratio. We selected markets across the full spectrum — vacation destinations, urban markets, mountain towns, and beach communities — to show where DSCR financing works and where it does not.

| Market | Median Home Price | Loan (75%) | Annual P&I | TTM Revenue | DSCR | Verdict |

|---|---|---|---|---|---|---|

| Logan OH (Hocking Hills) | $280,000 | $210,000 | $17,186 | $60,374 | 3.51x | Strong Pass |

| Pocono Township PA | $370,000 | $277,500 | $22,710 | $60,724 | 2.67x | Strong Pass |

| Joshua Tree CA | $450,000 | $337,500 | $27,621 | $53,199 | 1.93x | Strong Pass |

| Gatlinburg TN | $507,000 | $380,250 | $31,124 | $57,291 | 1.84x | Strong Pass |

| Charleston SC | $599,000 | $449,250 | $36,769 | $67,176 | 1.83x | Strong Pass |

| Branson MO | $261,000 | $195,750 | $16,020 | $28,796 | 1.80x | Strong Pass |

| Kissimmee FL | $369,000 | $276,750 | $22,649 | $39,725 | 1.75x | Strong Pass |

| Nashville TN | $480,000 | $360,000 | $29,462 | $45,657 | 1.55x | Pass |

| Broken Bow OK | $650,000 | $487,500 | $39,897 | $58,869 | 1.48x | Pass |

| Gulf Shores AL | $477,000 | $357,750 | $29,278 | $42,154 | 1.44x | Pass |

| Destin FL | $645,000 | $483,750 | $39,590 | $51,861 | 1.31x | Pass |

| Myrtle Beach SC | $303,000 | $227,250 | $18,601 | $24,198 | 1.30x | Pass |

| Sedona AZ | $977,000 | $732,750 | $59,969 | $72,087 | 1.20x | Borderline |

| Austin TX | $455,000 | $341,250 | $27,928 | $30,300 | 1.09x | Borderline |

| Big Bear Lake CA | $596,000 | $447,000 | $36,584 | $38,456 | 1.05x | Borderline |

| Scottsdale AZ | $880,000 | $660,000 | $54,014 | $47,851 | 0.89x | Fail |

| Denver CO | $590,000 | $442,500 | $36,217 | $26,497 | 0.73x | Fail |

| San Francisco CA | $1,300,000 | $975,000 | $79,814 | $36,218 | 0.45x | Fail |

Sources: AirROI TTM revenue data (April 2026), Zillow/Redfin median home prices (March-April 2026). P&I calculated at 7.25% / 30-year / 25% down. DSCR uses P&I only — adding taxes and insurance would lower ratios further.

The pattern is clear: markets that pass DSCR easily aren't necessarily the highest-revenue markets — they have dramatically lower entry costs. A $280,000 cabin in Hocking Hills earning $60,374 clears 3.51x DSCR, while a $977,000 Sedona property earning $72,087 manages only 1.20x. The ratio is about affordable entry more than raw revenue.

Markets Where the Math Works: DSCR Above 1.25x

Twelve of 18 markets in our analysis clear the 1.25x DSCR threshold at standard terms. They share a common trait: moderate to manageable home prices paired with strong STR demand drivers.

Logan OH (Hocking Hills) — 3.51x DSCR

Hocking Hills is Ohio's premier outdoor recreation destination, anchored by Hocking Hills State Park. With a median home price of just $280,000 and median annual revenue of $60,374, this market produces the strongest DSCR ratio in our analysis. AirROI data shows 45% occupancy and a $411 ADR — driven by couples and families booking 2–3 night cabin getaways from Columbus, Cincinnati, and Cleveland. The 702 active listings keep supply manageable relative to demand.

Pocono Township PA — 2.67x DSCR

The Poconos serve as the weekend escape valve for 30 million residents of the NYC and Philadelphia metro areas. At $370,000 median home price and $60,724 in annual revenue, Pocono Township delivers a 2.67x ratio. The market benefits from year-round demand: ski season in winter, lake activities in summer, and fall foliage tourism in autumn.

Joshua Tree CA — 1.93x DSCR

Despite California's generally high real estate prices, Joshua Tree remains accessible at a $450,000 median. The desert aesthetic that dominates Instagram and social media drives strong demand: $338 ADR and 48% occupancy produce $53,199 in annual revenue against $27,621 in debt service. Proximity to Joshua Tree National Park (3+ million annual visitors) provides a durable demand floor.

Gatlinburg TN — 1.84x DSCR

Gatlinburg's 4,000+ listings create competitive pressure, but proximity to Great Smoky Mountains National Park (the most-visited US national park) sustains strong ADR of $378. At $57,291 annual revenue against a $507,000 median home price, the cabins clear 1.84x comfortably.

Charleston SC — 1.83x DSCR

Charleston's 55% occupancy is the highest in our analysis, driven by year-round tourism, corporate travel, and wedding demand. Median revenue of $67,176 against a $599,000 home price produces a 1.83x ratio — strong for a coastal market at that price point.

Branson MO — 1.80x DSCR

Branson is one of the most affordable STR markets in the country, with a median home price of just $261,000. Annual revenue of $28,796 against a $16,020 annual mortgage clears the threshold cleanly. Branson draws 9 million visitors annually to its entertainment district, Table Rock Lake, and Silver Dollar City — producing consistent 41% occupancy with a $259 ADR.

Kissimmee FL — 1.75x DSCR

Disney World proximity drives 50% occupancy — the second-highest in our analysis. With median revenue of $39,725 against a $369,000 median home price, Kissimmee now produces solid DSCR despite nearly 10,000 active listings in the market.

Nashville TN — 1.55x DSCR

Over 7,000 active listings compete in a market with a $480,000 median home price, but Nashville's music-and-bachelorette tourism keeps median revenue at $45,657 — enough to clear 1.55x DSCR at standard terms.

Broken Bow OK — 1.48x DSCR

Broken Bow's luxury cabin market carries a $650,000 median home price — more expensive than Nashville or Austin — but the cabins generate $58,869 in annual revenue and a $469 ADR, producing a clean 1.48x. Drive-to demand from Dallas-Fort Worth (3 hours) and Oklahoma City (3.5 hours) sustains bookings year-round.

Gulf Shores AL — 1.44x DSCR

At $477,000 median home price and $42,154 revenue, the 5,200+ listing count creates supply pressure but the Alabama Gulf Coast's family beach appeal sustains demand. A 3-bedroom beachfront unit with professional photography and dynamic pricing can push revenue to $50,000+ and clear 1.70x.

Destin FL — 1.31x DSCR

Destin's premium Gulf beaches and emerald-water reputation produce $51,861 in revenue against a $645,000 median home price. The 1.31x ratio is tighter than inland cabin markets, but Destin's 4+ bedroom beachfront segment generates disproportionate revenue and clears DSCR with room to spare.

Myrtle Beach SC — 1.30x DSCR

Myrtle Beach's 8,900+ active listings create intense competition, but affordable entry at $303,000 paired with $24,198 revenue keeps DSCR above 1.25x. This is the prototypical "affordable entry rescues modest revenue" case in our scorecard.

Investor insight: The twelve passing markets share a pattern — either moderate home prices under $600,000 paired with at least $24,000 in revenue, OR higher-priced markets ($600K–$700K) with $50K+ revenue driven by cabin/beach demand. For more on identifying emerging workforce-driven STR markets with low entry costs, see our recent analysis.

Borderline Markets: DSCR Between 1.0x and 1.25x

Three markets land in the gray zone — technically cash-flow positive but below the 1.25x threshold most lenders require. These can work with above-median execution or adjustments to the deal structure.

Sedona AZ (1.20x) is the closest to passing. Sedona generates the highest raw revenue in our analysis at $72,087 — but a $977,000 median home price creates a $59,969 annual mortgage that drags DSCR below 1.25x. Sedona is a case study in how high entry costs can constrain DSCR even at premium ADR ($443) and occupancy (51%). A buyer acquiring below median or targeting the luxury 4-bedroom segment ($90K+ revenue) can clear the threshold.

Big Bear Lake CA (1.05x) suffers from California's high property costs ($596K) relative to seasonal mountain revenue ($38,456). The 1.05x ratio reflects a thin margin — operators targeting the ski/snowboard weekend segment with premium cabins can clear 1.25x, but median acquisition math is tight.

Markets Where the Math Breaks: DSCR Below 1.0x

Three markets fail outright to produce enough STR revenue to cover basic debt service. They share a common structural problem: median home prices that vastly outpace achievable STR revenue.

Luxury Markets With High Entry Costs

Scottsdale AZ (0.89x) is a luxury market where the median home price of $880,000 outpaces STR revenue of $47,851. Even strong occupancy (49%) and a $428 ADR cannot compensate for a $54,014 annual mortgage. Scottsdale DSCR financing requires either ultra-premium properties that generate $70,000+ in revenue or a down payment approaching 40%.

Regulated and Oversupplied Urban Markets

Denver CO (0.73x) faces structural headwinds: 4,800+ listings, $222 ADR (the lowest in our analysis among vacation-oriented markets), and only $26,497 in annual revenue against a $590,000 median home price. Denver's regulatory environment, which requires a primary residence license for STR, further constrains revenue potential.

San Francisco CA (0.45x) produces the worst DSCR ratio in our analysis by a wide margin. A $1.3 million median home price (conservative — Bloomberg reports $2.15M as of March 2026) creates a $79,814 annual mortgage. STR revenue of $36,218 covers less than half. San Francisco's strict STR regulations compound the problem — only primary residences with 90-day annual caps qualify for short-term rental permits.

The takeaway: The remaining failing markets all share one feature — median home prices above $580K paired with revenue that cannot keep pace due to regulation, urban long-stay skew, or luxury pricing overshooting leisure demand. DSCR financing rewards affordable entry more than raw revenue.

How to Improve Your DSCR Ratio

If your target market falls short of 1.25x, four strategies can close the gap.

1. Increase your down payment. Moving from 25% to 35% down reduces the loan amount by 13%, directly improving your DSCR by the same margin. A Sedona property at 1.20x DSCR with 25% down improves to 1.38x at 35% down — clearing the threshold cleanly. The trade-off is more capital locked up per property.

3. Choose an STR-specialized lender. According to Grafton Funding, "many DSCR lenders only accept long-term rent comparables, meaning working with an STR-naive lender means your oceanfront Airbnb gets evaluated like a standard rental — and your DSCR may look terrible." STR-specialized lenders like Griffin Funding, Kiavi, and Easy Street Capital use projected Airbnb income from market data platforms, which more accurately reflects your property's earning potential.

DSCR Loan Terms and Rates in 2026

Understanding the current lending landscape helps investors model accurate DSCR calculations and negotiate better terms.

LTV and down payment: Standard is 75% LTV (25% down) for STR properties. Some lenders offer up to 80% LTV for borrowers with strong credit and DSCR above 1.25. Sub-1.0 DSCR properties typically require 25–35% down.

Major DSCR lenders for STR investors: Griffin Funding, Kiavi, Easy Street Capital, Defy Mortgage, New Silver, and MoFin Loans. Key differentiators include whether they accept projected STR income (critical for purchases), minimum DSCR threshold, and closing speed (ranging from 6 to 45 days).

No property limit: Unlike conventional mortgages capped at 10 properties, DSCR loans have no cap. Each property qualifies independently, making this the preferred financing vehicle for investors scaling to 5, 10, or 20+ properties.

Tax angle: DSCR-financed STR properties qualify for the short-term rental tax loophole, which lets investors offset W-2 income with STR losses through cost segregation and bonus depreciation. The combination of DSCR financing + STR tax benefits creates a powerful wealth-building structure for investors who select markets with favorable DSCR ratios.

Calculate Your Property's DSCR

The scorecard above uses market medians — your specific property will vary based on purchase price, property type, and revenue execution. AirROI's calculator computes DSCR alongside cap rate and cash-on-cash return for any US market, using real revenue data from comparable listings.

Enter your target property's purchase price, down payment, and interest rate, and the calculator uses AirROI market revenue data to compute your projected DSCR automatically.

Frequently Asked Questions

Most DSCR lenders require a minimum ratio of 1.0 to 1.25 for short-term rental properties. A DSCR of 1.25 means the property generates 25% more rental income than the annual mortgage payment. Properties above 1.35 typically qualify for better interest rates, while some specialty lenders offer no-ratio programs for sub-1.0 DSCR with larger down payments of 25–35%.

Yes. DSCR loans qualify borrowers based on the property's projected or actual rental income rather than personal W-2 income. For purchase loans without operating history, lenders use projected STR income from market data platforms based on comparable listings. For refinances with 12 or more months of operating history, lenders typically use actual gross rental receipts from your hosting platform.

Based on AirROI data combined with 2026 median home prices, markets with the highest DSCR ratios include Logan OH/Hocking Hills (3.51x), Pocono Township PA (2.67x), Joshua Tree CA (1.93x), Gatlinburg TN (1.84x), Charleston SC (1.83x), and Branson MO (1.80x). These markets combine strong STR revenue with relatively affordable entry prices — the common thread is median home prices under $600,000 paired with at least $24,000 in annual revenue.

Four strategies work: increase your down payment from 25% to 35% to reduce the mortgage and improve DSCR by roughly 13%, target higher-revenue property types such as 3-bedroom cabins instead of 1-bedroom condos, choose an STR-specialized lender that uses projected Airbnb income rather than long-term rent comparables, and consider markets where the math naturally works rather than forcing a deal in a high-cost market.

DSCR loans are better when you already own multiple properties and DTI limits block conventional financing, when you are self-employed or have complex income, or when you want to scale quickly without property count limits. Conventional loans offer 0.5–1.5% lower rates and are better when you have strong W-2 income and fewer than 10 financed properties. The break-even point for most investors is around property number 3 or 4, when conventional DTI limits start binding.