Missouri SB 1066: The $2,655 STR Property Tax Trap Investors Just Dodged

A typical Branson short-term rental brings in $23,501 a year in gross Airbnb revenue. Until March 25, 2026, Missouri county assessors had the legal cover to erase $2,655 of that annually through a single administrative decision — flipping a residential single-family home to the 32% commercial assessment rate and triggering what Rep. Chris Brown called "almost a 70% increase in property taxes." Missouri SB 1066, which cleared the Senate 30-3 on March 25 with a companion House bill passing April 2, blocks that reclassification outright. For the 3,146 active Airbnb hosts in Branson and the 1,395 in Osage Beach and Lake Ozark, SB 1066 is not a tweak to the tax code — it is the difference between keeping and losing 10-20% of a property's entire annual STR revenue. This analysis uses AirROI data to quantify the exact dollar hit Missouri investors just avoided, walks through the mechanics of the loophole, and shows why investors in Tennessee, Florida, and Arizona should be watching Jefferson City closely.

Missouri SB 1066 in 30 seconds: What the Senate passed

The Missouri Senate voted 30-3 to pass SB 1066 on March 25, 2026, explicitly classifying single-family homes rented for fewer than 30 consecutive days as residential property for tax assessment purposes — capped at 15 properties per owner. Sen. Ben Brown (R-26) sponsored the bill, and the companion House measure HB 1768 passed the Missouri House on April 2, 2026. An earlier version, HB 1086, sponsored by Rep. Chris Brown (R-Kansas City), had already passed the House 118-34 in the prior session, giving SB 1066 unusually broad momentum heading into the mid-May session close.

The mechanics matter. SB 1066 amends Missouri's real property definitions under RSMo 137.016 so that the existence of state sales tax on short-term rental revenue does not, by itself, push a property into the commercial classification bucket. Assessors must now also consult the owner before attempting any reclassification. The 15-property cap is a deliberate compromise — it shields the typical hobbyist host and the small three-to-five-unit operator while preventing the residential rate from becoming a tax shelter for institutional landlords running 50-plus units.

The transient housing loophole, explained

| Dimension | Residential (19%) | Commercial (32%) |

|---|---|---|

| Assessment ratio of market value | 19% | 32% |

| Assessed value on a $400,000 Branson SFH | $76,000 | $128,000 |

| Annual tax at Taney County effective rate 0.97% | ~$3,880 | ~$6,535 |

| Absolute annual tax increase | — | +$2,655 |

| Percent increase in tax bill | — | +68.4% |

| % of gross STR revenue consumed ($23,501) | 16.5% | 27.8% |

"Some county assessors have started changing the classification of these properties from residential to commercial without clear statutory authority or consistent criteria, resulting in an almost 70% increase in property taxes." — Rep. Chris Brown (R-Kansas City), HB 1086 sponsor, via KOMU News

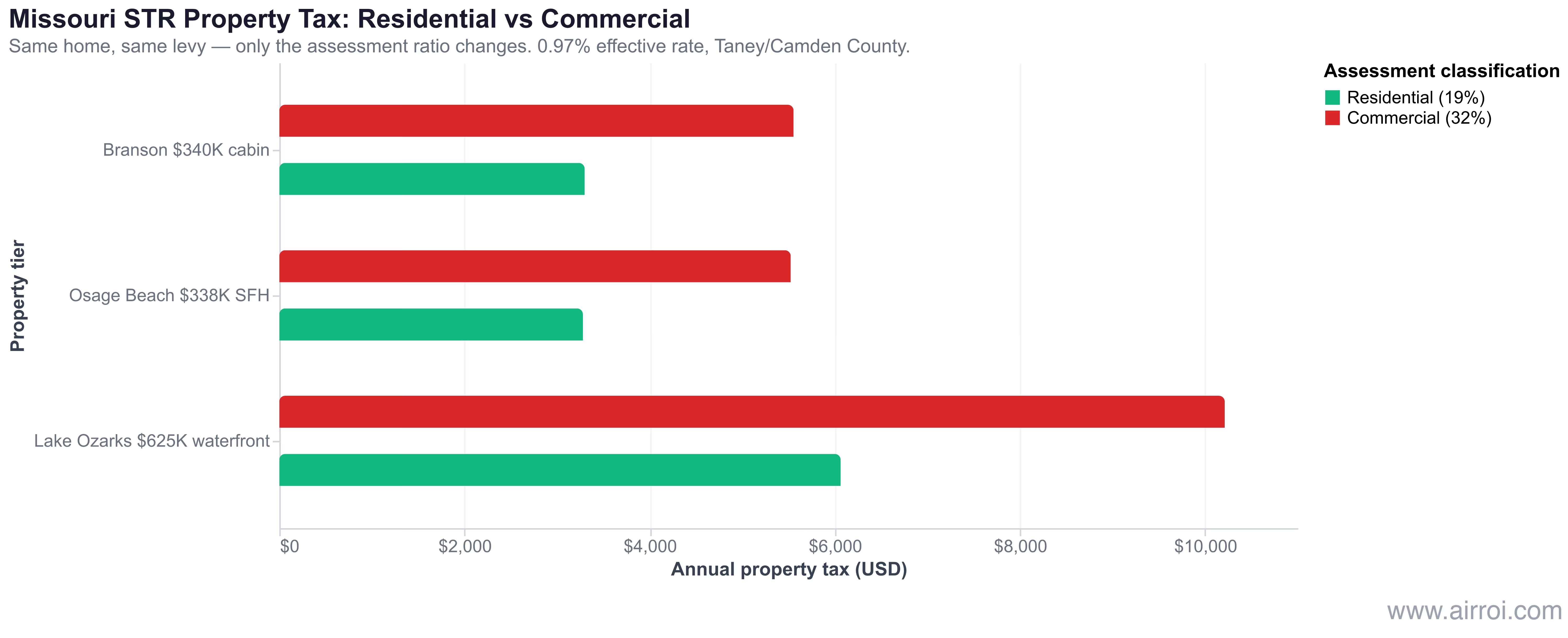

Branson case study: Quantifying the $2,655 hit

AirROI's Branson market data frames the stakes precisely. The 3,146 active Branson listings generate a median $23,501 in gross annual revenue per property at a $258.80 average daily rate and 41% occupancy — a classic leisure market that depends on a short, intense summer booking window. Monthly revenue peaks at $5,518 in June and $5,810 in July, then collapses to $1,358 in January and $1,312 in February. Property taxes, unlike revenue, do not have a low season. They land in one annual bill that has to be paid regardless of whether Silver Dollar City had a good weekend.

The picture tightens when you look at what Branson investors actually make. The seasonal revenue curve means most hosts earn roughly $15,000 of their $23,501 gross revenue during the June-to-August peak. Strip out cleaning, supplies, platform fees, utilities, insurance, and debt service, and the net margin on a typical Branson cabin is often $6,000 to $10,000 per year. Commercial reclassification on its own consumes 22% to 38% of that net — enough to convert a profitable rental into a break-even asset. SB 1066 is not protecting windfall profits; it is protecting the already-thin net margins on Missouri's entry-level STR deals.

Lake of the Ozarks: Bigger homes, bigger exposure

Run the same math on a $625,000 Camden County waterfront home that a retired couple uses as an intermittent STR. At 19% residential assessment and a 0.97% effective tax rate, the annual bill lands near $6,063. Under commercial reclassification, the same home owes approximately $10,212 — a $4,149 increase. That delta equals 20% of the home's $20,740 gross STR revenue. For a part-time host who rents the waterfront property on summer weekends and holiday weeks, losing a full fifth of gross revenue to an assessment rule change would push the economics below break-even once HOA dues, dock fees, utilities, insurance, and cleaning are layered in. Many of these properties would delist entirely, which is exactly what MOVHA documented happening in the St. Louis case.

The pattern is worth noting because Lake of the Ozarks demonstrates why commercial reclassification is a percentage play that disproportionately punishes higher-value real estate. The 19-to-32 ratio jump is applied to true value in money, so a $625,000 waterfront home eats a tax increase 84% larger in absolute dollars than the same increase on a $340,000 cabin. The Missouri STR investors with the most at risk under reclassification were never the commercial operators; they were the retirees and second-home owners who bought one waterfront property because they wanted to own a lake house and could afford to offset carrying costs with summer rentals.

Osage Beach's July peak revenue of $7,532 per listing — more than a third of annual income concentrated in one month — compounds the pressure. Property tax landed in January doesn't care that the lake freezes. Without SB 1066, Lake of the Ozarks investors would be writing a check in the middle of the off-season that equaled roughly a full summer weekend's gross revenue.

How Jackson County previewed the fight in 2025

Jackson County's 2025 reassessment is the story that made SB 1066 politically inevitable, and it is the story every STR investor outside Missouri should read carefully. In early 2025, then-Jackson County Assessor Gail McCann Beatty began reclassifying identified short-term rental properties from Missouri's 19% residential rate to the 32% commercial rate — systematically, property by property, without new legislation or a voter mandate. AirROI data shows Kansas City's 1,443 active STR listings generating a median $16,757 each in annual revenue, which means more than 1,400 Missouri hosts were potentially exposed to an immediate 68% property tax hike simultaneously.

SB 1066 converts the ad hoc political save into statutory protection. Jackson County dodged a bullet because a small group of organized hosts happened to have the right legislative allies at the right moment. Every Missouri STR investor now gets the protection by default. That is the real policy upgrade — not the specific math of the 19%-to-32% jump, but the shift from "hope your county assessor is reasonable" to "state law makes the reclassification illegal."

Which states are still exposed?

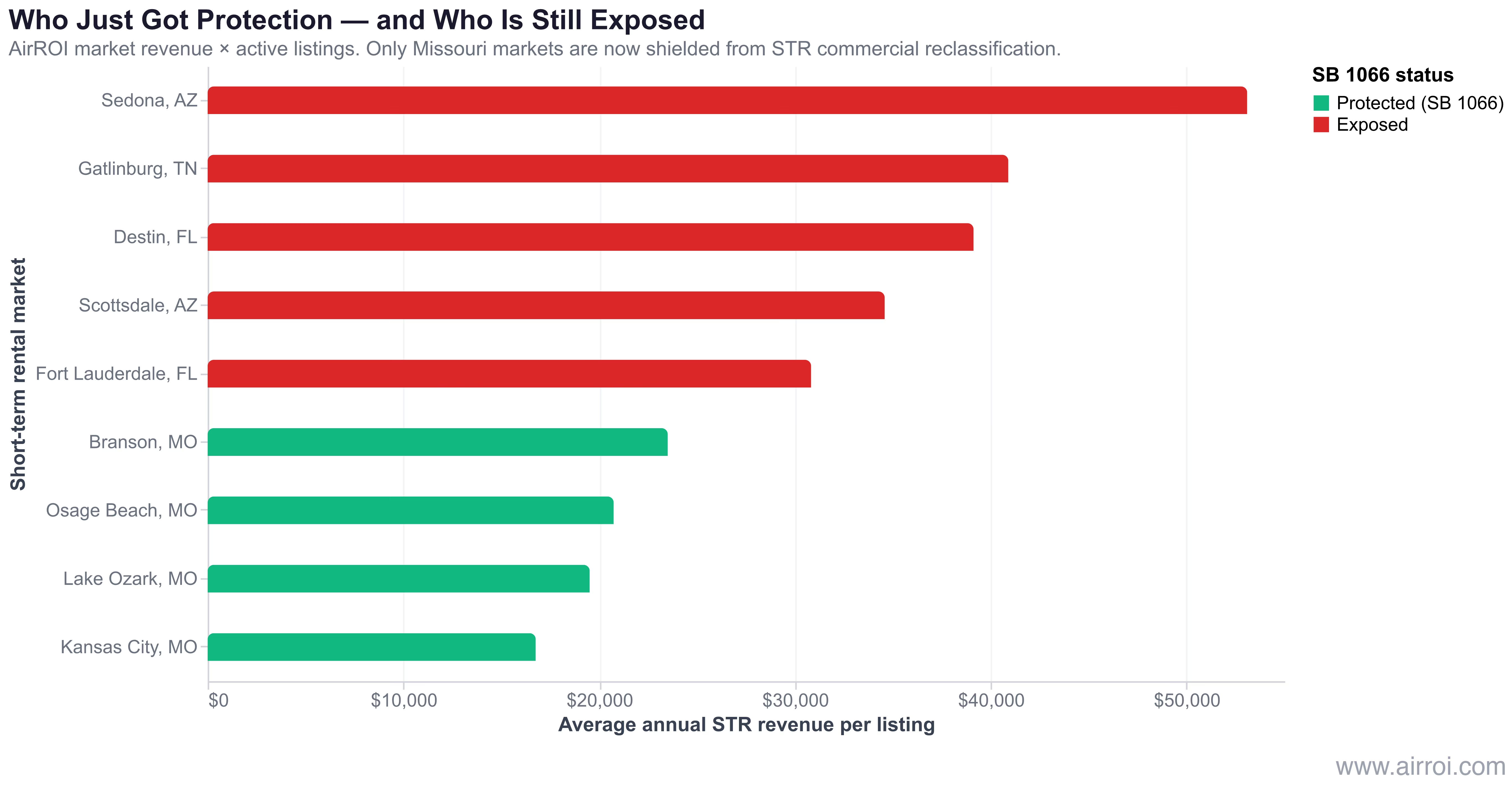

Missouri's move leaves it as the only state with explicit statutory protection against STR commercial reclassification. The states with the largest STR tax bases and the most latitude for assessor-level reclassification all remain exposed — and the AirROI data makes the stakes visible in a way the policy coverage does not.

| Market | Active Listings | Avg Annual Revenue | SB 1066-Style Protection? |

|---|---|---|---|

| Branson, MO | 3,146 | $23,501 | Yes (SB 1066) |

| Osage Beach, MO | 927 | $20,740 | Yes (SB 1066) |

| Lake Ozark, MO | 468 | $19,515 | Yes (SB 1066) |

| Kansas City, MO | 1,443 | $16,757 | Yes (SB 1066) |

| Gatlinburg, TN | 3,864 | $40,899 | No |

| Destin, FL | 4,049 | $39,121 | No |

| Sedona, AZ | 1,802 | $53,100 | No |

| Scottsdale, AZ | 4,720 | $34,582 | No |

| Fort Lauderdale, FL | 4,018 | $30,823 | No |

Gatlinburg alone represents the largest single reclassification exposure in the United States. The market's 3,864 active listings generate $40,899 in median annual revenue — a combined gross base of roughly $158 million that a single Sevier County assessor decision could re-rate overnight. Tennessee's classified property tax system is different from Missouri's, but the underlying dynamic is identical: state statute gives local assessors discretion over classification, and local officials are under mounting fiscal pressure. Destin and Scottsdale are similar stories — large, mature STR markets where millions of dollars in annual tax revenue could be unlocked through a single administrative reclassification, with no state bill currently blocking the move.

The investor checklist: How to price reclassification risk before you buy

For investors active outside Missouri, here is the concrete pre-purchase process to avoid walking into a reclassification trap. None of these checks take more than an hour. All of them should happen before you sign an offer, not after.

1. Pull the property's current assessment classification from the county assessor's office. Every county in the United States publishes its property tax roll, and the classification is a line item on the record card. Verify it reads "residential" — not "commercial," "lodging," "transient," or anything that hints at a different rate. If the classification is ambiguous or the assessor's office has recently changed its policy, treat it as a red flag.

2. Search local ordinances and recent assessor bulletins for 'transient housing' or 'commercial lodging' language. This is how Jackson County's 2025 push started — not with a new law, but with the assessor reinterpreting existing statutory definitions. If you find that language in a recent bulletin or policy memo, assume reclassification risk is active in that county.

3. Look at the reassessment cycle history. How often does the county reassess? Have any STR properties been reclassified in the past three years? A county that has already tried and either succeeded or been reversed is more likely to try again. Counties with a clean record and no STR-specific assessment guidance are lower-risk.

5. Prefer states with statutory protection. As of April 2026, Missouri is the only state with explicit statutory language blocking STR commercial reclassification, with Arizona and Ohio advancing adjacent preemption bills. Until more states pass Missouri-style language, concentrate portfolio exposure in states where reclassification risk is either statutorily blocked or genuinely low (no pending assessor activity, no county-level policy memos, no recent reassessment fights). Commercial operators with more than 15 properties need to pay particular attention to the SB 1066 cap — above the threshold, even Missouri no longer offers full protection.

One broader point: property tax reclassification is one of three main revenue levers local governments are using against STRs right now, alongside lodging tax increases and licensing caps. The other two are more visible and easier to lobby against, which is exactly why reclassification is the one that keeps catching investors off guard. Missouri's SB 1066 flips the default — from "prove your property should be residential" to "prove it shouldn't be." Every investor modeling STR deals in 2026 should want that default applied in their own state next.

Bottom line: The least-priced risk in STR investing just became the most visible

Missouri STR investors just avoided a property tax increase of roughly $2,655 per year on a typical Branson cabin and $4,149 per year on a typical Lake of the Ozarks waterfront home — exposures that would have consumed 10-20% of gross STR revenue per property on the 4,541 protected Missouri listings tracked by AirROI. SB 1066 is the first state law to close the commercial reclassification loophole explicitly, and the Jackson County 2025 backstory shows what happens when no such law exists: hosts are at the mercy of whichever county assessor is feeling most creative about revenue generation.

The broader lesson is that property tax is the STR variable nobody talks about until it moves. Most investor analysis focuses on ADR, occupancy, and RevPAR; most regulatory analysis focuses on permit caps and lodging tax rates. Commercial reclassification sits in the blind spot between the two, and it can silently erase more margin than either lever. Missouri just made it visible by writing statute around it. Investors in Tennessee, Florida, Arizona, and Georgia should be spending an hour with their county assessor's classification records before they sign their next STR offer — and watching Jefferson City's final passage of SB 1066 as a template for what their own state legislature needs to do next.

Frequently asked questions

What does Missouri SB 1066 actually do?

Missouri SB 1066 amends the state's real property definitions to explicitly classify single-family homes rented for fewer than 30 days as residential property, capped at 15 properties per owner. The bill passed the Missouri Senate 30-3 on March 25, 2026 and blocks county assessors from reclassifying short-term rentals as commercial property — a loophole Jackson County's assessor attempted to exploit in 2025.

How much would a commercial property tax reclassification cost a Missouri STR investor?

Commercial reclassification pushes Missouri's assessment ratio from 19% to 32%, which translates to roughly a 68% increase in the annual property tax bill. For a typical $340,000 Branson cabin, that is about $2,255 more per year in taxes — nearly 10% of the $23,501 in gross Airbnb revenue the typical Branson listing generates according to AirROI data. One St. Louis host reported their bill jumped from $8,000 to $20,000 annually after a reclassification plus revaluation.

What happened with Jackson County Missouri short-term rentals in 2025?

Jackson County Assessor Gail McCann Beatty reclassified identifiable STRs from the 19% residential rate to the 32% commercial rate in early 2025. After host backlash organized by the Missouri Vacation Home Alliance and MAREI, the Jackson County Legislature passed emergency Ordinance 5987 in June 2025 pausing reclassifications pending a countywide registration system. In November 2025, Jackson County voters approved a ballot question making the Assessor an elected position starting in 2028.

Is commercial property tax reclassification happening outside Missouri?

Yes. County assessors in Florida, Tennessee, Arizona, and Georgia have been exploring similar reclassifications as STR markets grow, and Arizona and Ohio have active preemption bills in 2026. Missouri's SB 1066 is the first bill to explicitly close the loophole at the state level. For reference, Gatlinburg TN hosts 3,864 active listings generating $40,899 each in annual revenue — a tax base that a single county decision could re-rate overnight.

Should I check my property's assessment classification before buying an STR?

Yes. Before closing on any short-term rental purchase, pull the property's current tax classification from the county assessor's office, check local ordinances for "transient housing" or "commercial lodging" language, and model a 60-70% worst-case tax hike into your underwriting. In states without statutory protection, a single assessor decision can add $2,500-$6,000 per year to carrying costs — a number your AirROI-powered revenue projection should always account for.