Short-Term Rental Ordinance 2026: The Small-City Wave

The next short-term rental crackdown will not come from a city you have heard of. While Los Angeles (14,083 active listings) and New York (18,772) dominate the regulation headlines, six small and mid-sized US cities quietly advanced a short term rental ordinance in a single week of May 2026 — and that is the more important story for hosts. This wave of small city Airbnb regulations spans Madison, Wisconsin (a proposed cap of 190 permits), Bakersfield, California (its first-ever ordinance plus a 12% lodging tax), Berea, Ohio (1,000-foot buffers ahead of the Cleveland Browns' stadium move), Decatur, Alabama (registration backed by $500-per-day fines), Arapahoe County, Colorado (a 500-foot separation rule effective late June), and West Columbia, South Carolina (collecting public input through May 31).

AirROI market data shows these six markets host roughly 7,500 active listings generating well over $150 million in combined annual revenue — money that caps, buffers, and registration thresholds can directly remove. The regulatory playbook perfected in big metros is now being copied, clause by clause, into towns a fraction their size. This analysis quantifies the revenue at risk per market, explains why the frontier moved down-market, and lays out the data signature operators should watch before their own city is next.

Disclaimer: This article is for informational purposes only and is not legal or investment advice. Short-term rental rules change quickly; verify current requirements with your local jurisdiction before acting.

Six Cities, One Week: The Small-City STR Ordinance Wave

Six US cities advanced short-term rental rules within days of each other in May 2026, each with a distinct mechanism — caps, buffers, registration, or a responsible-agent mandate. The table below pairs each city's AirROI market profile with the specific rule on the table, so the revenue exposure is legible at a glance.

| Market (AirROI scope) | Active listings | Occupancy | ADR | RevPAR | Annual rev/listing | The rule |

|---|---|---|---|---|---|---|

| Madison, WI | ~366 | 50% | $241.80 | $120.70 | $25,701 | 190-permit citywide cap |

| Bakersfield, CA | ~747 | 43% | $178.00 | $78.10 | $17,198 | First-ever permit + 12% TOT |

| Berea, OH* | ~49 | 46% | $188.00 | $91.50 | $21,951 | 1,000-ft buffer, $100 permit |

| Decatur, AL | ~69 | 38% | $158.60 | $64.40 | $14,010 | Registration, $500/day fine |

| Arapahoe Co., CO** | ~735 | 47% | $162.80 | $79.00 | $16,245 | 500-ft separation + agent |

| West Columbia, SC* | ~120 | 49% | $205.10 | $102.80 | $25,573 | Under public input |

*Berea and West Columbia are thin standalone markets; their parent metros (Cleveland: ~1,979 listings, $190 ADR; Columbia: ~1,040 listings, $195 ADR) frame the surrounding demand. *Arapahoe County's unincorporated STR market is proxied by Aurora, the county's largest city. Source: AirROI market data, trailing 12 months, May 2026.

Why Small Cities Are Regulating Airbnb in 2026

Three forces converged to push new Airbnb rules 2026 down-market: spillover from big-metro crackdowns, local housing-affordability pressure, and event catalysts. Berea is the clearest example of the third — a stadium relocation creating anticipated demand that the city chose to cap preemptively rather than absorb. The first two forces are structural: as Los Angeles and New York demonstrated that registration and primary-residence rules can shrink supply, smaller councils gained both a template and political cover to act.

The housing-pressure force is quieter but pervasive. In markets where median home prices have outrun local wages, every unit converted to a nightly rental is a unit removed from the long-term pool — a politically potent argument that does not require a market to be large to land. Decatur, Bakersfield, and West Columbia are not vacation destinations; they are working cities where the STR debate is framed less around tourism management and more around neighborhood character and housing supply. That framing is exactly what lets a 69-listing market like Decatur generate enough council attention to produce an ordinance.

Preemption does not end the fight — it relocates it. Where states forbid caps, cities pivot to permitting, safety, and tax. Where they stay silent, councils reach for the hard tools first.

The net effect is a regulatory landscape splitting into two tracks. In preemption states, the wave manifests as registration and tax regimes that survive legal challenge. Everywhere else — Wisconsin, Colorado, Alabama, South Carolina — councils are free to deploy caps and separation buffers, and in May 2026 four of them did exactly that within a single news cycle.

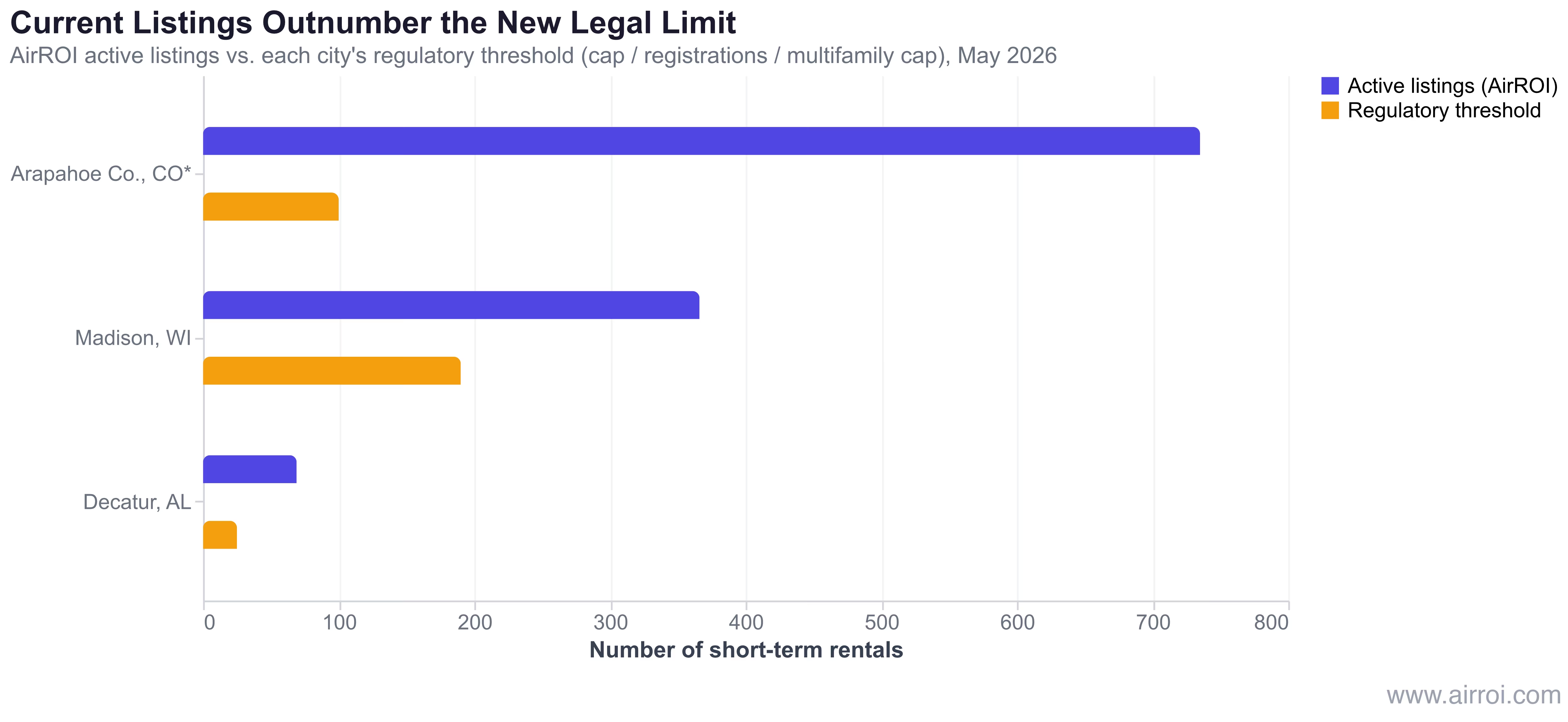

Revenue at Risk: What the Data Says City by City

Across the six wave markets, AirROI data puts roughly 7,500 active listings and well over $150 million in annual revenue inside the regulatory perimeter. The exposure is not evenly distributed — it concentrates in the markets with hard numeric limits and in the non-owner-occupied units that caps and separation rules target first.

Madison is the cleanest short term rental permit cap math. A ceiling of 190 against 295 to 366 measured active listings means a sizable share of current operators could be locked out the moment the cap takes effect — and because Madison already requires owner-occupancy, the investment units held by non-resident owners sit at the front of that line. At $25,701 in annual revenue per listing, an investor running two exposed units faces roughly $51,400 a year hanging on a permit decision.

Arapahoe County's 500-foot rule is a cap in disguise. A separation buffer is a soft cap: once one property on a block is licensed, every neighbor inside the radius is shut out, regardless of how many would otherwise qualify. At Aurora's $16,245 in annual revenue per listing — our proxy for the county's unincorporated market — and roughly 735 active listings in the broader market, even a modest buffer reshapes which addresses can legally operate.

The Compliance Gap: Decatur's 25-Signup Warning

Decatur, Alabama is a live experiment in the short term rental compliance gap — the distance between operators required to register and those who actually do. As of May 2026, only about 25 hosts had signed up under the new ordinance, against the roughly 60 to 69 active listings AirROI measures in the city. That is a participation rate below half, and it persists even though unpermitted operation will draw fines of up to $500 per day once the 90-day grace period ends in July.

The pattern is not unique to Decatur. Low early participation is the default state of every new registration regime, because the rational move for an individual operator is to wait and see whether the city actually enforces. The trouble is that what is rational for one host is corrosive for the whole market: a city that collects 25 registrations where it expected 60-plus concludes that voluntary compliance has failed, and reaches for the tools that do not depend on goodwill — platform-data subpoenas, escalating per-day fines, and proactive sweeps. The under-registered market effectively recruits its own harder enforcement.

The compliance gap is a signal, not just a statistic. A low early-registration rate tells a city that voluntary participation will not produce the data it wants — which is precisely what pushes councils toward stricter enforcement, higher fines, or platform-data mandates next.

The Down-Market Frontier: How These Rules Compare to LA and NYC

Second-tier cities are a fraction of the size of the headline markets, but their regulations are not watered-down versions — they are near-copies. The comparison below shows the frontier shifting, not softening.

| Dimension | Second-tier wave (Madison, Decatur, Arapahoe) | Big-metro precedent (LA, NYC) |

|---|---|---|

| Active listings | 49–747 per city | LA 14,083 / NYC 18,772 |

| Rule type | Caps, separation buffers, registration, responsible agent | Primary-residence rules + platform delisting |

| Enforcement maturity | New; grace periods; low signup rates | Years of enforcement infrastructure |

| Host revenue at stake per listing | $14,010 (Decatur) – $49,153 (Scottsdale) | Higher ADR, but more units already removed |

What is genuinely different down-market is the political terrain. Big metros have organized host associations, professional lobbying, and press scrutiny that slow ordinances and soften their edges. A council in a town of 50,000 faces none of that friction. The same rule that takes three years and a lawsuit to pass in Los Angeles can clear a small-city council in a single spring — which is exactly the speed the May 2026 wave demonstrated.

How to Read the Data Signature Before Your City Is Next

The markets that regulate next are legible in the data months ahead of the ordinance. A short-term rental market about to draw regulation shows a recognizable signature: listing counts growing faster than housing stock, a cluster of rentals concentrated in a few desirable neighborhoods, rising parking and noise complaints, and — the leading indicator that matters most — a zoning-code amendment appearing on a planning-commission agenda. By the time a public hearing is scheduled, the rules are usually 80% written.

Operators in unregulated second-tier markets can act on that signal rather than react to the headline. The practical moves, in order of leverage:

- Monitor the planning-commission calendar. Code-amendment study sessions and STR working groups are the earliest public artifact of intent. They precede a published ordinance by months.

- Register the day applications open. Decatur's data shows the cost of waiting; early registrants lock in legal status and often qualify for legacy exemptions that latecomers do not. Arapahoe County, for instance, gives operators active within six months before the effective date a legacy path — but only if they apply within 60 days of adoption.

- Stress-test exposure to caps and buffers. If your units are non-owner-occupied or clustered with other rentals on one street, you are in the highest-risk category for caps and separation rules. Know that before the rule exists.

- Keep a mid-term rental exit ready. Converting to 30-plus-day stays exits most STR ordinance definitions; it trades peak nightly revenue for regulatory durability and is the standard defensive move in a capped market.

- Line up a local responsible agent. Where responsible-agent rules spread — Arapahoe requires a contact reachable by phone within 15 minutes and on-site within 60 — absentee out-of-state ownership becomes non-compliant unless local management is already in place.

The deeper point is that regulation has stopped being a big-city problem. AirROI's market-level data — active-listing trends, RevPAR, occupancy, and the concentration of non-owner-occupied units — is the same signature councils read when they decide a market needs rules. Operators who read it first get to choose their response; everyone else gets to file an appeal.

Frequently Asked Questions

In one week of May 2026, six US cities advanced short-term rental ordinances: Madison WI (a 190-permit cap), Bakersfield CA (a first-ever permit plus 12% tax), Berea OH (1,000-foot buffers ahead of the Browns stadium), Decatur AL (registration backed by $500-per-day fines), Arapahoe County CO (a 500-foot separation rule), and West Columbia SC (under public input through May 31). The pattern marks the regulatory frontier shifting from big metros to second-tier markets.

Across the six wave markets, AirROI data shows roughly 7,500 active listings generating well over $150 million in combined annual revenue. Per-listing revenue ranges from $14,010 in Decatur to $49,153 in Scottsdale, and caps, separation rules, and registration thresholds put a meaningful share of that directly in play.

A separation rule requires a minimum distance between licensed short-term rentals to prevent clustering on one block. Arapahoe County, Colorado set that distance at 500 feet, which functions as a soft cap: once one property is licensed on a street, neighbors within the buffer cannot get a license, stranding investment units bought before the rule.

Watch the leading indicators: rapid listing growth relative to housing stock, clustering of rentals in a few neighborhoods, zoning-code amendment hearings, and parking or noise complaints. AirROI's market data — active-listing trend, RevPAR, and the concentration of non-owner-occupied units — is the data signature that typically precedes a regulatory response.

Penalties vary by city, but Decatur, Alabama fines unpermitted operators up to $500 per day once its July 2026 enforcement begins. With registration costing $500 total there, a single day of fines exceeds the entire cost of compliance — the economics overwhelmingly favor registering before enforcement starts.