Debt Service Coverage Ratio (DSCR)

Key Takeaways

- DSCR equals NOI divided by annual debt service (mortgage principal + interest)

- A DSCR of 1.0 means the property exactly covers its debt; lenders require 1.20–1.25 minimum for STR loan approval

- DSCR loans allow qualification based on property income rather than personal income — no W-2 or tax-return review required

- Higher DSCR ratios unlock better interest rates, higher loan amounts, and more favorable terms

- Market choice matters: cash-flow-oriented markets like Nashville and Gatlinburg produce higher DSCR than expensive coastal metros at the same loan-to-value

How to Calculate DSCR

DSCR = Annual Net Operating Income ÷ Annual Debt Service

Where:

- Annual NOI = Gross rental income − all operating expenses (cleaning, management, insurance, maintenance, utilities — excludes mortgage payments)

- Annual Debt Service = Total annual mortgage payments (principal + interest)

Example Calculation:

| Item | Amount |

|---|---|

| Annual gross rental income | $78,000 |

| Annual operating expenses | −$33,000 |

| Annual NOI | $45,000 |

| Monthly mortgage payment | $2,800 |

| Annual debt service | $33,600 |

DSCR = $45,000 ÷ $33,600 = 1.34

A DSCR of 1.34 means the property generates 34% more income than its mortgage demands — exceeding most lender minimums and qualifying for competitive rates.

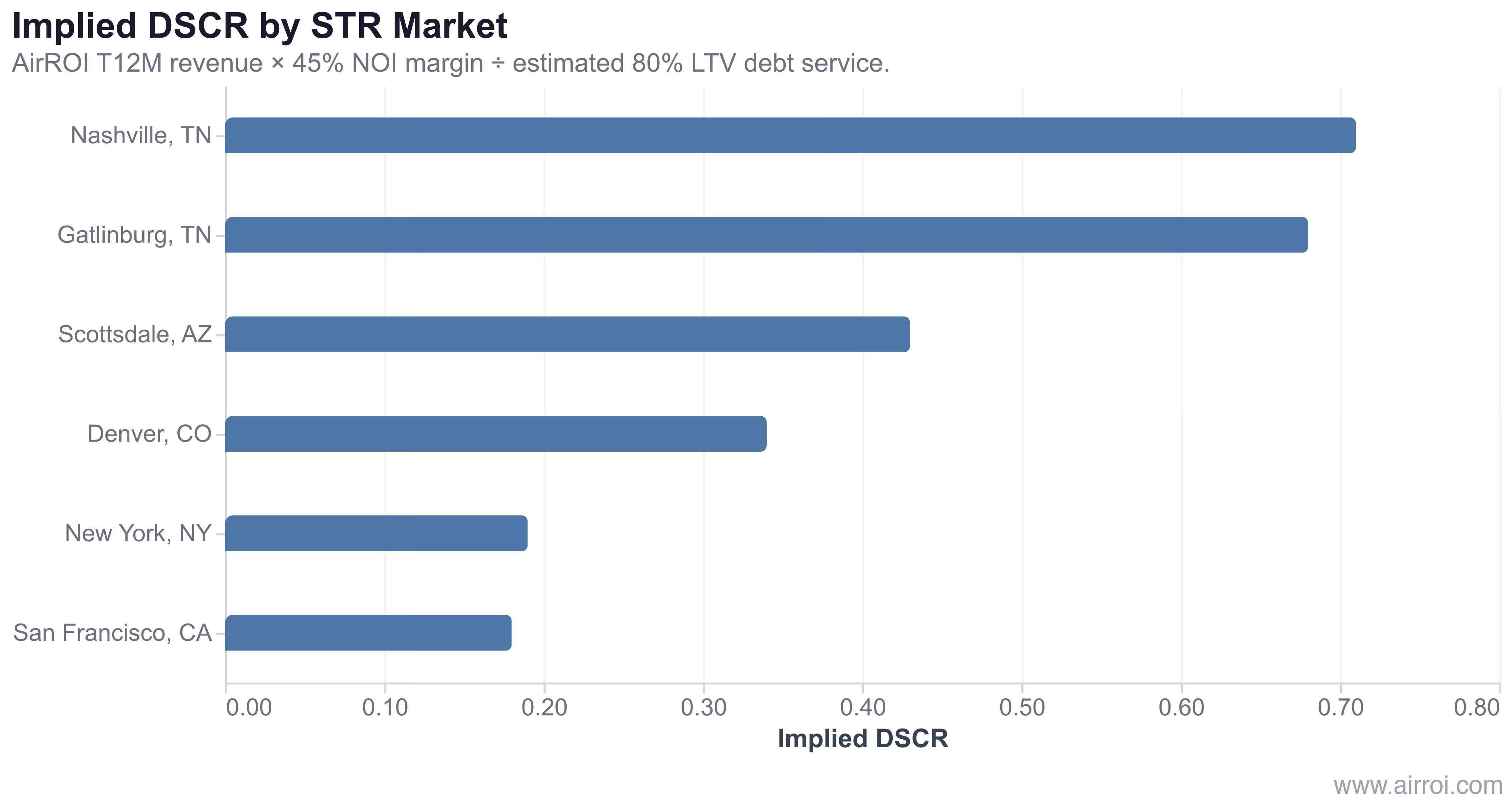

DSCR Across STR Markets

Market selection directly shapes whether a property can achieve a lender-qualifying DSCR. In AirROI's analysis of 33,659 active listings across six US markets, the implied DSCR at median revenue (applying a 45% NOI margin and an 80% LTV mortgage at 7.25%) ranges from 0.71 in Nashville to just 0.18 in San Francisco.

In AirROI's analysis of 33,659 active listings across Nashville, Gatlinburg, Scottsdale, Denver, New York, and San Francisco, city-median DSCR at 80% LTV ranges from 0.71 (Nashville) to 0.18 (San Francisco).

These city-median figures fall below the 1.20 lender threshold — which is precisely the insight. Median listing performance at median purchase price, financed at current rates, does not automatically produce a qualifying DSCR. That gap is why disciplined deal selection and larger down payments matter: a 35% down payment on the same Nashville property lifts the implied DSCR to roughly 1.10, and a high-performing listing at the 75th percentile of revenue clears 1.25 comfortably.

At today's rates, the DSCR challenge in STR investing is not revenue — it is purchase price relative to what median revenue will support. Buying below the market median, or increasing your equity stake, is the fastest route to a qualifying ratio.

DSCR Benchmarks and Loan Requirements

| DSCR Range | Interpretation | Typical Loan Terms |

|---|---|---|

| Below 1.0 | Property loses money after debt service | Loan unlikely; may require cash reserves |

| 1.0 – 1.15 | Barely covers debt; thin margin | Limited lenders; higher rates; 25%+ down |

| 1.15 – 1.25 | Adequate coverage | Standard DSCR loan terms available |

| 1.25 – 1.50 | Good coverage with safety margin | Competitive rates; 20% down possible |

| Above 1.50 | Strong coverage | Best rates; maximum leverage available |

Most DSCR lenders underwrite STR properties using projected market rent (from tools like AirROI), not the borrower's historical revenue, which means a well-selected market with strong occupancy comps can qualify even a first-time STR investor.

DSCR Loan vs. Conventional Loan

| Feature | DSCR Loan | Conventional Loan |

|---|---|---|

| Income verification | Property income only | Personal income + tax returns |

| Minimum down payment | 20% – 25% | 15% – 25% |

| Interest rates | 1–2% higher | Lower rates |

| Max properties | No limit | Typically 10 |

| Qualification speed | Faster (less documentation) | Slower (full underwriting) |

| Best for | Investors, self-employed | W-2 employees, first properties |

Why DSCR Matters for STR Investors

Loan qualification. DSCR is the primary metric lenders use to evaluate STR loan applications. Falling short of 1.20 means either restructuring the deal (larger down payment, shorter-term bridge loan) or finding a different property.

Seasonal risk buffer. STR revenue swings 30–40% between peak and shoulder seasons in most leisure markets. A DSCR of 1.25 at annualized revenue means the property still covers its mortgage during a 20% revenue dip — a thin but viable cushion. A DSCR of 1.50 absorbs a 33% revenue drop before breaking even.

Tips for Improving Your DSCR

- Increase NOI. Raise nightly rates through dynamic pricing, improve occupancy with better listing quality, or reduce operating expenses to boost the numerator of your DSCR calculation.

- Make a larger down payment. Reducing loan amount directly lowers annual debt service. Going from 80% to 70% LTV on a $500,000 property saves roughly $5,500 per year in debt service.

- Extend loan term. A 30-year amortization produces lower monthly payments than a 15 or 20-year term, improving DSCR at the cost of slower equity buildup.

- Shop for lower rates. Even a 0.5% rate reduction on a $400,000 loan saves roughly $2,000 annually — adding about 0.05 to DSCR on a $40,000 NOI property.

- Use conservative projections. Lenders discount aggressive revenue estimates. Presenting 12 months of actual STR income data, or AirROI market comparables, strengthens your underwriting package and reduces the lender's risk discount. Our STR investment analysis guide walks through building a lender-ready projection.

- Know your break-even occupancy. The minimum occupancy needed to maintain DSCR above 1.0 is the most useful stress-test metric you can put in front of a lender.

Frequently Asked Questions

Most lenders require a minimum DSCR of 1.20 to 1.25 for short-term rental loans, meaning the property's NOI must be 20-25% higher than annual debt payments. Some DSCR loan programs accept ratios as low as 1.0 or even 0.75 for strong borrowers in appreciating markets. Higher DSCR ratios (1.30+) typically qualify for better interest rates and loan terms.

Calculate DSCR by dividing the property's annual net operating income (NOI) by its annual debt service (total mortgage payments including principal and interest). For example, if annual NOI is $48,000 and annual mortgage payments are $36,000, the DSCR is 1.33. Use conservative STR revenue estimates and include all operating expenses in your NOI calculation for accurate results.

Yes, DSCR loans are specifically designed to qualify borrowers based on property income rather than personal income. These no-income-verification loans evaluate the property's ability to cover debt payments. They are popular with self-employed investors and those with complex tax returns. DSCR loans typically require higher down payments (20-25%) and carry slightly higher interest rates than conventional loans.

STR investors face variable monthly income — occupancy dips during shoulder seasons can cut revenue by 30-40% temporarily — making the DSCR safety margin critical. Lenders apply extra scrutiny to STR loan applications because seasonal variance raises default risk. A DSCR of 1.25+ provides a cushion that absorbs slow months without pushing the property into negative cash flow.

Improve DSCR by increasing NOI (raise nightly rates, improve occupancy, cut operating expenses) or reducing annual debt service (larger down payment, longer amortization, lower interest rate). Even a 0.5% rate reduction on a $400,000 loan saves roughly $2,000 per year in debt service, adding about 0.05 to your DSCR on a $40,000 NOI property.